--

Weekly Market Update for the Week Commencing

16th January 2017

Big Picture

View

Here is a summary of our big picture

view of the markets. Note that our short-term views may differ from our

big picture view.

The BULL market in US Treasury Bonds

that began in the early 1980s ended in early-2015, but there will be many years

of topping action in bond prices and bottoming action in bond yields before

major new trends get underway. (Last update: 29 June 2015)

The stock market, as represented by the S&P500 Index,

commenced

a secular BEAR market during the first quarter of 2000, where "secular

bear market" is defined as a long-term downward trend in valuations

(P/E ratios, etc.) and gold-denominated prices. This secular trend will bottom sometime between 2018 and 2020.

(Last update: 29 June 2015)

A secular BEAR market in the

US

Dollar

began during the final quarter of 2000 and ended in July of 2008. This

secular bear market will be followed by a multi-year period of range

trading.

(Last

update: 09 February 2009)

Gold commenced a

secular bull market relative to all fiat currencies, the CRB Index,

bonds and most stock market indices during 1999-2001.

This secular trend will peak sometime between 2018 and 2020.

(Last update: 29 June 2015)

Commodities,

as represented by the CRB Index, commenced a

secular BULL market in 2001 in nominal dollar terms. The first major

upward leg in this bull market ended during the first half of 2008, but

a long-term peak won't occur until 2018-2020.

(Last

update: 29 June 2015)

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Outlook Summary

Market

|

Short-Term

(1-3 month)

|

Intermediate-Term

(6-18 month)

|

Long-Term

(2-5 Year)

|

|

Gold

|

N/A |

Neutral

(21-Nov-16) |

Bullish

|

|

US$ (Dollar Index)

|

N/A |

Neutral

(17-Aug-16) |

Neutral

(19-Sep-07) |

|

US Treasury Bonds (TLT)

|

N/A |

Neutral

(21-Nov-16)

|

Bearish |

|

Stock Market (DJW)

|

N/A |

Neutral

(14-Nov-16) |

Bearish |

|

Gold Stocks

(HUI)

|

N/A |

Neutral

(21-Nov-16) |

Bullish

|

|

Oil |

N/A |

Neutral

(26-Oct-15) |

Bullish

|

|

Industrial Metals

(GYX)

|

N/A |

Neutral

(10-Oct-16) |

Bullish |

Notes:

1. Our short-term expectations are discussed in the commentaries, but except in

special circumstances we won't attempt to assign a "bullish", "bearish" or

"neutral" label to these expectations.

2. The date shown below the current outlook is when the most recent outlook change occurred.

3. "Neutral" means that we think risk and reward are roughly in balance with respect to the timeframe in question.

4. Long-term views are determined almost completely by fundamentals and intermediate-term views

are determined by a combination of fundamentals, sentiment and technicals.

Last week's posts at the TSI Blog

Revisiting the gold market's "London bias"

A wide-angle view of the US stock market

Summary of current

thinking/positioning

1) Thinking that the rebounds in

gold, silver and the associated mining indices are not yet close to being

over, but on the lookout for profit-taking opportunities in individual

stocks.

2) Maintaining long-term exposure to non-gold commodities

(natural gas, coal, uranium, copper, zinc, nickel, agricultural products),

but concerned that an intermediate-term correction will begin this

quarter. Hedged via EEM and USO put options.

3) Thinking that the

US Treasury Bond has significant additional short-term upside (within a

long-term bearish trend).

4) Expecting an extension of the US

equity bull market and expecting a generally-bullish global equity trend,

but concerned about short-term downside risk.

5) Thinking that the

Dollar Index is immersed in a 2-3 month correction, after which its

longer-term upward trend will resume.

6) Maintaining a large cash

reserve to hedge downside risk in equities (current cash percentage is

about 40%).

Industrial

Commodities

2017 Forecast

Here's how our 2016 annual forecast for industrial commodities (oil

and the industrial metals) was summarised:

"For this year there

is no reason to make separate forecasts for different industrial

commodities, because they are in synch. They are all massively 'oversold'

and poised for at least intermediate-term and possibly long-term upward

reversals from whatever lows are made during the first quarter."

The forecast 'panned out', although there is an as-yet-unanswerable

question as to whether the Q1-2016 upward reversals were the

intermediate-term or the long-term kind.

In one respect, this

year's forecast for industrial commodities is the opposite of last year's.

Whereas last year we were expecting an intermediate-term bottom during the

first quarter, this year we are expecting an intermediate-term top during

the first quarter. This is partly because speculators have built up

unusually-large long positions in some commodities, most notably copper

and oil. It is also because the forces that have caused the recent

strength in the prices of industrial commodities are likely to soon

disappear, at least temporarily. These forces are the US$ correction and

the Trump-related enthusiasm for any perceived beneficiary of "fiscal

stimulus".

To further explain, the Dollar Index will probably make

a new multi-year high during the second quarter of this year and the

Trump-related enthusiasm is misplaced. It is misplaced because a) the

additional US infrastructure spending will be less than anticipated (due

to budget constraints) and will have no meaningful effect on global

commodity consumption, and b) the planned tax cuts will take longer to

implement and will bring about less additional spending than currently

believed.

We expect that the Q1-2017 top will be followed by a

multi-month correction and an important bottom around mid-year in parallel

with an important top for the US$. With the US$ no longer a headwind and

speculative long positions having been greatly reduced in response to

price weakness, the stage will then be set for general commodity-price

strength during the second half of the year.

Overall, we expect

that 2017 will be an up-year for commodity prices.

Also, as part of

last year's annual forecast we wrote:

"In the commodity

markets, measures of negativity and downside momentum have reached rare

and in some cases unprecedented extremes. Also, the bottom section of the

following chart shows that the Goldman Sachs Spot Commodity Index (GNX)

has fallen to near its 2001 low relative to the S&P500 Index (SPX)."

Here is an updated version of the same chart. Note that although there

was a significant rebound in commodity prices (as represented by GNX) from

the early-2016 bottom, the GNX/SPX ratio is still near its 2001 low.

Regardless of how the commodity markets fare in nominal dollar terms, this

suggests that the risk/reward favours commodities over equities.

Copper Update

When the copper price held above

lateral support at $2.45 and bounced off its 50-day MA during the recent

pullback it opened up the possibility of a rise to as high as $3.00 prior

to a more substantial decline. Last week's price action increased the

probability of this outcome, in that the multiple tests of the $2.70-$2.75

range that have now taken place make it likely that this range will soon

be exceeded (the more times a support or resistance level is tested the

higher the probability that it will eventually be breached).

Critical support remains at $2.45, although a daily close below the 50-day

MA would warn of a downward trend reversal.

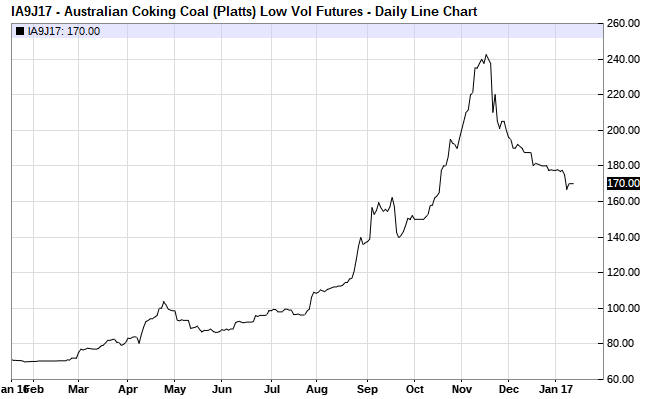

Coal Crash

The following chart shows last

year's incredible rally in the price of coking coal (the type of coal used

in steel making) to a November high of more than $240/tonne and the

subsequent plunge to a current level of $170/tonne.

Coal mining stocks haven't reacted in a big way to the 'coal crash' of

the past two months. For example, the Coal ETF (KOL) ended last Friday

within a few percent of its November-2016 closing high.

There are two reasons that coal-mining equities have taken coal's

price crash in stride. One is that despite the recent crash, the coal

price is still almost 150% higher than it was a year ago. The other is

that coal producers generally sell at contract prices that follow the spot

price with a significant lag and that rise/fall at a much slower pace than

the spot price. Consequently, the price at which most coal producers sell

is still on the rise and will be significantly higher in Q1-2017 than it

was in Q4-2016.

The TSI Stocks List has indirect exposure to coal

via Sprott Resource Corp. (SCP.TO) due to SCP's stake in Corsa Coal

(CSO.V). According to the most recent financial statements, CSO is SCP's

largest equity investment.

Coal's price plunge is almost certainly

due to the increase in supply that is occurring in response to the huge

preceding price gain. As the saying goes, in the commodity markets "the

cure for high prices is high prices".

Platinum is still

relatively cheap

A year ago we wrote that we were more

bullish on platinum than any other precious metal. That's still the case,

because relative prices are almost the same now as they were a year ago.

As illustrated by the following monthly chart, the platinum price remains

near a 50-year low relative to the gold price.

The T-Bond

rebound is just getting started

The following chart shows that

the 30-year T-Bond peaked in early-July last year and then fell all the

way back to its 2015 low. Since bottoming during the second half of

December it has rebounded to its 50-day MA.

A rebound to the 50-day MA is sometimes the best that a

downward-trending market can do, but there are good reasons to believe

that the T-Bond's rebound is not yet close to being complete. Sentiment,

as indicated by the Commitments of Traders (COT) data, is the most

important of these reasons.

The COT numbers were bullish when the

rebound began in late-December, but they are now even more bullish. In

fact, the combined COT situation for 30-year T-Bond futures and 10-year

T-Note futures is now as bullish as it has ever been. To be more specific,

speculators in long-dated Treasury futures have never been more net-short

than they are right now. The stage is therefore set for a large wave of

short-covering.

There's a good chance that the T-Bond will rise to

its 200-day MA within the next few months, but there are multiple paths it

could take to get there. One path involves some base-building over the

next few weeks with a test of the December low prior to the start of a

consistent upward trend. Another path involves only minor 1-2 week

consolidations along the way.

The T-Bond's short-term bullish

prospects are good news for gold investors, because if the T-Bond is

trending upward then in the absence of a very strong Dollar Index the

Bond/Dollar ratio will also be trending upward.

The Stock Market

The US

The NASDAQ100 Index (NDX) is continuing to work its way relentlessly

upward and has now achieved consecutive weekly closes above the big round

number (5,000). A realistic short-term target is the top of the

intermediate-term channel drawn on the following chart, but this is only

about 2% above the current price.

The Dow Industrials Index, however, has spent the past month chopping

back and forth within a narrow horizontal range just below its own big

round number (20,000). As mentioned in last week's Interim Update, it

looks like the US stock market will not reach a short-term top until the

financial news networks have had the opportunity to celebrate "Dow

20,000".

The UK

We are currently paying closer

attention than usual to the UK stock market due to the incredible recent

winning streak of London's FTSE100 Index. The FTSE has now risen for 14

trading days in a row and on 18 of the past 19 trading days. Streaks like

this are rare in senior stock indices.

As mentioned in last week's

Interim Update, it could become evident very early in the coming

correction as to whether we are dealing with a minor pullback or a 10%-15%

decline.

While the FTSE is extremely 'overbought' on a short-term basis, on a

long-term basis it has only just broken above the top of a base that has

been 17 years in the making. The break above long-term resistance could be

signaling that a 2-3 year cyclical advance has begun, or it could be a

'head fake'. It would be prudent to assume the former until/unless proved

otherwise.

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date |

Description |

|

Monday January 16 |

US markets closed for public

holiday |

| Tuesday

January 17 |

No important events scheduled |

|

Wednesday January 18 |

CPI

Industrial

Production

Beige Book

TIC Report |

|

Thursday January 19 |

Housing Starts

Philadelphia Fed Business Outlook Survey |

|

Friday January 20 |

No important events scheduled |

Gold and the Dollar

Gold

Last week the US$ gold price reached resistance in the low-$1200s. This was/is

our minimum target for the rally that began in December and is likely to end

during the first quarter of this year. That the minimum target was reached so

early in the quarter and with no significant intervening pullback means that the

maximum target stands a decent chance of being reached prior to a multi-month

price peak. The maximum target is the 200-day MA, which is presently near $1270.

In wave terms, the up-move in the gold price over the past three weeks is

probably the 'A' wave of an A-B-C pattern. Next comes a pullback or

consolidation probably lasting 1-2 weeks, after which there should be a rally to

a new high for the move.

That being said, the gold market is not yet

short-term 'overbought' so an extension of the initial wave is certainly

possible.

Gold Stocks

Our target range for the

expected Q1-2017 peak in the HUI remains 220-250. As illustrated below, near 220

there is the 200-day MA in addition to lateral resistance, and at 250 there is

lateral resistance.

The

HUI has moved sideways for 6 trading days since breaking above 200 on 5th

January. Minor consolidations within short-term upward trends often last 4-8

trading days, so a quick move up to the bottom of our target range could happen

as soon as this week. However, an equally-likely outcome is that the

consolidation/correction continues for at least another week and results in a

test of the 50-day MA, which is presently at 186.

Either way, we expect a

further gain of at least 10% and potentially as much as 25% prior to a

multi-month top.

The Currency Market

The Dollar Index

The downward correction

in the Dollar Index is proceeding roughly as expected. The Index reached its

50-day MA late last week and ended the week almost exactly level with this

moving average.

In

addition to the 50-day MA, there is significant support in the 100-101 range

defined by the 2015 peaks. This will probably mean that a rebound gets underway

during the first half of this week, but we doubt that the overall correction is

complete.

The 98-99 range is, we think, a reasonable target for a

short-term bottom.

Inflation anger is on the

rise in Germany

Here's an excerpt from an

article published at www.telegraph.co.uk last week:

"The ECB

wants to inflate away the debt of the southern European countries. This is a

clear conflict of interest with net creditors like Germany," said Clemens Fuest,

president of the IFO Institute in Munich. "There is a debate building up on the

expropriation of German savers by the ECB. This is going to become very

difficult if inflation approaches 2pc and they still do nothing. People will

conclude that their true motive is redistribution," he said.

What is new

is that Germany's inflation rate has suddenly jumped to 1.7pc after a long and

deceptive period of quiescence. It is now much higher than in southern Europe.

The mechanical effect is to drive real interest rates to minus 2pc, lower than

at any time in German history other than the two hyper-inflations after the

First and Second World Wars.

Professor Clemens said the politics are

poisonous because the ECB's majority bloc is openly sweeping aside German

objections. This plays into the hands of the eurosceptic Alternative fur

Deutschland (Afd), while the ruling Christian Democrats are toughening their

line to stop a leakage of votes.

"The perception is that we are being

dominated by foreigners. This is going to become a big issue in the campaign,"

he said."

At the heart of the issue is the impossibility of

concocting a one-size-fits-all monetary policy for a group of economically,

politically and culturally disparate countries.

While all the euro-zone

countries were experiencing superficial signs of deflation there was very little

pushback against the ECB's aggressive attempts to promote "inflation", but with

a) these attempts set to extend throughout 2017, b) obvious signs of price

inflation and an artificial boom appearing in the euro-zone's largest economy

and c) Italy and some of the smaller countries still immersed in economic

depressions, a major conflict appears to be brewing.

As implied in the

above article, the longer the ECB persists with its ultra-easy monetary policy

in a misguided effort to support the weakest economies, the greater will be the

pushback from Germany. One possible outcome is that German policy-makers gain

greater influence over the ECB, leading to one or more of the

economically-weaker countries leaving the monetary union. Another possible

outcome is that the ECB continues relentlessly along its current path, prompting

Germany to leave the monetary union to avoid a severe inflation problem.

Although such an eventuality can't be ruled out, Europe's monetary union

probably won't fracture this year. There is, however, a high probability that it

will fracture within three years.

Updates

on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Company

news/developments for the week ending Friday 13th January 2017:

Company

news/developments for the week ending Friday 13th January 2017:

[Note: AISC = All-In Sustaining Cost, FS = Feasibility Study, FY = Financial

Year, IRR = Internal Rate of Return, ISR = In-Situ Recovery, MD&A = Management

Discussion and Analysis, M&I = Measured and Indicated, NAV = Net Asset Value,

NPV(X%) = Net Present Value using a discount rate of X%, P&P = Proven and

Probable, PEA = Preliminary Economic Assessment, PFS = Pre-Feasibility Study]

*Blackham Resources (BLK.AX) reported its gold

production for the December quarter, which was the first quarter of production

for its newly-commissioned Matilda/Wiluna project in Western Australia.

There was a steady increase in production from the first gold pour in

mid-October through to year-end, with 9.2K ounces being produced during the

quarter and 5K of these ounces being produced in December. That is, the

annualised production rate was 60K ounces during December.

Most

importantly, the company advised that it is on track to produce gold at an

annualised rate of more than 100K ounces during the first half of the 2017

calendar year. To be more specific, the company advised that it is on track to

meet its 64K-71K-oz production target for FY2017 (the Financial Year ending 30th

June 2017). Given that 9K ounces were produced during the first half of the

Financial Year (the past 6 months), this means that the company expects to

produce 55K-62K-ounces during the first 6 months of the 2017 calendar year.

A higher gold price is not needed for BLK's stock price to move north of

A$1.00 within the next 9 months. All that's needed is for the company to achieve

its targeted production rate and for the gold price not to move a lot lower.

*Energy Fuels (EFR.TO, UUUU) advised that the U.S.

Bureau of Land Management (BLM) has issued a final environmental impact

statement (EIS) and record of decision (ROD) for the company's Sheep Mountain

uranium project in central Wyoming. The Sheep Mountain Project is a large-scale,

formerly-producing conventional uranium mine with a 30M-pound Indicated

resource.

The Sheep Mountain project is now fully permitted, meaning that

it could now be put into production if it made economic sense to do so.

Unfortunately, at the current uranium price in the low-US$20s the project is a

long way out of the money. To be more specific, according to the April-2012 PFS

the Sheep Mountain project would probably be economically viable at a uranium

price of $50/pound and would be economically robust (42% IRR) with a uranium

price of $65/pound.

Receipt of the final Sheep Mountain permits is still

a positive development, though, because it increases EFR's upside leverage to

the uranium price. The company now has another asset that can be quickly brought

into production after market conditions become suitable.

*Premier

Gold (PG.TO) now has so many 'irons in the fire' it is difficult to

keep track of the company's progress.

The company issued three press

releases last week, the first containing exploration results/plans, the second

reporting a maiden resource estimate for the Hasaga gold project in Ontario and

the third providing an update on production. For a company such as PG,

exploration results only matter to the extent that they add to the quantity or

quality of the resource base. We'll therefore focus on the latter two press

releases.

According to an estimate compiled by an independent consultant,

PG's 100%-owned Hasaga project has a total open-pit gold resource (there is the

potential to also define an underground resource, but this is yet to happen) of

about 1.7M ounces (1.1M "Indicated" plus 0.6M "Inferred") at an average grade of

around 0.8-g/t. This is a very good start, as a 1.7M-ounce resource could

already be enough to support a significant mining operation.

At this

stage it's impossible to intelligently assign a value to the Hasaga resource,

because gold-in-the-ground can be worth anything from zero to a few hundred

dollars per ounce. For example, a gold resource that has no realistic chance of

ever being economic or ever being permitted has zero value. However, if Hasaga

were the flagship project of a microcap miner we suspect that the stock market

would currently be assigning it a value of at least US$20/oz, or US$34M (C$45M).

This equates to about C$0.20 per PG share.

With regard to progress on the

production front, the company had a very good December quarter. With 81.8K

ounces of gold produced during the final quarter the company exceeded its yearly

guidance by about 2K ounces. Specifically, its 2016 guidance was for 100K-110K

ounces of gold production and it ended up producing 112K ounces.

It

seems, however, that production was pulled forward from 2017, because the 2017

guidance has been reduced by a few thousand ounces. This year's production is

now expected to be 125K-135K ounces at an AISC of only US$660-$690/oz. A lot

will obviously depend on the gold price, but this suggests that PG's operating

gold mines will have positive cash flow in excess of US$50M during 2017.

Upcoming news of significance will be the year-end financial statements in

February and an updated resource estimate for the exploration-stage McCoy-Cove

project some time before the end of March.

At the current gold price we

think that PG would be fairly valued at around C$4/share.

*Ramelius

Resources (RMS.AX) reported December-quarter gold production of 31.3K

ounces, which is near the low end of the company's 31K-35K guidance range. We

view this production result as neutral.

Despite the production coming in

at the low-end of the forecast range, it was another quarter of strong cash

generation for RMS. The company now has no debt and A$95M of cash, which amounts

to a $6M improvement during the quarter.

With 525M shares outstanding,

net cash of A$95M and a current stock price of A$0.57, RMS has an enterprise

value of A$204M. At an A$/US$ exchange rate of 0.74, this equates to US$151M.

For a company with profitable gold production in excess of 100K ounces/year in

the world's lowest-risk mining jurisdiction, an enterprise value of US$151M is

low.

We think there's a good chance of RMS's stock price rising to A$1.00

during 2017.

*Sabina Gold and Silver (SBB.TO) had

significant news last Friday. SBB is not a current member of the TSI List, but

it is a former and potential future member.

Last June the Nunavut Impact

Review Board (NIRB) recommended to the Minister of Indigenous and Northern

Affairs Canada (INAC) that the Back River project not proceed to the next phase

of permitting. This was a major and surprising setback for SBB's flagship

project, and opened up three possibilities.

The first was that the

Minister would accept the NIRB's recommendation and effectively kill the

project. The second was that the Minister would ignore the NIRB's recommendation

and allow the project to proceed to the mine construction phase. The third and

by far the most likely was that the Minister would return the Back River project

to the NIRB for further consideration.

On Friday 13th January the most

likely of the three outcomes was confirmed. The project has been returned to the

NIRB.

There wasn't a big market reaction to the news on Friday (the stock

was up 10%) because the outcome was generally expected and because a lot of

uncertainty remains. It is reasonable to assume that the project will eventually

get permitted, but there is no telling how long it will take for SBB to satisfy

the bureaucrats at the NIRB and obtain the necessary positive recommendation. In

last Friday's press release SBB simply wrote: "Sabina will await direction from

the NIRB on how the additional review of the project is to proceed."

Given the uncertainty regarding timing, at the current price we are not

interested in owning SBB shares or returning the stock to the TSI List. However,

we might be interested at a much lower price or after the permitting schedule

becomes clearer.

*Taseko Mines (TGB) announced

December-quarter copper production of 41M pounds, bringing full-year production

to 133M pounds.

The December-quarter production result was excellent.

Combined with the higher average copper price during the quarter it should

provide a significant boost to TGB's financial position. The next look at TGB's

financial position will happen when the company's annual report is issued during

the second half of February.

While TGB's financial situation has clearly

improved and is trending in the right direction, the improvement appears to have

been largely factored into the stock price. As illustrated below, a substantial

upward re-rating has occurred.

We

will play it by ear, but as things stand today we would view a rise in TGB's

stock price to around US$1.50 as a selling opportunity. In fact, given the

magnitude of the stock's recent advance it could, for risk/money-management

reasons, be appropriate to take partial profits now.

*Timmins

Gold (TGD) reported December-quarter gold production of 25.3K ounces

and total 2016 production of 100.3K ounces. The annual output was slightly above

the top end of the company's upwardly-revised guidance range and was therefore a

good result.

As per TGD's previously-advised plan for its San Francisco

mine in Mexico, 2017 gold production is expected to be 70K-75K ounces at a cash

cost of US$900-$950/oz. This cash cost implies a total cost of at least

$1150/oz, which, in turn, implies that TGD would be doing only marginally better

than breaking even at the current gold price.

Fortunately, TGD's balance

sheet is now healthy and if it can bring its Ana Paula gold project into

production over the next couple of years it will have a much lower overall cost

profile. The FS for the Ana Paula project is expected to be complete by

mid-2017.

As previously advised, TGD's value is highly levered to the

gold price. For example, our rough estimate of fair value increases from

US$0.39/share to US$0.85/share with a rise in the gold price from $1200/oz to

$1300/oz.

List

of candidates for new buying

From within the ranks of TSI stock

selections the best candidates for new buying at this time, listed in

alphabetical order, are:

1) ALK.AX at A$0.35 or lower (last Friday's

closing price: A$0.38)

2) BLK.AX (last Friday's closing price: A$0.57)

3) ESM.TO (last Friday's closing price: C$0.85)

4) PG.TO following a

pullback to the C$2.50s (last Friday's closing price: C$2.91)

5) SCP.TO

(last Friday's closing price: C$0.54) or ADI.V (last Friday's closing price:

C$0.19). Note: These companies are merging.

Note that the above list is

limited to five stocks. It will sometimes contain less than five, but it will

never contain more than five regardless of how many stocks are attractively

priced for new buying.

Speculative

exposure to copper

In the 19th October 2016 Interim Update we

added Australia-listed Cassini Resources (ASX: CZI) to the TSI Small Stocks

Watch List (SSWL). It was trading at A$0.05 at that time and is now trading at

around A$0.057.

CZI's flagship asset is the West Musgrave nickel-copper

project in Western Australia, a project with a global resource containing about

3.8B pounds of copper and 1.8B pounds of nickel. CZI currently owns 100% of West

Musgrave, but Oz Minerals (OZL.AX) can earn 70% of the project over the coming

few years by spending A$36M and completing a feasibility study.

It's the

partnership with the financially-strong mid-tier mining company (OZL) that

attracts us. Without this partnership CZI would be just one of the many

microcaps with a large, low-grade mineral deposit. They are a dime a dozen.

With 276M shares outstanding, CZI's current market cap is only about A$16M

(US$12M). This market cap is low relative to the amount that OZL is planning to

spend on the project to earn its share and miniscule relative to the potential

value of such a large base-metals project.

The risk is that exploration

results are not good enough, prompting OZL to return the project to CZI after

spending only $3M.

Saying

farewell to an old friend

Rumours emerged late last week that

London-listed

Acacia Mining (ACA.L), a company that produces gold at the rate of around

800K ounces/year from mines in Tanzania, is in merger discussions with Endeavour

Mining (EDV.TO). The companies acknowledged that discussions had taken place,

but that no deal was currently in the works.

We won't be surprised if the

merger happens, because it appears to make sense. Assuming it was carried out as

a merger of equals (meaning: no takeover premium) it would, we think, be

slightly positive for EDV. It would be very positive in terms of in-ground

resources, slightly positive in terms of balance sheet, neutral in terms of

production and slightly negative in terms of production cost (ACA's production

cost is higher than EDV's).

If it happens, the combined company will be a

senior gold producer with a market cap in the US$4B-$5B range and annual

production of around 1.5M ounces. All of the production would come from Africa

-- about half from the west side and half from the east side.

Although

the merger might not happen and would probably be slightly positive for EDV if

it did, this news has prompted us to remove EDV from the TSI List. One reason is

that the company is getting too big with too many 'moving parts', making it

time-consuming to closely follow (we cover a lot of ground in the TSI

commentaries and therefore need to limit the amount of time we devote to any one

stock). A second reason is that we expect EDV to move in line with the overall

gold-mining sector from here on, that is, the dramatic outperformance that EDV

provided last year is unlikely to occur in the future. For example, if GDX were

to rise by 10-15% over the coming month then EDV would probably do the same.

Last Friday's closing price of C$22.83 for EDV is almost identical to the

(split-adjusted) price at which the stock was added to the List 5 years ago, so

the long-term EDV trade will go into the record books as a break-even result.

However, the majority of our buy suggestions over the years occurred when the

stock was trading at $4-$8, so most long-term TSI readers who traded the stock

probably did very well.

EDV could return to the TSI List in the future,

but probably only as a short-term trading position.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://www.barchart.com/

http://bigcharts.marketwatch.com/