![]()

![]()

![]()

![]()

-- Weekly Market Update for the Week Commencing 16th April 2018

Big Picture

View

Here is a summary of our big picture

view of the markets. Note that our short-term views may differ from our

big picture view.

The BULL market in US Treasury Bonds that began in the early 1980s ended in mid-2016, but there will be many years of topping action in bond prices and bottoming action in bond yields before major new trends get underway. A major decline in government bond prices will unfold during the 2020s. (Last update: 11 September 2017)

The stock market, as represented by the S&P500 Index, commenced a secular BEAR market during the first quarter of 2000, where "secular bear market" is defined as a long-term downward trend in valuations (P/E ratios, etc.), gold-denominated prices and inflation-adjusted prices. This secular trend will bottom in 2020 or later. (Last update: 11 September 2017)

A cyclical BEAR market in the US Dollar began in 2016-2017. (Last update: 11 September 2017)

Gold commenced a secular bull market relative to all fiat currencies, the CRB Index, bonds and most stock market indices during 1999-2001. This secular trend will peak in 2020 or later. (Last update: 11 September 2017)

Commodities,

as represented by the CRB Index, commenced a

secular BULL market in 2001 in nominal dollar terms. The first major

upward leg in this bull market ended during the first half of 2008, but

a long-term peak won't occur until 2020 or later.

(Last

update: 11 September 2017)

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

True

Fundamentals Summary

[Notes:

1) The date shown next to the current True Fundamentals Model (TFM) signal is

when the most recent change occurred. 2) Charts of the Gold and Equity

TFMs are included in the "Charts and Indicators" section of the TSI web

site]

| Market | True Fundamentals Model (TFM) |

| Gold (US$ Price) | Bearish (12 Jan 2018) |

| US Equity (SPX) | Bullish (13 Apr 2018) |

| Currency (Dollar Index) | Bullish (15 Dec 2017) |

| Commodities (GNX) | Bullish (29 Dec 2017) |

Last week's posts at the TSI Blog

Trade as a

zero sum game

The

short that keeps on giving?

Summary of current

thinking/positioning

1) A number of markets are set

up for trend reversals or accelerations, with the US$ being the linchpin.

If the DX breaks out to the downside from its recent narrow range, rallies

should begin or accelerate across the commodity world with silver bullion

and gold-mining stocks leading the way higher. However, if the DX breaks

out to the upside from its recent range then the commodity world will be

pressured downward for at least a few weeks thereafter.

2) The SPX

is about to either end its correction by completing a successful test its

early-February low (2530) or escalate the significance of the January-2018

top by breaking to a new low for the year. The former outcome is the more

likely, but there remains the threat of a trend-ending plunge to a new low

for the year.

3) There are signs that the multi-year upward trend

in commodity prices that got underway in early-2016 has resumed.

4) Government bond prices are in long-term downward trends and will go

much lower before year-end, but a counter-trend rebound is underway. We

expect the next downward leg in the bond bear market to begin within the

next few weeks, but due to the huge speculative net-short position in

10-year T-Note futures we aren't yet interested in placing a new bearish

bet.

5) Holding a cash reserve of around 30%.

A dramatic upward

reversal in US monetary inflation

In February of this year the

year-over-year rate of growth in the US True Money Supply, a.k.a. the US

monetary inflation rate, was only 2.4%. This was its lowest level since

March of 2007 and not far from a multi-decade low. In March of this year,

however, the monetary inflation rate almost doubled -- to around 4.6%.

Refer to the following chart for more detail. What caused the reversal and

what effect will it have on the economy and the financial markets?

The Fed has been slowly removing money from the economy via its QT

program, so March's money-supply surge wasn't caused by the central bank.

The main cause also wasn't the commercial banking industry, because

although there has been an up-tick in the rate of bank credit expansion

over the past month it is nowhere near enough to explain the increase in

TMS.

We can't be certain, but by a process of elimination we

conclude that the sharp upward reversal in the US monetary inflation rate

was due to money coming into the US from overseas. If so, the most likely

driver would be the repatriation of corporate profits due to the tax

changes approved near the end of last year.

In other words, it's

likely that March's TMS surge was due more to the way that the banking

system accounts for existing US dollars than an increase in the total

supply of US dollars.

If the monetary inflation reversal has more

to do with a change in the way existing US dollars are accounted for than

a sudden large increase in the pace of new dollar creation, then the

effects on the economy and the financial markets will be minimal. In any

case, after the monetary inflation rate has moved high enough for long

enough to set in motion an artificial boom, a drop to a relatively low

inflation level will inevitably lead to a bust (an economic recession and

a large decline in the stock market, often accompanied by a banking

crisis). For example, the pronounced rebound in the TMS growth rate from

Q4-2006 to Q3-2007 did not stop the recession, the equity bear market and

the banking crisis of 2007-2009.

This means that as a result of the

2017 decline in the monetary inflation rate to near a 20-year low, the die

has been cast.

The big unknown right now is the timing of the bust

that will occur in response to last year's precipitous decline in the

monetary inflation rate. Will it get underway during the second half of

this year or will it wait until next year?

Interest Rates

The on-going LIBOR surge

The relentless rise over the past few months in the London InterBank

Offered Rate (LIBOR), a short-term interest rate for interbank lending and

a popular benchmark, has garnered a lot of attention in the press.

The first of the following charts shows that 3-month LIBOR made a new

9-year high at the end of last week. The rise in LIBOR is mostly a

reflection of the general rise in short-term interest rates, although the

second of the following charts suggests that there is a little more to it.

The second chart shows that the spread between 3-month LIBOR and the

3-month T-Bill yield has moved up to the top of its narrow 9-year

horizontal range. In other words, the main 3-month interest rate used by

banks when trading with each other has risen relative to the 3-month

interest rate paid by the US government.

We think that the rise in the LIBOR-TBill spread has the same primary

cause as the recent surge in US TMS: changes in US tax regulations that,

among other things, have created a short-term incentive for money to flow

into the US. Some of the money that US corporations had loaned to banks

outside the US has been removed from this market, forcing the banks to

offer higher interest rates to attract short-term funding.

Therefore, it seems to us that the rise in the LIBOR-TBill spread and

other LIBOR spreads is NOT a signal that a banking crisis is brewing.

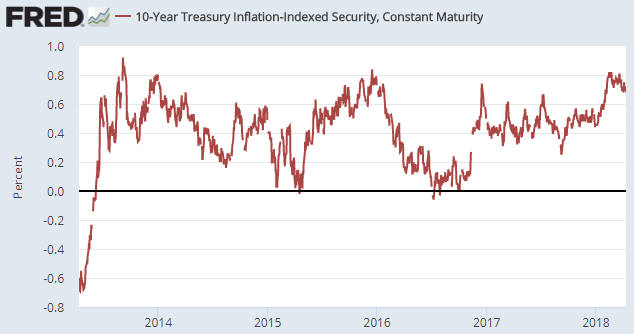

The 'real' interest rate remains range-bound

The yield on the 10-year TIPS (Treasury Inflation-Protected Security) is a

proxy for the real US 10-year interest rate. It is, in effect, the nominal

10-year interest rate minus the expected change in the CPI.

As

illustrated below, since mid-2013 the 10-year TIPS yield has oscillated

between 0% and 0.8%. It has recently turned down after touching the top of

this range, but remains near a 5-year high.

If the 10-year TIPS yield were to break upward from its multi-year

range it would put significant and potentially irresistible downward

pressure on the prices of gold, commodities and equities, but over the

next few months the real interest rate will more likely trend downward

than break out to the upside. This will be due to inflation expectations

rising faster than nominal interest rates.

Oil

Oil negates the

double-top scenario

The oil price ended the week before

last at the bottom of a 2-month channel, having potentially completed a

double top near $66. Last week, however, it invalidated the double top

idea by breaking above its January and March highs. It also reached the

top of its short-term channel, so don't jump to the conclusion that the

break above lateral resistance implies significant additional gains.

We now view oil's price action as neutral. At the same time, the

sentiment situation remains bearish (the total speculative net-long

position in oil futures remains near an all-time high) and, as discussed

below, the fundamentals remain bullish. The oil market is therefore a

'mixed bag'.

Oil fundamentals stay bullish

It's worth repeating that for an industrial commodity with a large and

liquid futures market, such as oil, the "term structure" in the futures

market (a.k.a. the futures curve) is the most reliable indicator of the

supply-demand situation.

An upward-sloping futures curve is called

"contango" and is the normal state of affairs. In this normal state of

affairs a more distant futures contract will have a higher price because

of the cost of storage and financing, not because traders expect the price

to be higher in the future.

When the curve flattens in most cases

it means that the physical supply situation is getting tighter. This is

because if the gap between a futures price and the spot price falls to the

point where it is less than the cost of storage, then a risk-free

arbitrage opportunity will be presented to the owners of physical supply.

They can sell their physical oil, buy the futures and make a guaranteed

profit equal to the cost that they would have paid for storage minus the

difference between the futures price they paid and the spot price they

received.

Sometimes the futures curve doesn't just flatten, it

inverts; that is, the curve becomes downward-sloping. This is called

backwardation. When the oil market is well into "backwardation" it means

that a substantial risk-free profit is being offered to the owners of

physical supply who are able to do the trade described above.

Since

risk-free profit opportunities tend to be fleeting, the only way that

"backwardation" can be sustained is if very few owners of physical supply

are in a position to do the trade described above. In other words,

sustained "backwardation" implies a market with minimal surplus supply,

either because inventory levels are low or because the current owners of

the physical supply are unwilling to relinquish ownership even when

presented with a large financial incentive to do so.

Here are four

charts that show the change in the oil market's futures curve over the

past ten months. The first chart shows the situation at 20th June 2017.

This is a picture of a normal, well-supplied market. The second chart

shows the situation at 16th August 2017, by which time the curve had

flattened markedly. This implies that oil's supply situation tightened

between 20th June and 16th August, 2017, but the fact that the curve still

had an upward slope suggests that there was no shortage in mid-August of

last year. The third chart shows the situation at 8th November 2017. This

is a picture of a market in which you get paid significantly more to

deliver a barrel of oil today than to store the barrel and deliver it a

year from now, which implies a significant supply shortage. The fourth

chart shows the current situation. It indicates that the fundamental

supply-demand situation is even more bullish now than it was in

early-November of last year.

Oil's fundamentals are unequivocally bullish, but speculative

sentiment is very extended into optimistic territory. This has been the

case for many months now. The sentiment situation keeps warning "high risk

of a significant price decline" while the fundamental situation keeps

saying "a downward price correction could occur, but it won't get very

far".

The Stock Market

A "Dow Theory" sell signal

occurs when both the Dow Industrials Index (INDU) and the Dow

Transportation Average (TRAN) experience significant initial declines from

their highs, rebound to lower highs and then close below the closing lows

of their initial declines. Such a signal was generated last Monday (9th

April) when TRAN closed marginally below its 9th February low, INDU having

already closed below its February low during the second half of March.

Here's a picture of the recent Dow Theory sell signal:

Is the Dow Theory sell signal an important development?

The

answer is no; it's meaningless. Even if there had been follow-through to

the downside, Dow Theory signals are not reliable indicators of the

future. And as things currently stand there has been no follow-through to

the downside. Both the INDU and the TRAN ended last week above their

breakdown levels.

While the TRAN is definitely worthy of our

attention, the NASDAQ100 Index is vastly more important these days. As

illustrated below, the NASDAQ100 Trust (QQQ) has not yet closed below, or

even traded below, its early-February closing low.

The evidence continues to support the bull-market correction scenario.

In fact, the evidence in support of this scenario increased last week due

to our Equity True Fundamentals Model (ETFM) shifting from bearish to

bullish. This shift was caused by a contraction in credit spreads and a

decline in the 10-year TIPS yield.

Our own account now has two

small bearish speculations, both of which will be kept on a tight leash.

We have some QQQ June-2018 put options that will be exited if QQQ achieves

consecutive daily closes above its 50-day MA and some Tesla (TSLA)

June-2018 put options that will be exited if TSLA achieves consecutive

daily closes above $310.

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date | Description |

| Monday Apr-16 |

Retail Sales Business Inventories Housing market Index TIC Report |

| Tuesday Apr-17 |

Housing Starts Industrial Production |

| Wednesday Apr-18 | Fed's Beige Book |

| Thursday Apr-19 | No important events scheduled |

| Friday Apr-20 | No important events scheduled |

Gold and the Dollar