![]()

![]()

![]()

![]()

-- Weekly Market Update for the Week Commencing 16th October 2017

Big Picture

View

Here is a summary of our big picture

view of the markets. Note that our short-term views may differ from our

big picture view.

The BULL market in US Treasury Bonds that began in the early 1980s ended in mid-2016, but there will be many years of topping action in bond prices and bottoming action in bond yields before major new trends get underway. A major decline in government bond prices will unfold during the 2020s. (Last update: 11 September 2017)

The stock market, as represented by the S&P500 Index, commenced a secular BEAR market during the first quarter of 2000, where "secular bear market" is defined as a long-term downward trend in valuations (P/E ratios, etc.), gold-denominated prices and inflation-adjusted prices. This secular trend will bottom in 2020 or later. (Last update: 11 September 2017)

A cyclical BEAR market in the US Dollar began in 2016-2017. (Last update: 11 September 2017)

Gold commenced a secular bull market relative to all fiat currencies, the CRB Index, bonds and most stock market indices during 1999-2001. This secular trend will peak in 2020 or later. (Last update: 11 September 2017)

Commodities,

as represented by the CRB Index, commenced a

secular BULL market in 2001 in nominal dollar terms. The first major

upward leg in this bull market ended during the first half of 2008, but

a long-term peak won't occur until 2020 or later.

(Last

update: 11 September 2017)

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

True

Fundamentals Summary

[Notes:

1) The date shown next to the current True Fundamentals Model (TFM) signal is

when the most recent change occurred. 2) Charts of the Gold and Equity

TFMs are included in the "Charts and Indicators" section of the TSI web

site]

| Market | True Fundamentals Model (TFM) |

| Gold (US$ Price) | Bullish (13 Oct 2017) |

| US Equity (SPX) | Bullish (25 Sep 2017) |

| Currency (Dollar Index) | Bearish (19 May 2017) |

| Commodities (GNX) | Bullish (05 May 2017) |

Last week's posts at the TSI Blog

Blatant statistical bias: Gun ownership vs. gun deaths

Updating gold's true fundamentals

Summary of current

thinking/positioning

1) Neutral while awaiting

clearer signals on the short-term prospects for gold and the associated

mining indices.

2) With the stock market having got through the

bulk of a risky seasonal period with minimal volatility, no longer

anticipating a tradable short-term decline.

3) Looking for

opportunities to increase exposure to industrial-commodity (base metals,

O&G) stocks.

4) Expecting the Dollar Index to resume its rebound

following a brief consolidation.

5) Anticipating significant

additional short-term weakness in the commodity currencies (the C$ and the

A$).

6) Thinking that the T-Bond has commenced an intermediate-term

decline and that rebounds should be viewed as opportunities to expand a

bearish position.

7) Maintaining a cash reserve of about 35%.

The US monetary

inflation rate continues to plunge

The Fed's monetary data for

September indicate that the year-over-year rate of growth in US True Money

Supply (TMS) has dropped to only 3.3%. This is the lowest since

April-2007, meaning that it's a 10-year low. As recently as last November

it was in double digits, so the decline has been steep. Here's the

relevant chart:

According to our theory, the plunge in the US monetary inflation rate

to a low level won't pose a major threat to asset prices or the global

economic boom as long as it is offset by rapid monetary inflation in the

euro-zone. Up until now it has been, but only just.

The ECB's

monetary data for September won't be available until late October, at

which time we'll find out if euro-zone monetary inflation is still

sufficient to offset the decline in US monetary inflation.

The T-Bond has

rebounded. What now?

The iShares 20+ Year Treasury

ETF (TLT), our favourite proxy for long-dated US Treasury securities, has

rebounded from an early-October low near its 200-day MA to slightly below

its 50-day MA. This could mean that the expected counter-trend rally is

complete and that a decline to a new multi-month low is about to begin,

but it's also possible that the rebound is only about half complete and

that some consolidation within the coming week or two will be followed by

an extension to the vicinity of the early-September high. Each of these

possibilities would be consistent with our intermediate-term bearish

outlook for this market.

We can't possibly know whether TLT's rebound is complete, but we do

know that last week's price action has created a better opportunity to buy

TBT (a leveraged fund that moves in the opposite direction to TLT) than

existed a week earlier. We suggest averaging into TBT during periods of

short-term T-Bond strength over the remainder of this year in preparation

for a large T-Bond decline during the first half of next year.

As

well as being a reasonable speculation in its own right, anyone with

significant exposure to gold could view a bet against the T-Bond as a

hedge against gold-price weakness. The reason is that at a time when US

inflation expectations are stable the US$ gold price will tend to move in

the same direction as the T-Bond price (in the opposite direction to

long-term interest rates). This relationship is evidenced by the following

chart comparison of the US$ gold price and TLT.

Commodities

Cost of the futures roll

Here's a chart of the natural gas (NG) continuous futures price

covering the past 8 years and 2 months. This time span was chosen because

it is a long period during which the NG price essentially went nowhere (8

years and 2 months ago the NG price was roughly the same as it is today).

Now, here's a chart of

UNG (the United States Natural Gas Fund) covering the same period. UNG

is an ETF that invests in NG futures.

The eagled-eyed will spot a difference between the above charts. The

difference, in a nutshell, is that a fund that invests in NG futures lost

about 93% of its value over a period in which the NG futures price was

unchanged.

Here's a chart that illustrates the extent to which UNG

has underperformed the commodity it is supposed to be tracking.

Part of UNG's relatively poor performance can be explained by the

fund's expenses, but the total expense ratio is only 1.27% and a 93% loss

over slightly more than 8 years equates to a compounded loss of about 30%

per year. The cost of managing the fund therefore explains almost nothing.

Almost all of the underperformance is due to the futures roll. In

other words, the price of UNG has been in a relentless downward trend

relative to the price of the underlying commodity due to the ETF's regular

requirement to roll from an expiring futures contract into the next

available contract. In the US natural-gas futures market it is normal for

the next contract to be priced at a premium to the expiring contract, so

UNG is having to consistently sell low and buy high.

UNG's

performance is an extreme example of what will happen to any ETF that

holds futures contracts* in a market that is usually in short-term

contango (nearer contracts cheaper than more distant contracts). An even

more extreme example is VIXY, a fund that holds Volatility Index futures

contracts. It is still possible to make money by going long such funds,

but the timing of both entry and exit has to be very accurate.

If

you own a commodity futures ETF at a time when the underlying market is in

short-term backwardation (nearer contracts priced higher than more distant

contracts) then the futures roll will work in your favour, because when

the ETF does 'the roll' it will be selling at a higher price than it is

buying. However, most commodity futures markets are in contango most of

the time.

*This issue does not apply to

commodity ETFs that hold the physical commodity.

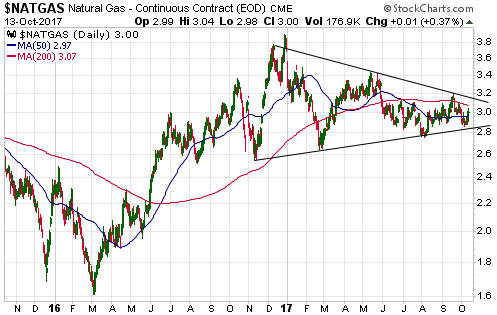

Natural Gas

The NG price has done worse than we thought it

would during this year to date. Instead of adding to the gains achieved

during March-December of last year it has oscillated within a contracting

range.

We don't have a strong opinion on what will happen to the NG price

over the months ahead. The price pattern is neutral and the amount of NG

in storage (see chart below) is close to its 5-year average for this time

of the year, so the supply situation is also neutral. All we can say is

that a daily close above $3.20 would suggest that an intermediate-term

rally had begun and that a daily close below $2.75 would warn of

significant downside potential.

At this time our only exposure to natural gas is via a long-term

position in Petrus Resources (PRQ.TO), a junior Canadian NG producer.

Although PRQ's stock price has performed similarly to the NG price during

this year to date and although the company would benefit from a higher NG

price, we don't expect the stock price to consistently track short-term

moves in the commodity price.

The Grains

In 2016 the prices of soybeans,

corn and wheat made 5-year lows. They rallied from those lows and then

gave back the bulk of their gains. In each case, the decline to a higher

low could be part of a long-term basing process. After the long-term base

comes the new multi-year upward trend.

Here are the relevant

charts:

Exposure to "the grains" can be obtained via JJG or GRU -- ETNs that

track indices comprising soybean, corn, wheat and soybean-oil futures. The

tracked indices are adversely affected by the "futures roll", which is why

the ETNs recently made new bear-market lows. However, the effect of the

"futures roll" is not as pronounced with JJG and GRU as it is with UNG.

Here's a chart of GRU:

The Stock Market

Nothing matters except

the story

This year has been difficult for anyone

employing a value-oriented approach to selecting stocks and other assets,

because it seems that nothing has mattered except the story. In general,

investors (using the word as loosely as possible) have flocked to assets

with interesting stories regardless of valuation and have ignored assets

that by traditional measures offer good value.

Examples are easy to

find within all sectors of the stock market. They include:

1)

Shopify (SHOP), a loss-making e-commerce company that trades at 18-times

revenue and 450-times next year's imagined profit. E-commerce is great for

consumers and makes for an enticing story due to the potential growth, but

it tends to be either a low-margin or a no-margin business. Just look at

Amazon.com (AMZN). Rarely has any company dominated an industry the way

that AMZN dominates on-line shopping, and yet its on-line shopping

business has never been consistently profitable. But who cares about

profits when the story is exciting!

2) Tesla (TSLA), the manufacturer of electric cars and batteries.

Great product, great story, terrible business. It's likely that within

five years TSLA will declare bankruptcy or get bought at a low price by

another car manufacturer, but that hasn't prevented 'investors' from

valuing the company at about 12 times book value.

TSLA's price

chart is beginning to look bearish, so perhaps in this case reality is

about to strike.

3) Novo Resources (NVO.V), an early-stage gold miner exploring a large

land package in the northern part of Western Australia. This company is

yet to discover anything substantial, but it is being valued by the stock

market at C$1.1 billion due to an appealing story (the story that it

might, just might, discover something big).

4) Garibaldi Resources (GGI.V), an early-stage minerals explorer that

was trading below C$0.20/share three months ago and on Friday 13th October

traded as high as C$4.20. The reason for the 2500% price increase? A good

story! The company is yet to report its first drill result, but there's

the possibility that it might, just might, have discovered something

valuable.

However, the best examples of nothing mattering except the story are

to be found outside the stock market. We are referring to Bitcoin and the

hundreds of other cryptocurrencies that have been assigned high

valuations.

Assigning high valuations to good stories regardless of

valuation is evidence of a mania. The vast majority of these stories will

end up worthless, but speculators should keep in mind that in the

short-term there is more money to be made by going long the good stories

than accumulating assets that offer good value.

Current

Market Situation

There is often a volatility spike during

the September-October period. This year, however, not only has there been

no volatility spike to speak of during this period to date, there has been

an uncommon lack of volatility. This is evidenced by the VIX having just

spent 5 weeks oscillating between 9.0 and 10.5.

Most stock indices

are now short-term 'overbought', not just in the US but throughout the

world. However, the warning signs that were apparent during August and the

first half of September have since disappeared.

At the start of

last week one of the remaining reasons to anticipate a significant

short-term decline was the precarious position of the NASDAQ100 Index

(NDX). We are referring to the fact that a week ago this influential index

was poised at the top of its 'rising wedge'. That's no longer an issue,

though, because the NDX broke through the top of its 'wedge' last week

(see chart below). There could be a breakout failure this week, but as

things stand today there is nothing in the price action to suggest that

anything more bearish than a routine pullback is about to happen.

A 1-2 week pullback to address the 'overbought' condition could begin

at any time, but a larger decline does not appear to be in the offing.

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date | Description |

| Monday Oct-16 | Treasury Budget |

| Tuesday Oct-17 |

Import and Export Prices Housing Market Index Industrial Production TIC Report |

| Wednesday Oct-18 |

Housing Starts Beige Book |

| Thursday Oct-19 | Philadelphia Fed Business Outlook Survey |

| Friday Oct-20 | Existing Home Sales |

Gold and the Dollar