-- Weekly Market Update for the Week Commencing

16th November 2015

Big Picture

View

Here is a summary of our big picture

view of the markets. Note that our short-term views may differ from our

big picture view.

The BULL market in US Treasury Bonds

that began in the early 1980s ended in early-2015, but there will be many years

of topping action in bond prices and bottoming action in bond yields before

major new trends get underway. (Last update: 29 June 2015)

The stock market, as represented by the S&P500 Index,

commenced

a secular BEAR market during the first quarter of 2000, where "secular

bear market" is defined as a long-term downward trend in valuations

(P/E ratios, etc.) and gold-denominated prices. This secular trend will bottom sometime between 2018 and 2020.

(Last update: 29 June 2015)

A secular BEAR market in the

US

Dollar

began during the final quarter of 2000 and ended in July of 2008. This

secular bear market will be followed by a multi-year period of range

trading.

(Last

update: 09 February 2009)

Gold commenced a

secular bull market relative to all fiat currencies, the CRB Index,

bonds and most stock market indices during 1999-2001.

This secular trend will peak sometime between 2018 and 2020.

(Last update: 29 June 2015)

Commodities,

as represented by the CRB Index, commenced a

secular BULL market in 2001 in nominal dollar terms. The first major

upward leg in this bull market ended during the first half of 2008, but

a long-term peak won't occur until 2018-2020.

(Last

update: 29 June 2015)

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Outlook Summary

Market

|

Short-Term

(1-3 month)

|

Intermediate-Term

(6-18 month)

|

Long-Term

(2-5 Year)

|

|

Gold

|

N/A |

Bullish

(26-Mar-12) |

Bullish

|

|

US$ (Dollar Index)

|

N/A |

Neutral

(22-Jun-15) |

Neutral

(19-Sep-07) |

|

US Treasury Bonds (TLT)

|

N/A |

Bearish

(19-Oct-15)

|

Bearish |

|

Stock Market

(DJW)

|

N/A |

Neutral

(05-Oct-15) |

Bearish

|

|

Gold Stocks

(HUI)

|

N/A |

Bullish

(23-Jun-10) |

Bullish

|

|

Oil |

N/A |

Neutral

(26-Oct-15) |

Bullish

|

|

Industrial Metals

(GYX)

|

N/A |

Neutral

(09-Nov-15) |

Bullish

(28-Apr-14) |

Notes:

1. Our short-term expectations are discussed in the commentaries, but except in

special circumstances we won't attempt to assign a "bullish", "bearish" or

"neutral" label to these expectations.

2. The date shown below the current outlook is when the most recent outlook change occurred.

3. "Neutral" means that we think risk and reward are roughly in balance with respect to the timeframe in question.

4. Long-term views are determined almost completely by fundamentals and intermediate-term views

are determined by a combination of fundamentals, sentiment and technicals.

Last week's posts at the TSI Blog

Martin Armstrong botches a critique of Austrian Economics

A great crash is

coming!

Why hasn't the Fed's QE caused "inflation"?

Manufacturing versus

Services

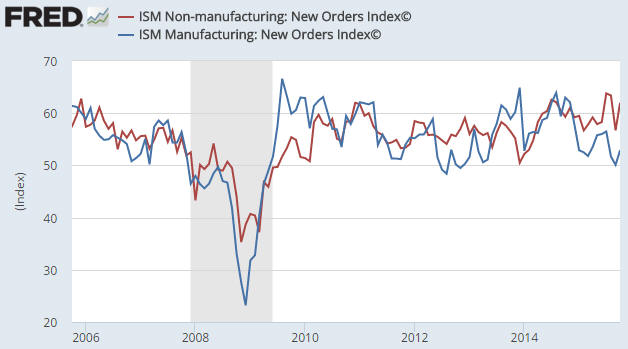

A year ago, both the ISM

Manufacturing New Orders Index and the ISM Non-Manufacturing (that is, services)

New Orders Index were near 10-year highs. Today, the services index is still

near a 10-year high whereas the manufacturing index has dropped back to near the

bottom of its 5-year range. Refer to the following chart for details. What does

this divergence mean?

Apart from the obvious (service businesses are generally doing better than

manufacturing businesses), we think it means that the US economy is less likely

to head into recession within the next three months than would be the case if

both the manufacturing and non-manufacturing indices were near the bottoms of

their 5-year ranges. That being said, if conflict arises between these two

indicators of economic performance, the manufacturing index's signal is likely

to be the more accurate. For example, if the manufacturing new-orders index were

to drop to 48 or lower we would take it as a reliable signal that the US economy

had entered or was about to enter recession territory, regardless of what the

non-manufacturing new-orders index happened to be signaling at the time.

The reason is that even nowadays, manufacturing is the foundation of the US

economy. To put it another way, although the services-oriented industries are

now a large part of the economy, these industries are built on a manufacturing

base. If the base becomes very weak, the entire structure will eventually become

very weak.

The bottom line is that in looking for evidence that the US economy has entered

or is about to enter recession, we will continue to focus on the manufacturing

numbers. At the moment the numbers that have proven to be the most reliable

recession indicators are saying that the economy is lacklustre, but not in

recession.

The Stock Market

Comparisons that make sense

Comparisons between the current situation and 2007-2008 are misguided. The main

reason is that the monetary backdrop is very different. The monetary backdrop is

critical, because the sort of 'liquidity crisis' that characterised the dramatic

2007-2008 stock-market decline is virtually impossible under current monetary

conditions. Also, it is extremely unlikely that the next bear market will follow

the path of the one that is freshest in everyone's minds.

If the US stock market is in the process of transitioning into a cyclical

bearish trend, then the early-1970s, the late-1970s and the early-2000s are

potentially-valid comparisons. Currently, the greatest fundamental similarities

appear to be with the early-2000s, in that in 2000 the US economy was widely

viewed as a bastion of strength, the US$ was strong, the stock market was being

boosted by the performances of a relatively small number of high-market-cap tech

stocks, and the Fed was just beginning to tighten monetary policy.

Interestingly, if we line up the March-2000 top with the July-2015 top we also

find price-action similarities with the early-2000s.

Lining up the March-2000 and July-2015 tops is what we've done in the following

chart. Taking this chart literally suggests a short-term bottom within the

coming fortnight and then a rally that culminates with a successful test of the

high near year-end.

On the other hand, if the US stock market is still immersed in a cyclical

bullish trend then potential comparisons are 1986, 1997-1998 and 2011.

Current Market Situation

The SPX pulled back sharply last week. We wouldn't have been surprised if the

200-day MA had offered support for a few days on the way down, but it didn't.

Instead, this MA was decisively breached on Thursday and there was

follow-through to the downside on Friday.

Our view has been that regardless of whether or not the cyclical bull market

ended a few months ago, a decline that retraces at least half of the

September-October rally was likely to happen in November. At this time we see no

reason to change our view.

An exact 50% retracement would take the SPX down to 1994, but there is support

at around 2000 that could limit the decline. There is also a not-insignificant

risk that a lot more than half of the preceding rally will be retraced before a

short-term bottom is in place, although very little chance that the

August-September lows will be breached between now and year-end.

The Dow Transportation Average (TRAN), the US stock market's leader to the

downside over the past 12 months, ended Friday's session at the support level we

mentioned in last week's Interim Update. TRAN should soon confirm the overall

market's downward reversal by closing below this support.

It's a good bet that an effort to rally the market will begin during the first

half of this week, although given the news backdrop (the horrific attacks in

Paris on Friday night) we certainly wouldn't bet on an immediate turnaround. The

effort to get a rally going will be led by hedge funds that now have a vested

interest -- having piled into long positions over the past few weeks in a

desperate attempt to rescue their annual results -- in a strong stock market.

However, any rally in the SPX that begins without a preceding drop to 2000 or

lower will probably fail within a few days at no higher than the 200-day MA and

be followed by a decline to new multi-week lows.

What to do?

Traders with short-term bearish positions (put options, for example) should look

for opportunities to exit over the next two weeks, beginning on Monday if there

is downward acceleration in reaction to the latest economic and political

developments. Just as the best times to exit bullish positions are when the

future looks incredibly bright and the average investor doesn't have a care in

the world, the best times to exit bearish positions are when the future looks

bleak and there is panic in the air.

We have a stock market put-option position. Our intention is to sell at least

half of this position if the market falls sharply during the first hour of

trading on Monday and to hold the full position if the market immediately begins

to rebound. As noted above, a rally that begins without a preceding drop to 2000

or lower on the SPX probably won't get very far.

The next good opportunity to enter bearish speculations will probably arrive

during the second half of December.

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date |

Description |

| Monday

Nov 16 |

Empire State Mfg Survey |

| Tuesday

Nov 17 |

CPI

Industrial Production

TIC ReportHousing Market

Index |

| Wednesday

Nov 18 |

Housing Starts

FOMC Minutes |

| Thursday

Nov 19 |

Philadelphia Fed Business

Outlook Survey

Leading Economic Indicators |

| Friday

Nov 20 |

No important events

scheduled |

Gold and the Dollar

Gold

Gold COT Reality

Proponents of the story that the gold market is dominated by a grand,

never-ending price-suppression scheme will often point the finger of blame at

the bullion-bank commercial traders whenever there's a sizable decline in the

gold price. In doing so they are obviously reliant on their readers/followers

being poorly informed, since the bullion-bank commercials (the largest

"commercial" operators in gold futures) are almost always net buyers during

periods of significant price weakness. For example, during the sharp price

decline of the past three weeks the "commercials" operating on the COMEX

substantially reduced their collective net short position in gold futures

contracts, that is, the "commercials" were substantial net buyers of gold

futures contracts. Furthermore, the net-buying on the part of the "commercials"

started as soon as the price began to decline.

The reality is that IF the futures market was the driving force behind the

recent sharp pullback in the gold price, the price decline MUST have been driven

by speculative selling. There is no other possibility.

The word "if" is capitalised in the preceding paragraph because while the recent

sharp pullback was probably driven by speculative selling in the futures market,

we can't know for sure that this was the case. What we mean is that we can't

rule out the possibility that the decline was driven by selling in the physical

market.

It is of little consequence to us whether a move in the gold price is led by the

physical market or the futures market. In fact, we question whether it serves

any useful purpose to view the physical and futures markets as being separate.

However, analysing the physical and "paper" gold markets as if they were

separate has certainly become a popular endeavour.

We've noticed that the proponents of the gold-suppression story will usually

attribute a rally in the gold price to physical buying and a decline in the gold

price to "paper" selling, but please understand that they have no way of

actually knowing which market was the driver. More to the point, they generally

have no way of even hazarding an educated guess, because they rarely look where

they should be looking for clues. The fact is that the only definitive indicator

of whether a price move was driven by the physical market or the futures market

is the change in the spread between the spot price and the futures price,

although a rapid change in speculative positioning in the futures market can

also be a clue.

Instead of tracking an indicator that could possibly give them the information

they desire, it seems that the aforementioned storytellers usually just make

guesses and 'support' these guesses by citing irrelevant news/data such as the

number of gold coins being bought by the US public or the amount of gold being

imported by China. As long as it can be shown that someone is buying, their

conclusion is that the physical market is strong. Since someone is always

buying, their conclusion is always that the physical market is strong and,

therefore, that any meaningful price decline must have been caused by the

selling of paper gold.

Current Market Situation

The COT data for 10th November will be interesting, because it will show what

happened to speculative positioning in the gold market in reaction to the strong

US employment numbers that were announced on 6th November. The COT data would

normally have been published by the CFTC on Friday 13th November, but due to a

federal holiday on 11th November the publishing date has been delayed to 16th

November (we know, it doesn't make sense, but this is a government department we

are dealing with). If it turns out that the change in speculative positioning

indicated by the 10th November numbers is large enough to be important then

we'll send out an email with our related comments on Monday-Tuesday.

The US$ gold price has now fallen on 12 of the past 13 and 19 of the past 22

trading days, an extraordinary short-term streak. However, the decline has lost

momentum and last week's price action was mostly uneventful. The only noteworthy

development last week was Thursday's spike down to the July low. This could turn

out to have been a successful test of the July low, but no conclusions can be

drawn at this time.

Our view continues to be that the start of the next tradable gold rally is

probably still at least a month away, with the days around the 16th December

FOMC announcement currently being the most realistic time window (for a rally

start). In the interim we expect that there will be a 1-2 week rebound.

Gold Stocks

Current Market Situation

As was the case with gold bullion, last week's performance by the HUI was

uneventful. The HUI performed slightly better than gold (it moved sideways while

the gold price fell $6), but there is no evidence that a short-term bottom is in

place or even that a 1-2 week rebound has begun.

There is no change in our short-term outlook. We suspect that a rebound over the

coming 1-2 weeks will be capped by the 50-day MA (near 120) and that a test of

the September low will occur in December.

Due to a deal announced last week, a brief note about Kinross Gold (KGC) is

appropriate.

KGC announced the acquisition of two Nevada-based gold-producing assets from

Barrick Gold. These assets came at a total cost of US$610M and are expected to

add 430K ounces/year to KGC's production (annual production will increase from

around 2.6M ounces to around 3M ounces). KGC has ample cash on hand to fund the

purchase.

Prior to this deal KGC offered the best value among the senior gold stocks. As a

result of this deal KGC's relative value is even better. Furthermore, its

country/political risk will decline due to the addition of production in a

low-risk jurisdiction.

We thought that KGC would rebound to its 200-day MA (but not much further)

during September-October, which it did. It has since declined with the overall

sector and stands a good chance of making a higher low within the next several

weeks.

We will be on the lookout over the weeks ahead for a new opportunity to

establish a trading position in KGC.

What to do?

The significant sector-wide decline of the past three weeks has taken almost all

gold-mining stocks down.

With many of the lowest-risk stocks having again reached the bargain basement

and with there not yet being any evidence that a short-term bottom is in place,

the lowest-risk stocks should be the primary focus of any new buying on the part

of intermediate-term and long-term traders who currently do not have much

exposure to gold mining (those who already have substantial exposure should

probably wait for evidence of a short-term bottom before doing any new buying).

With regard to the TSI Stocks List, this means that most new buying should

currently be directed towards stocks with a Risk Rating of 1 or 2.

Short-term traders should not do any buying until there is evidence that a

short-term bottom is in place.

The Currency Market

The Yuan

Aside from a small official devaluation in August, China's government has been

propping-up its currency (the Yuan) relative to the US$ over the bulk of the

past 12 months. That is, China's government has acted to prevent its currency

from doing what it would otherwise have done, which is to weaken relative to the

US$.

Yuan strength would normally be perceived as a disadvantage by the Keynesians

and mercantilists making government policy in China, but there are two reasons

to believe that China's apparatchiks have done what they needed to do to create

a stronger Yuan over the course of this year. One reason is to discourage

capital outflows, which reached problematic levels over the past several months.

The other reason is to smooth the way for the Yuan's inclusion in the IMF's

Special Drawing Rights (SDR).

Late last week IMF staff recommended that the Yuan be included in the SDR

basket, alongside the US dollar, the euro, the British pound and the Yen. This

almost certainly means that the IMF's executive board will approve the Yuan's

inclusion in the SDR when it meets on 30th November. That is, the Yuan's

inclusion in the SDR basket is now pretty much a done deal. What does this mean

from a practical investing/trading perspective?

Not much, because this development won't significantly alter global Yuan demand.

The reality is that no private entity cares about SDR composition when making

capital allocation decisions and that central-bank decisions regarding

international currency reserves are primarily dictated by considerations that

won't be affected by having the Yuan as part of the SDR. However, China's

leaders apparently view SDR inclusion as a badge of honour -- a symbol of

China's ascension to a position of global power.

Because the Yuan's insertion into the SDR will not significantly alter the

demand for this currency, it will probably not lead to strength in the Yuan

beyond a possible short-lived reaction to the news. In fact, it will probably

lead to a weaker Yuan. The reason is that having done what was needed to attain

the prestige that goes along with being part of a very exclusive club, China's

senior policy-makers won't be so concerned in the future about propping-up their

currency.

The Dollar Index

The Dollar Index ignored last week's stock market decline and appears to be

heading for a test of its March high at 100-101. Due to the lopsided sentiment

backdrop indicated by surveys and the COT situation, we do not expect that it

will make a solid/sustained break through the March high within the next three

months.

Updates

on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Company

news/developments for the week ended Friday 13th November 2015:

Company

news/developments for the week ended Friday 13th November 2015:

[Note: AISC = All-In Sustaining Cost, FS = Feasibility Study, FY = Financial

Year, IRR = Internal Rate of Return, MD&A = Management Discussion and Analysis,

M&I = Measured and Indicated, NAV = Net Asset Value, NPV(X%) = Net Present Value

using a discount rate of X%, P&P = Proven and Probable, PEA = Preliminary

Economic Assessment, PFS = Pre-Feasibility Study]

*Almaden Minerals (AAU) published its financial statements for the

September quarter. Taking into account the balance sheet at 30th September and

subsequent spending, we estimate that AAU presently has only about C$3M of

working capital. This is probably only enough to fund the company for another

3-6 months, so it is reasonable to expect that AAU will soon raise additional

money. We suspect that it will do a $3M-$5M equity financing, but there are

other possibilities. For example, it could choose to finance itself by selling a

silver and/or gold stream linked to future production from its Tuligtic project.

*Dalradian Resources (DNA.TO) issued its financial report for the

quarter ending 30th September 2015. The report showed that the company had C$20M

of working capital at 30th September, which is down from C$33M at 30th June.

However, shortly after the end-of-quarter cutoff the company completed a C$40M

equity financing, so it should now have C$55M-$60M of working capital. This

should be more than enough to fully fund DNA through to the September-2016

estimated completion of the FS for its Curraghinalt gold project.

*Endeavour Mining (EDV.TO, EVR.AX) reported its financial results

for the September quarter. The results were satisfactory in absolute terms and

very good compared to what most other gold-mining companies have been reporting.

EDV made a profit of US$7M during the September quarter, bringing its 9-month

profit to US$57M (about US$0.11/share). However, the profit didn't alter the

balance sheet, as net debt remained at US$223M.

*Premier Gold (PG.TO) published its financial results for the

September quarter. According to these results the company had about C$79M of

working capital at 30th September, down from C$90M at 30th June. PG continues to

be in a very strong financial position.

PG previously advised that it expects to end this year with C$75M of working

capital and to end next year with about C$100M of working capital assuming an

average gold price of US$1200/oz in 2016. Next year's expected working-capital

increase is due to PG becoming a gold producer courtesy of its 40% stake in the

South Arturo project.

*Pilot Gold (PLG.TO) published its financial statements for the

September quarter. The most important number for an exploration-stage mining

company is the working capital, which in PLG's case was US$10.2M (C$13.6M) at

30th September (down from US$12.7M at 30th June). At the current rate of

spending this would be enough to fund the company for 9-12 months, although we

suspect that PLG's management will look for an opportunity to top-up the

treasury within the next 4 months.

Also, PLG announced a change of CEO. Matt Lennox-King has left and has been

replaced on an interim basis by Rob Pease. Provided that Rob Pease's appointment

really is an interim measure while a permanent replacement is sourced, this

management change is neutral. However, we would consider the change to be

negative if Pease's appointment becomes permanent, as we were unhappy with his

performance in a previous role as CEO of Sabina (SBB.TO).

*Sabina Gold and Silver (SBB.TO) published its financial

statements for the September quarter. According on these statements and the

company's press release, SBB had C$19.8M of working capital at 30th September

and will end the year with about C$17M of working capital. This suggests that

SBB is fully funded for at least the next 12 months or until a decision is made

to commence mine construction.

By the way, the fact that SBB is fully funded for the next 12 months doesn't

mean that it won't do an equity financing within the next few months. It means

that the company is not under any pressure to raise money and should therefore

not be forced to accept onerous financing terms.

The demand for SBB shares remained relatively high over the past three weeks

despite the sector-wide downturn. As a result, daily trading volume has been

greater than usual and the stock has held onto the gains achieved during the

September-October rally.

*Timmins Gold (TGD) reported results from infill and confirmation

drilling at its development-stage Ana Paula gold project in Guerrero province,

Mexico. The results were generally very good.

Ana Paula is currently undergoing a Feasibility Study that is scheduled to be

complete in mid-2016. A PEA completed last September indicates that it could be

developed into an open-pit 116K-oz/yr gold mine with an AISC of only $567/oz.

The M&I resource is 1.86M ounces, and at a gold price of $1200/oz the after-tax

NPV(5%) and the IRR are estimated to be $185M and 28.1%, respectively.

Furthermore, the economics have since improved due to TGD's acquisition of the

El Sauzal plant from Goldcorp.

The biggest problem with the Ana Paula project is its location, in that Guerrero

is a moderately high-risk province due to the large drug gangs that operate

there. However, if the security-related risk is mitigated by the company and/or

reduced by greater diligence on the part of Mexican authorities, this project

alone could be worth a multiple of TGD's current market cap.

When TGD agreed to buy the Ana Paula project in February in an all-stock deal,

we thought that it was paying far too much. This is because we were blissfully

unaware that TGD's current assets were massively overstated on its balance sheet

and that the company's flagship San Francisco mine was performing well below

plan. Now that light has been shone on the true state of TGD's balance sheet and

flagship operation, the Ana Paula purchase looks much better.

The most important short-term issue for TGD will be the renegotiation of a

US$10M loan repayment due to Sprott Asset Management on 31st December 2015. If

this loan repayment can be postponed by one year then TGD's financial situation

will be greatly improved and the stock price will probably continue the recovery

that began last week.

*UEX Corp. (UEX.TO) issued its financial report for the latest

quarter. The report showed that the company had C$5.8M of working capital at

30th September, which probably means that it currently has about C$5M.

As noted two weeks ago, the company has made an interesting acquisition that

obligates it to pay C$6.5M by the end of next year, including C$2M by the end of

this year. It will also have to fund exploration on its current projects and the

usual G&A costs, so it's a good bet that UEX will do an equity financing within

the next couple of months. Our guess is that it will raise at least C$5M in the

near future by issuing new shares.

As we wrote two weeks ago: "We think that the completion of the

aforementioned financing will create a very good opportunity for patient

speculators to take a new position or add to existing positions in UEX."

List

of candidates for new buying

From within the ranks of TSI stock selections the best candidates for new buying

at this time, listed in alphabetical order, are:

1) AKG (last Friday's closing price: US$1.58)

2) DNA.TO (last Friday's closing price: C$0.71)

3) EDV.TO at C$0.65 or lower (last Friday's closing price: C$0.67)

4) EVN.AX (last Friday's closing price: A$1.24)

5) PG.TO (last Friday's closing price: C$2.33)

Note that the above list is limited to five stocks. It will sometimes contain

less than five, but it will never contain more than five regardless of how many

stocks are attractively priced for new buying.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://research.stlouisfed.org/