![]()

![]()

![]()

![]()

-- Weekly Market Update for the Week Commencing 17th October 2016

Big Picture

View

Here is a summary of our big picture

view of the markets. Note that our short-term views may differ from our

big picture view.

The BULL market in US Treasury Bonds that began in the early 1980s ended in early-2015, but there will be many years of topping action in bond prices and bottoming action in bond yields before major new trends get underway. (Last update: 29 June 2015)

The stock market, as represented by the S&P500 Index, commenced a secular BEAR market during the first quarter of 2000, where "secular bear market" is defined as a long-term downward trend in valuations (P/E ratios, etc.) and gold-denominated prices. This secular trend will bottom sometime between 2018 and 2020. (Last update: 29 June 2015)

A secular BEAR market in the US Dollar began during the final quarter of 2000 and ended in July of 2008. This secular bear market will be followed by a multi-year period of range trading. (Last update: 09 February 2009)

Gold commenced a secular bull market relative to all fiat currencies, the CRB Index, bonds and most stock market indices during 1999-2001. This secular trend will peak sometime between 2018 and 2020. (Last update: 29 June 2015)

Commodities,

as represented by the CRB Index, commenced a

secular BULL market in 2001 in nominal dollar terms. The first major

upward leg in this bull market ended during the first half of 2008, but

a long-term peak won't occur until 2018-2020.

(Last

update: 29 June 2015)

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Outlook Summary

|

Market |

Short-Term (1-3 month) |

Intermediate-Term (6-18 month) |

Long-Term (2-5 Year) |

| Gold | N/A |

Bullish (10-Oct-16) |

Bullish |

| US$ (Dollar Index) | N/A |

Neutral (17-Aug-16) |

Neutral (19-Sep-07) |

| US Treasury Bonds (TLT) | N/A |

Bearish (19-Oct-15) |

Bearish |

| Stock Market (DJW) | N/A |

Bearish (19-Sep-16) |

Bearish |

| Gold Stocks (HUI) | N/A |

Bullish (10-Oct-16) |

Bullish |

| Oil | N/A |

Neutral (26-Oct-15) |

Bullish |

| Industrial Metals (GYX) | N/A |

Neutral (10-Oct-16) | Bullish |

4. Long-term views are determined almost completely by fundamentals and intermediate-term views

are determined by a combination of fundamentals, sentiment and technicals.

Last week's posts at the TSI Blog

Most people want price controls

The gold manipulation silliness continues

Summary of current

thinking/positioning

1) No longer hedged via put

options against short-term downside in gold and the associated mining

stocks (due to options having been exited in response to the recent price

plunge), but still hedged via a substantial cash reserve. Expecting large

gains in gold-related investments over the next two years, but not

expecting much with regard to the next 6 months.

2) Gradually

increasing exposure to non-gold commodity-related stocks during periods of

price weakness in anticipation of 2017-2018 being a very bullish period

for commodities. Thinking that the early-2016 lows could be tested prior

to the start of the aforementioned bullish period.

3) Thinking that

the US stock market has commenced a meaningful 1-2 month decline.

Positioned via QID call options and EEM (Emerging Markets ETF) put

options.

4) Due mainly to the divergence between the currency and

oil markets discussed in the 12th October Interim Update, expecting the

oil price to soon commence a tradable decline and positioned for such an

outcome via USO put options.

5) Thinking that the Yen is about to

break out to the downside, that the commodity currencies are still in

consolidation mode with a risk of testing their early-2016 lows, and that

within the next few months the British Pound will make a low of similar

magnitude to the major bottom of early-1985.

6) Maintaining a large

cash reserve in recognition of the downside risk in almost all equities

(current cash percentage is around 50%), but looking for opportunities to

reduce cash and add to gold plus commodity exposure.

The US Treasury

has been tightening monetary conditions

Since last October the

year-over-year rate of growth in US True Money Supply (TMS) has risen from

about 6.8% to about 9.6%. Putting this into perspective, 9.6% is the

fastest rate of US monetary inflation since April-2013. The acceleration

in the US money-supply growth rate has, however, partly been offset by the

US Treasury's removal of money from the economy. Curiously, while

'everyone' has been agonising over when the Fed will take its next baby

step along the tightening path, the US Treasury has been stealthily

tightening US monetary conditions.

The stealth tightening by the

Treasury was broached in a

14th September post at the TSI Blog. The crux of the matter is that

there has been a large increase since early-November of last year in the

amount of money held by the Treasury in its account at the Fed. This money

forms part of the US money supply and is therefore included in the TMS

calculation, but for all intents and purposes it has been temporarily

removed from the economy.

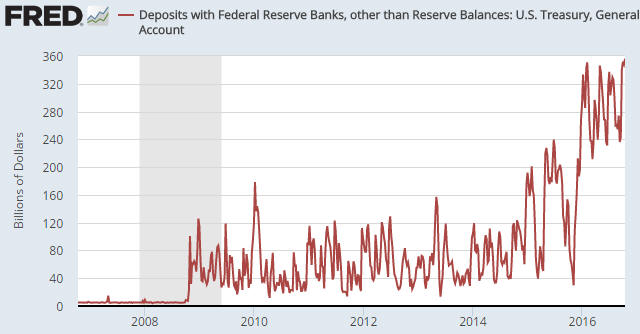

The following chart illustrates what we

mentioned in the preceding paragraph (the chart indicates the amount of

money in billions of dollars that the US federal government has on deposit

at the Fed). It shows that:

1. Prior to 2008 the Treasury's account

at the Fed was usually almost empty.

2. From late-2008 through to

late last year the amount held in the Treasury's account at the Fed

usually fluctuated between $20B and $120B, and that in early-November of

last year it was around $30B.

3. This year the amount held in the

Treasury's account at the Fed has fluctuated in a much higher range and is

currently at an all-time high of almost $360B.

In effect, the US Treasury has removed -- by not spending all the

taxes it collects or the money it borrows -- about $330B from the US

economy since early-November of last year. This is sufficient to have

caused a slowing of economic activity.

Just to be clear, creating

money out of nothing can only get in the way of real economic progress,

but it often causes a burst of activity and temporarily makes the economy

seem more vibrant. It can be likened to throwing a party in which the seed

corn is consumed. The party-goers feel great for a while...and then they

starve. By the same token, while slowing the pace at which money is

created out of nothing (that is, slowing the pace at which the seed corn

is consumed) will ultimately be helpful, in the short-term it will make

the economy seem less vibrant. In terms of short-term economic effect, the

actions taken by the US Treasury since last November are similar to

slowing the pace at which new money is created.

Conspiracy

theorists would be having a field day if the opposite had happened, that

is, if the amount of money in the Treasury's account at the Fed had fallen

by $330B over the past 11 months. They would be shouting that the account

had been drained in an effort to give the economy an artificial boost in

the lead-up to the Presidential election, thus improving the chances of a

Democrat victory. But with the incumbents having taken money OUT of the

economy in the lead-up to the election this particular theory never got

off the ground.

So what, then, is the reason for the stealth

monetary tightening conducted by the US Treasury via its account at the

Fed?

We can only guess, but it's reasonable to assume that the

slight tightening of monetary conditions was NOT an intended consequence

of the Treasury's actions. In other words, it's implausible that during

the year leading up to an election the Treasury knowingly took a course of

action that would be a short-term economic depressant.

A far more

reasonable explanation is that the action was taken for risk management

purposes. The Treasury has always lived from hand to mouth, with almost no

emergency cash. Having run out of money a couple of times over the past

few years due to inter-party haggling over the "debt ceiling", it has

probably been decided that a lot more cash should be kept in reserve.

The bond market

breaks support

The iShares 20+ Year Treasury

ETF broke below support at $133 on Friday. This breakdown suggests

short-term downside potential to $127-$128 and -- dare we say it -- is

possibly an early warning that the secular bull market in US government

bonds has ended.

The market for government bonds has been steadily weakening since

early-July. The weakening could be a routine intermediate-term correction

within an on-going bull market, but there are signs that it is something

more serious. Specifically, there are signs that it is due to a spreading

realisation that central-bank programs designed to push bond prices to

absurdly-high levels are counter-productive, and that a further

doubling-down on these programs could wreak both economic and political

havoc.

Last Friday's reaction to a Janet Yellen speech was one such

sign that the bond market is becoming increasingly wary of central-bank

promises to do more of the same. We are referring to the fact that when

Yellen speculated on Friday that the Fed might have to do more

(meaning: monetise more assets and hold interest rates lower for longer),

the T-Bond sold off and broke below support.

The T-bond price is

not going to suddenly collapse in a heap, because the Treasury market is

still widely considered to be a safe haven in times of trouble and there

will be no shortage of trouble in the future. A realistic possibility,

however, is a downward trend that gradually picks up steam over the coming

12 months.

The Stock Market

The US

The S&P500 Index (SPX) opened sharply lower last Thursday and briefly

traded below support at 2120 (the 'cliff edge') before reversing course.

It ended the day with a trivial loss and handily above the aforementioned

support. Optimism inspired by Thursday's turnaround then prompted some

follow-through to the upside during the first couple of hours of Friday's

trading session, but the gains were given back and the market ended flat

on the day.

Despite the downside breakout from a 'contracting

triangle' early in the week and significant intra-day volatility during

the final two days of the week, the SPX got through last week's challenges

without suffering much technical damage. So, what's likely to happen from

here?

One possibility is that a routine 2-month correction ended with last

Thursday's short-lived breach of support. If so, a rally to a new all-time

high is just getting underway.

It's more likely, however, that

there will soon be another test of support at 2120 with a very different

result. As previously advised, we are expecting that a breach of support

at 2120 will be followed by a quick decline to near the "Brexit" sell-off

low in the 1990s.

For anyone interested in taking a short-term

bearish position, one advantage of the current situation is that it

wouldn't take much movement in the wrong direction (upward) to show that

the position was wrong. As mentioned in last week's Interim Update, all it

would take is a daily SPX close above 2170. This makes risk management

relatively straightforward.

Emerging Market Equities

We use the Emerging Markets Equity ETF (EEM) as a commodity-market

indicator. It is useful in this regard because periods during which EEM is

strong relative to the SPX almost always coincide with periods of

broad-based strength in commodity prices. Moreover, the EEM/SPX ratio

either leads the commodity world at major turning points or can be used to

confirm a major trend reversal in commodities.

There was enough

strength in the EEM/SPX ratio during the first 8 months of this year to

signal a major reversal from down to up in the commodity world. However,

no major trend evolves in a straight line and there are signs, including

the recent divergence between the Canadian dollar and the oil price, that

at least a 1-2 month period of commodity-price weakness has begun or will

soon begin.

If we get concurrent downturns in the commodity markets

and the SPX over the weeks ahead then EEM is likely to fall in both

nominal dollar terms and relative to the SPX.

With reference to the

following chart, EEM has more-or-less traded sideways since topping in

August. It appears to have broken below the bottom of a channel that dates

back to the January low, but the important support lies at $36.00. EEM

support at $36 is equivalent to SPX support at 2120, with a decisive

breach projecting a decline to the June low ($32 for EEM).

We are planning to substantially increase our exposure to non-gold

commodity stocks over the months ahead, but we already have enough

exposure to this group of stocks to be concerned about the effects on our

portfolio of concurrent commodity and equity sell-offs. We therefore

purchased some December-2016 EEM put options last week as both a hedge and

a speculation.

Those who are interested in a way of trading a

short-term stock market decline and who aren't interested in trading

options could consider buying the ProShares UltraShort Emerging Markets

ETF (EEV) near Friday's closing price of US$15.52. A decline in EEM to

around $32 would likely result in a gain of around 25% in EEV's price.

A daily close above $38.50 by EEM could be used as a stop for an

emerging-markets-related bearish speculation.

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date | Description |

| Monday October 17 |

Empire State Mfg Survey Industrial Production |

| Tuesday October 18 |

CPI TIC Report |

| Wednesday October 19 |

Housing Starts Fed's Beige Book |

| Thursday October 20 |

Existing Home Sales Leading Economic Indicators |

| Friday October 21 | No important events scheduled |

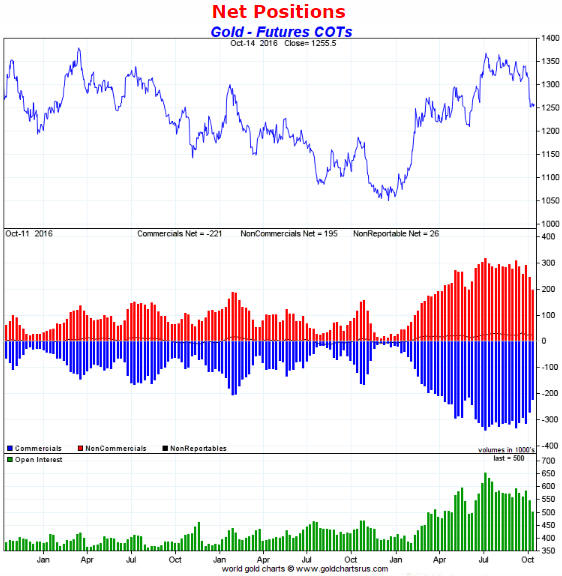

Gold and the Dollar