-- Weekly Market Update for the Week Commencing

18th April 2016

Big Picture

View

Here is a summary of our big picture

view of the markets. Note that our short-term views may differ from our

big picture view.

The BULL market in US Treasury Bonds

that began in the early 1980s ended in early-2015, but there will be many years

of topping action in bond prices and bottoming action in bond yields before

major new trends get underway. (Last update: 29 June 2015)

The stock market, as represented by the S&P500 Index,

commenced

a secular BEAR market during the first quarter of 2000, where "secular

bear market" is defined as a long-term downward trend in valuations

(P/E ratios, etc.) and gold-denominated prices. This secular trend will bottom sometime between 2018 and 2020.

(Last update: 29 June 2015)

A secular BEAR market in the

US

Dollar

began during the final quarter of 2000 and ended in July of 2008. This

secular bear market will be followed by a multi-year period of range

trading.

(Last

update: 09 February 2009)

Gold commenced a

secular bull market relative to all fiat currencies, the CRB Index,

bonds and most stock market indices during 1999-2001.

This secular trend will peak sometime between 2018 and 2020.

(Last update: 29 June 2015)

Commodities,

as represented by the CRB Index, commenced a

secular BULL market in 2001 in nominal dollar terms. The first major

upward leg in this bull market ended during the first half of 2008, but

a long-term peak won't occur until 2018-2020.

(Last

update: 29 June 2015)

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Outlook Summary

Market

|

Short-Term

(1-3 month)

|

Intermediate-Term

(6-18 month)

|

Long-Term

(2-5 Year)

|

|

Gold

|

N/A |

Bullish

(26-Mar-12) |

Bullish

|

|

US$ (Dollar Index)

|

N/A |

Bullish

(29-Feb-16) |

Neutral

(19-Sep-07) |

|

US Treasury Bonds (TLT)

|

N/A |

Bearish

(19-Oct-15)

|

Bearish |

|

Stock Market

(DJW)

|

N/A |

Bearish

(30-Dec-15) |

Bearish

|

|

Gold Stocks

(HUI)

|

N/A |

Bullish

(23-Jun-10) |

Bullish

|

|

Oil |

N/A |

Neutral

(26-Oct-15) |

Bullish

|

|

Industrial Metals

(GYX)

|

N/A |

Neutral

(09-Nov-15) |

Bullish

(28-Apr-14) |

Notes:

1. Our short-term expectations are discussed in the commentaries, but except in

special circumstances we won't attempt to assign a "bullish", "bearish" or

"neutral" label to these expectations.

2. The date shown below the current outlook is when the most recent outlook change occurred.

3. "Neutral" means that we think risk and reward are roughly in balance with respect to the timeframe in question.

4. Long-term views are determined almost completely by fundamentals and intermediate-term views

are determined by a combination of fundamentals, sentiment and technicals.

Last week's posts at the TSI Blog

ZeroHedge tries to create more drama out of nothing

The

true meaning of gold's COT data

Money

should NOT be backed by gold

The folly of staying bearish on oil due to "excess supply"

Monetary Inflation

Update

The most important monetary

indicator

The change in the rate of monetary inflation is one of the two inter-related

drivers of the boom-bust cycle, the other being the manipulation/distortion of

interest rates (the two are inter-related because interest rates can't be

suppressed without increasing the money supply and the creation or destruction

of money will naturally affect interest rates). That's why we closely track the

money-supply growth rates of several countries/regions.

The most important money supply is that of the US, but we've found that from a

practical investing/speculating standpoint the most useful money-supply

indicator is the combination of US$ and euro supply. We call this combination

"G2 TMS", where TMS stands for True Money Supply (a monetary aggregate based on

Austrian Economics principles). We created G2 TMS in response to what happened

during 2005-2006, when accelerating monetary inflation in the euro-zone delayed

the onset of an economic bust in the US.

As illustrated below, over the past 5 years the year-over-year (YOY) rate of

growth in G2 TMS oscillated between 6% and 10%. There was a surge to the top of

this range last year thanks to more rapid money-pumping in the euro-zone, but

over the past few months the inflation rate has fallen back to near the middle

of its 5-year range.

The booms that ended in 2000 and 2006-2007 did so a few months after the G2

monetary inflation rate dropped below 6%, which suggests that the current

investment booms are yet to run out of monetary steam. However, considering the

damage that has been done by the unprecedented central-bank interventions of the

past several years, it will not surprise us if the next bust starts with the G2

monetary inflation rate still comfortably above 6%. In fact, the next bust might

have already begun.

In summary, it's very likely that a decline in the G2 monetary inflation rate to

below 6% would soon be followed by economic busts and financial-market crises in

the US and Europe, but there's also an uncomfortably-high risk that this time

around these painful developments will begin at a faster inflation rate.

Japan's monetary inflation rate continues to defy widespread expectations and

beliefs

In early-2013 the Bank of Japan (BOJ) fired what many have likened to a monetary

bazooka when it implemented a QE program that was vastly bigger, relative to

GDP, than anything ever attempted in a developed country in the modern era.

Let's call it a QE on Steroids (QEOS) program. At the time this monetary bazooka

was fired, the YOY rate of growth in Japan's M2 money supply was slightly above

3%. Today it is still slightly above 3%. So much for the 'bazooka'.

As illustrated below, Japan's M2 inflation rate initially responded to the QEOS

program by rising to a high of almost 4.5% in early-2014. However, even at this

accelerated pace the money supply in Japan was growing at less than half the

pace of the money supply in the US at the time. Japan's current rate of monetary

inflation is less than half that of the US and less than one-third that of the

euro-zone. And yet, we still regularly see comments to the effect that the Yen

is being inflated to oblivion.

The fact is that the entire decline in the Yen from early 2013 through to

mid-2015 was based on a false perception. Perhaps that's why the Yen has been

'surprisingly' strong over the past few months.

Despite the obvious real-estate bubble, easy monetary policy persists in

Australia

Australia's monetary inflation rate has tapered over the past 12 months (see

chart below), but it is still in double digits. This hasn't prevented the A$

from strengthening on the FX market over the past three months, because the A$'s

rate of exchange against the US$ is primarily influenced by commodity prices and

the commodity markets have rallied. However, the on-going rapid monetary

inflation probably means that anyone in Australia whose salary isn't rising by

at least 8%/year will be experiencing a declining salary in real terms and that

houses are going to remain very expensive for a while.

Commodities

The wide-angle view

Over the past 10 years the CRB Index (the green line on the following chart) has

generally trended with international freight rates as measured by the Baltic Dry

Index (BDI, the blue line on the following chart). There have been multi-month

periods when these two quantities went their separate ways, but they always

ended up moving back into line with each other. For example, when a rally in the

CRB Index and a decline in the BDI during the first half of 2014 created a large

divergence, the divergence was subsequently closed by a plunge in the CRB Index.

For another example, a divergence created by a surge in the BDI and a decline in

the CRB Index during June-July of last year was subsequently eliminated by a

plunge in the BDI.

The CRB and the BDI have rallied together over the past 2 months, although the

BDI has recently been a lot stronger than the CRB.

The above chart's message is that it makes no sense to be bullish on commodities

and not bullish on international freight rates. If a major or at least an

intermediate-term bottom was put in place for broad-based commodity indices

during the first quarter of this year, as we currently suspect, then it's highly

probable that a major or at least an intermediate-term bottom is in place for

international freight rates.

The next chart compares the EEM/SPY ratio (emerging-market equities relative to

the US stock market) with the Goldman Sachs Spot Commodity Index (GNX). This

chart shows that on a long-term basis the GNX trends in the same direction as

the EEM/SPY ratio. More importantly, it shows that the EEM/SPY ratio tends to

lead the GNX at major turning points.

It's possible that a major turning point occurred early this year, but it hasn't

yet been confirmed. Confirmation would take the form of EEM/SPY achieving a

weekly close above its 70-week MA (the blue line on the chart).

Oil

In a

blog post late last week we discussed the folly of remaining bearish on oil

due to "excess supply". In a note at the end of this post we wrote: "The

price action hasn't yet definitively signaled a reversal, but it's possible that

an intermediate-term reversal signal will be generated at the end of this week."

An intermediate-term reversal signal was generated at the end of last week, in

that oil managed to achieve a weekly close above its 40-week MA (the red line on

the following chart) for the first time since mid-2014. Furthermore, the most

reliable measure of oil's supply-demand situation indicates a significant

tightening in this market over the past two months. We are referring to the fact

that there has been a meaningful shrinkage in the "contango" (the difference

between the price for future delivery and the cash price), which tells us that

oil supply is presently not as excessive as many people seem to believe.

At the same time, the following chart shows that the price reversed downward

last week after touching the top of a 2-year channel. This suggests to us that

there will be consolidation in the oil market over the next few weeks even if a

long-term upward reversal has happened.

A multi-year bottom is probably in place in the oil market, although there is

still a risk that the February low will be tested as part of a basing process.

The Copper Bottom

From the 15th February Weekly Update:

"At major price bottoms, gold leads and copper follows. With gold having

provided us with evidence that something more than a short-term rebound is in

the works, it's time to give more thought to the possibility that a sustained

up-turn in the copper market is not far away.

While gold tends to lead at major bottoms, the lead time is variable. For

example, in 2001 the bottom for gold preceded the bottom for copper by about 7

months, whereas in 2008 the bottom for gold preceded the bottom for copper by

1-2 months. However, if we are right to assume that gold has bottomed then the

next upside breakout in the copper price should signal the start of an

intermediate-term rally.

With reference to the following chart, a daily close above $2.15 would take the

copper price above lateral resistance and the top of a well-defined 9-month

channel. As long as the gold market maintains its longer-term bullish posture we

would therefore take a daily close above $2.15 as evidence of a sustainable

turnaround in the copper market."

The copper price subsequently signaled a sustainable turnaround by closing above

US$2.15. It then moved up to the low-$2.30s before embarking on a correction. We

don't know if the correction is over and we will not be surprised if the January

low is tested as part of a basing process, but due primarily to gold's

performance and leadership we suspect that a multi-year price bottom is in place

for copper.

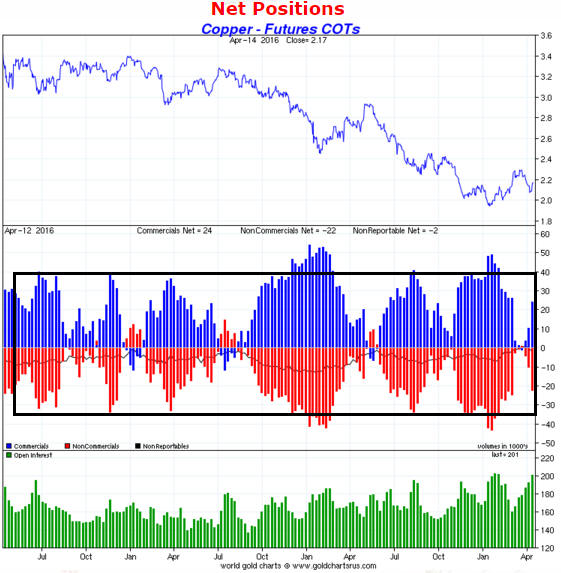

The Commitments of Traders (COT) report continues to perform admirably as an

indicator of short-term price tops and bottoms in the copper market. Just a

reminder that short-term price bottoms tend to occur at around the time that the

blue bars on the following chart (the Commercial net-position) reach the top of

the indicated range and/or the red bars on the following chart (the Speculative

net-position) reach the bottom of the indicated range, and that short-term price

tops occur at around the time that the speculative net-position reaches zero or

becomes slightly positive.

The COT data signaled the recent short-term price top and is currently

non-committal.

Chart source: www.sharelynx.com

A final point is that the COT levels that reliably indicated short-term price

tops and bottoms in copper over the past three years are going to stop working

when copper enters a new bull market. The reason is that after the major price

trend shifts from down to up the speculative net-position will be skewed more to

the long side than it has been over the past few years. The red bars on the

above chart moving well above zero during a short-term upward trend will

therefore be a sign that the long-term price trend has become bullish.

The Stock Market

The US

The senior US stock indices traded in a very narrow range over the final two

days of last week, that is, over the days since we posted last week's Interim

Update. On a daily closing basis the SPX was up one point on Thursday and down

two points on Friday. This means that the stock market is still 'pushing the

envelope' in terms of what's possible/plausible for a bear-market rebound.

Also unchanged over the final two days of last week are the bearish

divergences/non-confirmations we've recently noted. Specifically, the Dow

Transportation Average and the number of individual stocks making new highs are

still below their March peaks.

Here's the sequence of events that should soon begin IF our big-picture view is

correct:

1) A sharp 1-2 week pullback, most likely bottoming in the vicinity of the SPX's

50-day MA (1990-2000).

2) A rebound to a lower higher.

3) A much larger decline lasting several weeks.

By the way, step 1) in this sequence is a likely outcome even if our favoured

bear-market scenario is wrong. This is because a pullback to near the 50-day MA

is due (or overdue) regardless of the longer-term outlook. The difference is

that if a bull market is still in progress then a decline to the 50-day MA would

be followed by a move to a new high for the year.

With regard to valuation, the article posted

HERE makes some good points. For example, earnings for the S&P500 Index are

now about the same as they were in 2013 when the index was trading slightly

above 1600, which means that the SPX has gained about 30% over the past 2.5

years with no growth in earnings. This would not imply present over-valuation if

the market were dirt cheap back in 2013, but back then the P/E ratio was already

about 13% above the long-term average. Today the SPX's P/E ratio is 24, putting

it in the top 8% of the long-term range.

On its own, a high valuation is generally not a good reason to enter a bearish

speculation. This is because historically-expensive markets often get more

expensive, and sometimes get a lot more expensive, before they top. However, we

currently have over-valuation combined with evidence that the long-term price

trend has reversed downward. To put it another way, there is evidence that

valuations are going to become lower over the months ahead.

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date |

Description |

| Monday

Apr 18 |

Housing Market Index |

| Tuesday

Apr 19 |

Housing Starts |

| Wednesday

Apr 20 |

Existing Home Sales |

| Thursday

Apr 21 |

Philadelphia Fed Business

Outlook Survey

Leading Economic Indicators |

| Friday Apr 22 |

No important events

scheduled |

Gold and the Dollar

Gold

The Yuan Gold Fix

As of April 19 the

Shanghai Gold Exchange (SGE) will quote a "gold fix" twice per day.

Like the famous twice-daily London Gold Fix, the SGE gold fix will simply be a

snapshot of the spot price at a set time. In other words, the 'fix' is not

actually determined by the banks that participate in the 'fixing' process, it is

determined by the market. There is some ability for the participants in the

'fix' to shift the price in one direction or the other for their own purposes

(for example, to avoid paying-out on option contracts), but the effect on the

overall market of such machinations would be very small in terms of both time

and price.

As far as we can tell, the Yuan gold fix will have no effect on gold's true

fundamentals and will therefore have no effect on gold's intermediate-term or

long-term price trends. It shouldn't even have an effect on gold's short-term

price performance, although whether it does or not will largely depend on the

vagaries of speculative sentiment.

Current Market Situation

The US$ gold price achieved a marginal upside breakout near the end of the week

before last. It built on this breakout last Monday, but then turned around and

headed back to its 50-day MA. At the end of last week it was in the narrow gap

between its 50-day and 20-day MAs -- slightly above the former and slightly

below the latter.

The reason we rarely buy in reaction to an upside breakout is that more than

half the time they either prove to be false signals or are quickly followed by

pullbacks to test the breakout. We don't yet know whether gold's recent upside

breakout was a genuine signal of what's to come or a false signal 'designed' to

suck-in some additional speculators on the long side prior to a move to new

2-month lows. These conflicting near-term outcomes are equally plausible.

With regard to gold's likely performance over the weeks ahead, the waters are

muddied by the fact that speculative sentiment has become increasingly bullish

over the past 2 months while the price has worked off an 'overbought' extreme by

essentially going sideways. We are referring to the fact that last Friday's

closing level for the US$ gold price was $12 lower than its closing level on

11th February, and yet the total speculative net-long position in Comex gold

futures is now substantially greater than its February-2016 peak and at its

highest level since late-2012 (when gold was trading at around $1700/oz). To put

it another way, in momentum terms the gold market appears to have completed a

correction while at the same time becoming even more stretched to the upside in

speculative sentiment terms.

That there has, indeed, been rising speculative enthusiasm for gold in the face

of lacklustre short-term price action is also evidenced by the performance of

the gold-mining sector. Since 11th February there has been a 21% increase in GDX

and a 35% increase in the more speculative GDXJ in parallel with a 1% DECLINE in

the US$ gold price.

One possibility is that there will be a further surge in the level of

speculation over the next 2-3 weeks, propelling gold to the low-$1300s and

creating a blow-off move to the upside in the gold-mining sector. This is why

it's important to maintain a sizable core position in gold stocks. Another

possibility is that there will soon be a solid break below the 50-day MA in the

gold market, prompting the quick-fire liquidation of recently-taken speculative

positions in both gold and the mining stocks. This is why it's important NOT to

have leveraged positions predicated on a bullish near-term outcome.

Gold Stocks

With regard to both the price action and the fundamental backdrop, the

gold-mining rally that has the most in common with this year's rally is the one

that began in late-November of 2000. This was the rally that kicked off a

cyclical and a secular bull market.

The following weekly chart covering the 2000-2002 period shows that the first

intermediate-term correction didn't begin until after the HUI reached its

200-week MA (the red line) in early-May of 2001. The chart also shows that there

was a significant 3-4 week short-term correction in March-2001 -- near the

mid-point of the first upward leg.

The next weekly chart shows the current situation.

The main difference up until now between the rally that got underway in

late-2000 and the rally that got underway in January of this year is that this

year's rally has not yet experienced a genuine short-term correction. In fact,

since the beginning of this year's rally there have only been two down-weeks for

the HUI and these down weeks were separated by four up-weeks.

If this year's rally ends up matching the 2000-2001 rally then the HUI will

reach an intermediate-term peak of around 250 in late-June or early-July.

However, in order for the rally to continue for another 2-3 months there will

soon have to be a significant multi-week correction (the HUI can't keep going up

in a straight line). An alternative is that we get an upside blow-off that takes

the HUI to an intermediate-term peak within the next 2-3 weeks. Such a blow-off

would likely be followed by a large 1-2 month decline.

Zooming-in on the recent price action, the HUI broke out to the upside during

the week before last and built on its breakout during the first two days of last

week before suffering a minor set-back. At the risk of sounding repetitive

(we've said something similar almost every week for the past 2 months), the HUI

remains stretched to the upside but hasn't yet signaled a short-term top.

At a minimum, a correction within an on-going short-term upward trend would take

the HUI down to the 165-170 range. A short-term correction to lateral support at

140 is still possible, but as a result of the price action of the past two weeks

is now much less likely.

Before leaving the gold-mining sector it is worth mentioning that there has

recently been evidence of speculators moving down the gold-stock food chain in

search of profits. What we mean is that some lower-quality/higher-risk gold

stocks have recently risen sharply on much-higher-than-average trading volumes.

Two examples are Golden Star Resources (GSS) and Timmins Gold (TGD), but there

are many others.

Speculators are undoubtedly now being attracted to lower-quality/higher-risk

gold stocks on the basis that these stocks offer huge leverage to additional

gains in the gold price. But while this line of thinking can be correct, it

doesn't always apply.

For example, a gold deposit that currently requires a gold price of at least

$1800/oz to become economic offers precisely zero leverage to an increase in the

gold price, because the gold will never be extracted from the ground. That's not

because the gold price won't eventually move above $1800/oz, but because by the

time the gold price moves above $1800/oz the cost of extracting the gold will

have risen and there will be many other deposits with better economics standing

in line for development.

Also, whether or not a gold producer with relatively high costs actually does

offer operational leverage to gains in the gold price will depend on what

financial commitments the producer has entered into. For example, due to the

"streaming" and debt deals done by GSS to ensure its survival, GSS offers

surprisingly little operational leverage to the gold price. In effect, GSS now

exists primarily for the benefit of Royal Gold, its "streaming" partner and

major creditor.

The Currency Market

In last week's Interim Update, we wrote: "The Dollar Index is showing signs

of reversing upward. It will generate a clear-cut bullish signal in the form of

an outside week to the upside if it is able to trade above 95.1 within the next

two trading days and retain the bulk of Wednesday's gain."

The Dollar Index did trade above 95.1 and achieved an outside week to the

upside. The bullish signal was weakened by Friday's pullback, but we would still

view it as an early warning of a short-term trend reversal. A weekly close above

96 would be a more conclusive warning.

The Yen has been a relatively strong currency since the global stock-market peak

in mid-2015, which isn't surprising to us. What is surprising is the Yen's

upward acceleration over the past two months in parallel with the stock market's

rebound.

Based on the performance of Yen futures during previous rallies from multi-year

bottoms (the shaded areas on the following weekly chart), the 200-week MA (the

red line on the chart) is the most realistic target for an intermediate-term

peak. This implies a 2016 upside target for Yen futures of around 97.

Updates

on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Company

news/developments for the week ending Friday 15th April 2016:

Company

news/developments for the week ending Friday 15th April 2016:

[Note: AISC = All-In Sustaining Cost, FS = Feasibility Study, FY = Financial

Year, IRR = Internal Rate of Return, MD&A = Management Discussion and Analysis,

M&I = Measured and Indicated, NAV = Net Asset Value, NPV(X%) = Net Present Value

using a discount rate of X%, P&P = Proven and Probable, PEA = Preliminary

Economic Assessment, PFS = Pre-Feasibility Study]

*Dalradian Resources (DNA.TO) reported the final results from the

51,000m infill drilling program at its Curraghinalt project in Northern Ireland.

The drilling program was designed to convert a substantial portion of the

Inferred resources to M&I resources as part of the on-going FS.

It looks like the drilling program achieved its intended purpose, but we'll soon

know for sure because a resource update incorporating the 51,000m of infill

drilling is nearing completion. This resource update will be an important

milestone for DNA.

We have C$2.00 in mind as an intermediate-term target for DNA. This target is

based on our valuation of the Curraghinalt project, which is, in turn, based on

the project's PEA and our view that the FS (due late this year) will confirm the

positive economics indicated by the PEA. However, the stock is not currently a

good candidate for new buying. This is due to last week's >20% surge to the

vicinity of an important resistance level (see chart below).

Even though DNA slightly underperformed over the past two months and continues

to offer good value, for anyone with a significant position in this stock the

recent rapid rise to the vicinity of important resistance has created an

opportunity for PARTIAL profit-taking.

*Energold Drilling (EGD.V) published its financial results for the

year ending 31st December 2015.

Revenue for the year was C$82M, which was C$19M lower than the previous year

thanks to the industry-wide reductions in drilling for metals, oil and gas.

However, the company did a good job of protecting its balance sheet considering

the very difficult market environment for its services. Specifically, the

company began 2015 with a healthy $64M of adjusted working capital (current

assets minus current liabilities and long-term debt) and ended the year with a

still-healthy $59M of adjusted working capital.

With about C$1.23/share of adjusted working capital and an $80M/year drilling

business, EGD continues to offer good value at its current share price of

C$1.12. Note, though, that its business probably won't begin to improve until at

least 6 months after a sustained turn to the upside in commodity prices.

Assuming that commodity prices bottomed during the first quarter of 2016, this

means that its business probably won't begin to improve until at least Q3-2016.

However, the stock price moved up sharply from a January bottom due to the

stock's extremely low valuation (it traded in the low-C$0.30s during December

and January) and a change in market sentiment.

We mentioned last November that the one company-specific concern we have about

EGD is that the "Current Assets" category of its balance sheet includes C$54M

under "Inventories". This is unchanged over the past 12 months and is a concern

because it is an unknown -- we don't know the composition of the "inventories"

amount and whether or not this amount is an accurate reflection of present

market value.

*Endeavour Mining (EDV.TO) announced that it has commenced mine

construction at the Hounde gold project in Burkina Faso. The Hounde Project is

expected to deliver average production of 190K-oz per year over a 10-year mine

life at an AISC of US$709/oz, and the initial capital cost is estimated at

US$328M. Production is scheduled to begin late next year.

The initial capex will be funded by EDV's existing cash and the cash it expects

to generate over the coming 18 months. To ensure that its existing mines

generate sufficient cash to fully fund the construction of the Hounde mine, the

company has established a hedging program covering 50% (400K ounces) of its

production during the 15-month period from April-2016 through to June-2017. The

hedging program guarantees a minimum gold price of US$1200/oz and a maximum gold

price of US$1400/oz for EDV's production during this period.

With the recent acquisition of True Gold Mining (TGM) and the decision to move

the Hounde project into production, EDV can now be likened to a West Africa

gold-mining ETF. When Hounde goes into production the company will have two

operating gold mines in Burkina Faso (Karma and Hounde), two operating gold

mines in Ivory Coast (Agbaou and Ity), an operating gold mine in Mali (Tabakoto)

and an operating gold mine in Ghana (Nzema).

We roughly estimate EDV's value to be C$15/share at a gold price of US$1200/oz

and C$20/share at a gold price of US$1300/oz. It's time we did an updated,

detailed valuation for this stock, but we are holding off because the company is

so active at the moment that any estimate would quickly become obsolete.

*Pilot Gold (PLG.TO) reported the results of the first 8 holes of

this year's drilling program at its Goldstrike project in Utah. This project was

previously mined on a small scale during the 1980s and 1990s via 12 shallow

pits. PLG believes that there could be a lot more gold in the vicinity.

There were significant oxide-gold intercepts in seven of the aforementioned

holes, including 2.10 grams/tonne gold (g/t Au) over 35.1 metres and 1.19 g/t Au

over 57.9 metres.

PLG's drilling program is open-ended, with results from earlier holes

determining the quantity and locations of subsequent holes. The aim is to obtain

enough data to come up with an initial resource estimate by year-end.

*Petrus Resources (PRQ.TO), a junior natural-gas producer, is

worthy of comment due to the relentless decline in its stock price. In January

the company completed a financing at C$7.40/share and also completed a takeover

of Phoscan (FOS) based on an implied C$7.40/share price for the yet-to-be-listed

PRQ shares. The shares were listed on the TSX in February and commenced trading

at C$5.00.

We became interested and brought the stock to the attention of TSI readers after

it had dropped to the C$2.90s, where it appeared to offer good value. The stock

price has since fallen all the way to the C$1.80s.

We have no new information. As mentioned in a previous commentary, we suspect

that the relentless downward pressure on the stock price is the result of

selling by the former shareholders of FOS who ended up with PRQ shares as part

of the takeover that was completed in January. These shares are being sold into

a market that has remained illiquid up until now, which would explain why the

selling is having such a big effect on the stock price. However, there is a risk

that the price weakness is the result of company-specific problems that we are

unaware of.

Due to the fact that we added PRQ to the TSI List as a long-term play based on

valuation it would be illogical for us to remove it after there has been no

known fundamental change and an improvement in the valuation.

In our own accounts the exposure to PRQ is about half of what we would consider

to be a full position. Our plan is to build up to a full position over the next

few months, but whether we actually do so will depend on the company-specific

facts we gather and the performance of the natural-gas market in the meantime.

*Ramelius Resources (RMS.AX) reported that its gold production for

the March quarter was at the low end of its 26K-29K guidance range and that the

average AISC for the quarter was higher than the A$1150/oz guidance. Also, the

company consumed about A$2M of cash during the quarter due to about $8M of

capital spending.

This is not a great result, but it's still OK. With capital spending on the new

Vivien gold mine now essentially complete and low-cost production from the

Vivien mine set to increase, RMS is likely to be cash-flow positive and

profitable during the current quarter.

*Timmins Gold (TGD) reported a good production result for the

first quarter of 2016. The company produced 25.1K ounces of gold, which was

slightly ahead of plan and a bit more than we were counting on. What we don't

know -- because the information isn't yet available -- is whether the good

production result enabled the company to add some much-needed cash to its

balance sheet. As previously advised, TGD needs to obtain additional cash -- to

fill a balance-sheet hole -- by mid-year. If it can do so without massively

diluting the stock it will have the potential to retrace the bulk of the past 2

years' price decline.

*UEX Corp. (UEX.TO) reported the initial results from its drilling

program at the Christie Lake uranium project. UEX currently owns 10% of the

project and has an option to increase its ownership to 70%. The project has an

historic (meaning: not NI 43-101 compliant) resource of 21M pounds grading 3.2%

U3O8.

The results have been received for three holes, two of which failed to hit the

targeted mineralisation and one of which contained a very significant

intersection grading 13.24% U3O8 over 3.1m. This is a good start.

Candidates

for new buying

In the market update posted on 9th April we wrote:

"...if you have a relatively small position in the gold-mining sector and

feel the need to increase your exposure to this sector in response to last

week's upside breakouts in the gold-mining indices, the following stocks are

worth considering near their current prices:

DNA.TO, EVN.AX, PG.TO, RSG.AX, SBB.TO"

It's getting increasingly difficult to find anything in the gold-mining sector

that isn't very stretched to the upside on a short-term basis and could

therefore be considered for new buying in the immediate future. For example, a

week ago the stocks mentioned above had been consolidating for a few weeks and

in addition to offering good value were not short-term 'overbought', but during

the past week DNA.TO and RSG.AX gained more than 20%. Although they are both

likely to trade much higher within the coming 12 months, these two stocks can

now be eliminated as immediate candidates for new buying. EVN.AX, PG.TO and

SBB.TO 'only' gained about 5% last week and could still be considered for new

buying by investors who feel the need to increase their exposure to the gold

sector.

Outside the gold-mining sector there is some value to be found. In particular,

there are uranium and O&G stocks/ETFs that offer good value and are not

short-term 'overbought'. However, concern about the risk of a general

stock-market decline prevents us from highlighting these stocks.

On a short-term basis the trade with the best risk/reward is some form of

bearish speculation on the broad US stock market. Examples include inverse index

funds, put options on ETFs such as QQQ and SPY, and call options on inverse

funds such as QID. This is partly because the general market's short-term risk

is high and partly because it wouldn't take much additional strength from here

to prove us wrong (our bear-market scenario is close to a make-or-break

position, which makes risk management straightforward).

Last Friday we added to our QID call-option position (a bearish speculation

linked to the NASDAQ100 Index). The position size is still small, but it would

yield a large profit if the NASDAQ100 were to return to its 2016 low within the

next 2.5 months.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html