![]()

![]()

![]()

![]()

-- Weekly Market Update for the Week Commencing 19th March 2018

Big Picture

View

Here is a summary of our big picture

view of the markets. Note that our short-term views may differ from our

big picture view.

The BULL market in US Treasury Bonds that began in the early 1980s ended in mid-2016, but there will be many years of topping action in bond prices and bottoming action in bond yields before major new trends get underway. A major decline in government bond prices will unfold during the 2020s. (Last update: 11 September 2017)

The stock market, as represented by the S&P500 Index, commenced a secular BEAR market during the first quarter of 2000, where "secular bear market" is defined as a long-term downward trend in valuations (P/E ratios, etc.), gold-denominated prices and inflation-adjusted prices. This secular trend will bottom in 2020 or later. (Last update: 11 September 2017)

A cyclical BEAR market in the US Dollar began in 2016-2017. (Last update: 11 September 2017)

Gold commenced a secular bull market relative to all fiat currencies, the CRB Index, bonds and most stock market indices during 1999-2001. This secular trend will peak in 2020 or later. (Last update: 11 September 2017)

Commodities,

as represented by the CRB Index, commenced a

secular BULL market in 2001 in nominal dollar terms. The first major

upward leg in this bull market ended during the first half of 2008, but

a long-term peak won't occur until 2020 or later.

(Last

update: 11 September 2017)

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

True

Fundamentals Summary

[Notes:

1) The date shown next to the current True Fundamentals Model (TFM) signal is

when the most recent change occurred. 2) Charts of the Gold and Equity

TFMs are included in the "Charts and Indicators" section of the TSI web

site]

| Market | True Fundamentals Model (TFM) |

| Gold (US$ Price) | Bearish (12 Jan 2018) |

| US Equity (SPX) | Neutral (12 Jan 2018) |

| Currency (Dollar Index) | Bullish (15 Dec 2017) |

| Commodities (GNX) | Bullish (29 Dec 2017) |

Last week's posts at the TSI Blog

There were no blog posts last week.

Summary of current

thinking/positioning

1) A number of markets are set

up for trend reversals or accelerations, with the US$ being the linchpin.

If the DX breaks out to the downside from its recent narrow range then

rallies should begin or accelerate across the commodity world, with silver

bullion and gold-mining stocks leading the way higher. However, if the DX

breaks out to the upside from its recent range then the commodity world

will have a downward bias for the ensuing two months.

2) More

evidence has emerged that the US stock market's decline from its January

peak was nothing more than a short-term correction, although there is

still a chance that some stock indices will revisit their early-February

lows.

3) Downward corrections in oil and copper will end by May,

with the timing dependent upon what happens in the currency market. We've

had March in mind for a correction low, but the turning point will be

delayed if the DX breaks out to the upside.

4) Bond yields are in

long-term upward trends and will go much higher before year-end, but a

counter-trend move is underway. The counter-trend move could end at any

time, although we won't be interested in placing a new bet against the

bond market (a new bet on higher interest rates) until there is a

substantial reduction in the speculative net-short position in 10-year

T-Note futures.

5) Holding a cash reserve of 25%-30%.

Interest Rates

The Fed is set to hike

two more times before mid-year

Unless nuclear war breaks

out in the next two days, the Fed will announce another 0.25% increase in

its targeted interest rates on Wednesday 21st March. This will bring the

target range to 1.50%-1.75%. Also, there's a high probability of another

0.25% hike at the June FOMC meeting (13th June).

Two 0.25% Fed rate

hikes before mid-year will not have a big effect on the financial markets

because the scenario has been almost fully discounted. As evidence we cite

the following chart of the 3-month T-Bill yield (UST3M).

The

pattern over the past two years has been for UST3M to move slightly above

the bottom of the expected new target range a few weeks prior a Fed rate

hike. For example, last November the Fed Funds Rate (FFR) target range was

1.00%-1.25% and there was a general expectation that the target would be

boosted to 1.25%-1.50% in December. To reflect this expectation, UST3M

rose to 1.30% in the second half of November.

A repeat of the

pattern would now see UST3M at about 1.55% (near the bottom of the range

that will come into being on 21st March), but the market is already

pricing the 3-month bill to yield 1.78%. This means that it is pricing in

a near certainty of an increase to 1.75%-2.00% within three months.

A lot will have to go wrong in the stock market and/or the economy

over the next 2-3 months to prevent the Fed from implementing its second

2018 rate hike in June. It's therefore a good bet that the first half of

2018 will contain two rate hikes. However, that might be 'all she wrote',

because it's quite possible that stock market and/or economic weakness

will become serious enough by July-August to put the Fed on hold.

The T-Bond rebound gathers some steam

The 30-year

T-Bond broke out to the downside from a major top formation in

late-January. This breakout provided powerful confirmation of our bearish

outlook for long-term bond prices and bullish outlook for nominal interest

rates.

The T-Bond's breakout suggests that there is scope for

considerable additional downside in the price over the coming two

quarters, but by the third week of February the Treasury market had become

sufficiently 'oversold' to enable a counter-trend rebound to get underway.

The base of the major top formation (146.5-147.0) is an obvious target for

this rebound.

The following chart compares the T-Bond price with

the S&P500 Index (SPX). It isn't a random coincidence that the downside

breakout by the T-Bond was almost immediately followed by a sharp decline

in the stock market (as represented here by the SPX). As we've said

numerous times in the past, the stock market can ignore a rising

interest-rate trend for a long time, but if the trend persists then it

eventually becomes almost the only thing that matters.

It seems that the stock market has become accustomed to a 10-year

yield in the 2.80%-3.00% range. This means that the breakouts to new

multi-year highs in the 10-year yield (see chart below) and new multi-year

lows in the T-Bond price (as discussed above) provoked only a short-term

stock market correction, albeit a sizable one. They didn't bring about a

major stock market decline. For that, the 10-year yield probably will have

to break solidly above 3%.

A new TBT trade opportunity may soon emerge

The ProShares UltraShort 20+ Year Treasury Fund (TBT) trends in the

opposite direction to the T-Bond. We exited a TBT long position at a

profit about a month ago with the aim of re-establishing a position

following a rebound in the T-Bond price. The T-Bond rebound is well

underway and, as a result, soon there may be a good opportunity to buy

TBT.

We hope to be able to re-enter TBT at around $36 in

preparation for another multi-month decline in the bond market, but we'll

take our cues from the COT data and the price action in the Treasury

market. With regard to the former, we'd like for there to be a substantial

shrinkage in the speculative net-short position in 10-year T-Note futures

before we place a new bet against the bond market.

The Stock Market

Current Market Situation

The NASDAQ100 Index (NDX) managed to close lower on each of the past

four days without negating the previous week's upside breakout. Therefore,

the probability that we are dealing with a genuine breakout has increased,

although we still can't rule out the possibility that some stock indices

will test their early-February spike lows before the overall correction

ends.

The Dow Transportation Average (TRAN) is one stock index that is very

much at risk of testing its early-February spike low. This risk will be

greatly reduced by a daily close above 10,800.

We assess the stock market's true fundamentals to be neutral at this

time.

After being at an optimistic extreme during January and being

momentarily fearful when the short-volatility trade was blowing up in

early-February, sentiment also appears to be neutral at this time. On the

minus side there is very little negativity or fear evident in the

sentiment indicators, but on the plus side the speculative 'froth' that

was blatantly obvious two months ago has been removed.

The bottom

line is that the stock market is not yet totally 'out of the woods', but

there's a high probability that the Q1 decline was nothing more than a

short-term correction.

Tesla (TSLA), the world's greatest

story stock

TSLA is a classic story stock, in that it has

a market valuation that could only be justified by creating a story

involving wildly ambitious assumptions about the future. In TSLA's case,

however, the wildly ambitious assumptions seem totally implausible rather

than just unlikely.

Why investors are buying/holding this stock

near its current valuation is therefore something of a mystery to us. In

particular, we can't understand how anyone with any business sense could

expect a car manufacturer that did nothing except hemorrhage cash during a

period when it was benefiting from government assistance and first-mover

advantage to consistently generate large profits after the government

assistance is mostly taken away and the company finds itself in direct

competition with the likes of Mercedes, Porsche, BMW, Audi and Jaguar.

That being said, timing is everything. It seems inevitable that the

price of a Tesla share will drop to a small fraction of its current level,

but we aren't confident that it will happen this year. Also, Tesla CEO

Elon Musk is one of the all-time great promoters -- a modern day PT

Barnum. He seems to be able to whip-up enthusiasm for the stock at will.

With regard to timing, over the past 9 months the TSLA price has

traced out a pattern that has the look of a major top, and within the

larger pattern it has, over the past 3 months, traced out what looks like

a double top. This could mean that we are not far away from the point

where selling pressure finally begins to overwhelm the buying of Musk's

blind followers.

Critical support and resistance lie at $310 and

$360, respectively. A solid close below $310 would warn that a substantial

decline was about to begin whereas a close above $360 would warn that

everything since the June-2017 peak was an intermediate-term consolidation

within an on-going bull market.

The TSI List currently has a bearish TSLA speculation in the form of

the April-2018 $250 put option. There is now only about a month before

this option expires, so unless the downside breakout that we are

anticipating happens in the next week or so we will have to either exit at

a loss or

roll into a later-dated option. Most likely the former, unless we have

a good reason to believe that a large decline has begun.

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date | Description |

| Monday Mar-19 | No important events scheduled |

| Tuesday Mar-20 | No important events scheduled |

| Wednesday Mar-21 |

Q4-2017 Current Account Balance Existing Home Sales FOMC Policy Statement and Forecasts |

| Thursday Mar-22 | No important events scheduled |

| Friday Mar-23 |

Durable Goods Orders New Home Sales |

Gold and the Dollar

There is still a realistic chance that the gold sector (as represented

by the HUI) will make a multi-month low this month, but only if there is a

sharp decline over the coming 1-2 weeks. The most likely alternative would

be a continuing downward drift to an intermediate-term bottom in May.

The Currency Market

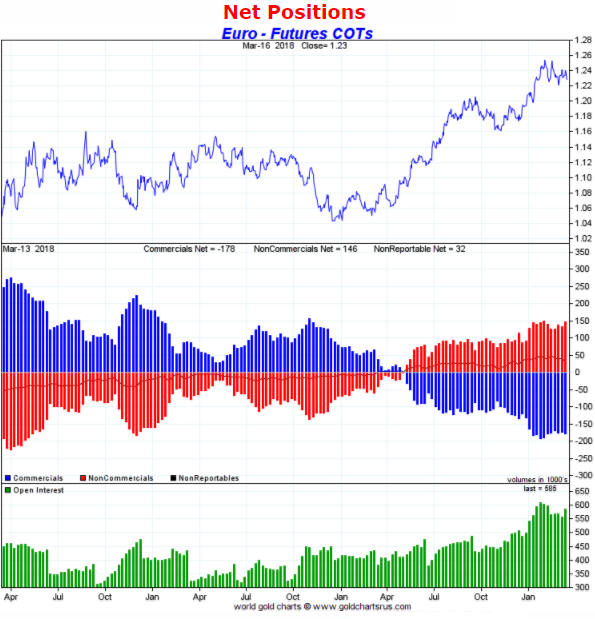

The Euro

The 2-month trading

range in the DX evident on the chart included in the Gold section above is

associated with and similar to the 2-month trading range in the euro

evident on the daily chart displayed below. The difference is that for the

DX it's a potential base and for the euro it's a potential top.

If

the euro breaks below the bottom of its range in the near future then up

to 2 months of additional downside may be in store. The targets would be

1.19 and 1.16 (we think that lateral support at 1.16 defines the euro's

maximum short-term downside risk).

That being said, there's no

guarantee that we are dealing with a topping pattern in the euro. It could

be a mid-trend consolidation, in which case there will soon be a break

above the top of the range followed by up to 2 months of additional

upside.

We put the odds at 60/40 in favour of a near-term downside

breakout in the euro.

The main reason to favour a downside breakout is that speculative euro

sentiment remains stretched into optimistic territory at a time when

interest-rate and equity-performance differentials constitute a

substantial headwind. The stretched speculative sentiment is indicated by

the following chart of the euro's COT situation. This chart shows that the

range-trading of the past 2 months has done nothing to reduce the

enthusiasm of speculators in euro futures.

The A$

When we posted our 21st February

commentary the A$ was trading at 78, which we had previously cited as a

likely level for a correction low. However, we wrote that taking into

account the overall market situation there could be up to 2 additional

points of downside before the next tradable rally got underway. Our

preference was to wait for a better opportunity before buying.

We

speculated that a better opportunity to buy the A$ would arrive in March,

as this was a likely time for the Dollar Index to reach a short-term top

and for some high-profile commodity markets to reach short-term bottoms.

The A$ is now one point lower, having rebounded to around 79 before

dropping to 77. As illustrated by the following daily chart, the rebound

ended at the 50-day MA.

A decline to 76 appears to be on the cards,

but a lot will depend on whether the DX breaks out to the upside or the

downside from its 2-month range. Even though the A$ is not part of the DX,

if the DX breaks out to the upside and accelerates in that direction then

many high-profile commodities and all the major currencies will come under

pressure.

Updates

on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() Company

news/developments for the week ending Friday 16th March 2018:

Company

news/developments for the week ending Friday 16th March 2018:

[Note: AISC = All-In Sustaining Cost, FS = Feasibility Study, FY =

Financial Year, IRR = Internal Rate of Return, ISR = In-Situ Recovery,

MD&A = Management Discussion and Analysis, M&I = Measured and Indicated,

NAV = Net Asset Value, NPV(X%) = Net Present Value using a discount rate

of X%, NSR = Net Smelter Return, P&P = Proven and Probable, PEA =

Preliminary Economic Assessment, PFS = Pre-Feasibility Study]

*Alio Gold (ALO) reported the result of the first deep

hole from its 6-hole surface drilling program at the Ana Paula project in

Guerrero State, Mexico. The purpose of the hole was to get more

information about the high-grade breccia mineralisation below the proposed

open pit and to test a potential source of lower-grade mineralisation that

is much closer to the surface but outside the proposed pit. The hole was

successful on both counts, intersecting 6.45 g/t gold over 19.0m in the

deep, high-grade breccia and 1.3 g/t gold over 55.7m in the

close-to-the-surface lower-grade area.

Two more holes in the 6-hole

program are complete and awaiting assays.

*U.S. Gold

Corp. (USAU) has completed comprehensive geochemical sample

surveys covering the 20-square-mile Keystone district project area. The

sample database now comprises 4,225 soil samples, 2,250 rock samples, 649

fine-sediment stream samples, and 620 altered stream cobble samples. This

is all part of the process of zooming in on target areas for drilling.

*Solitario Zinc (XPL) published its financial

statements for the quarter and year ending 31st December 2017. The

statements revealed that the company had no long-term debt and US$14.5M of

working capital (down about US$0.5M over the final 3 months of the year).

XPL is well positioned with stakes in two attractive exploration-stage

zinc projects. It is also very under-valued at its current price of

US$0.50.

As mentioned in our 19th February report, we are concerned

that it will remain very under-valued for another 6-12 months due to a

lack of market-moving news.

![]() List

of candidates for new buying

List

of candidates for new buying

From within the ranks of TSI

stock selections the best candidates for new buying at this time, listed

in alphabetical order, are:

1) ALK.AX (last Friday's closing price:

A$0.31)

2) ALO (last Friday's closing price: US$2.42)

3)

AOI.TO (last Friday's closing price: C$1.27)

4) PG.TO (last

Friday's closing price: C$3.01)

The above list is limited to five

stocks. It will sometimes contain less than five, but it will never

contain more than five regardless of how many stocks are attractively

priced for new buying.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://www.goldchartsrus.com/