![]()

![]()

![]()

![]()

-- Weekly Market Update for the Week Commencing 19th August 2019

Big Picture

View

Here is a summary of our big picture

view of the markets. Note that our short-term views may differ from our

big picture view.

The BULL market in US Treasury Bonds that began in the early 1980s ended in mid-2016, but there will be many years of topping action in bond prices and bottoming action in bond yields before major new trends get underway. A major decline in government bond prices will unfold during the 2020s. (Last update: 11 September 2017)

The stock market, as represented by the S&P500 Index, commenced a secular BEAR market during the first quarter of 2000, where "secular bear market" is defined as a long-term downward trend in valuations (P/E ratios, etc.), gold-denominated prices and inflation-adjusted prices. This secular trend will bottom in 2020 or later. (Last update: 11 September 2017)

A cyclical BEAR market in the US Dollar began in 2016-2017. (Last update: 11 September 2017)

Gold commenced a secular bull market relative to all fiat currencies, the CRB Index, bonds and most stock market indices during 1999-2001. This secular trend will peak in 2020 or later. (Last update: 11 September 2017)

Commodities,

as represented by the CRB Index, commenced a

secular BULL market in 2001 in nominal dollar terms. The first major

upward leg in this bull market ended during the first half of 2008, but

a long-term peak won't occur until 2020 or later.

(Last

update: 11 September 2017)

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

True

Fundamentals Summary

[Notes:

1) The date shown next to the current True Fundamentals Model (TFM) signal is

when the most recent change occurred. 2) Charts of the Gold and Equity

TFMs are included in the "Charts and Indicators" section of the TSI web

site]

| Market | True Fundamentals Model (TFM) |

| Gold (US$ Price) | Bullish (04 Jan 2019) |

| US Equity (SPX) | Bearish (19 Apr 2019) |

| Currency (Dollar Index) | Neutral (15 Mar 2019) |

| Commodities (GNX) | Bearish (01 Jun 2018) |

Last week's posts at the TSI Blog

There were no blog posts last week.

Summary of current

thinking/positioning

1) The performance of the Dollar

Index (DX) could be 'choppy' for 1-3 more months, but the most likely

direction of the next tradable move is down.

2) The US$ gold price

has broken out to the upside on a monthly basis and has confirmed a bull

market (implying the likelihood of significant additional gains over the

coming 1-2 years). However, the short-term risk/reward is no longer

favourable. We expect that a short-term top will be in place by

early-September.

3) As is the case with gold bullion, the

gold-mining sector's short-term risk/reward is no longer favourable.

However, substantial additional gains probably will be made within the

next 6 months.

4) The SPX has signaled a short-term top and

probably has commenced a sizable 1-2 month decline.

5) The start of

a multi-quarter T-Bond decline has been delayed by recent market action.

We guess that a downward trend will get underway during September-October,

but first a short-term top must be signaled. There is a risk that

near-term stock market weakness will lead to additional upside in the

T-Bond.

6) We are holding a cash reserve of about 25%.

Commodities

Expecting a platinum

breakout

First gold broke out to the upside (from a

long-term consolidation) and then silver broke out to the upside (from a

long-term downward trend). Next it should be platinum's turn.

For

platinum, a weekly close above $920 would be a major upside breakout as it

would take out the April-2019 intermediate-term top and the

downward-sloping trend-line dating back to the 2016 top.

Platinum is absurdly cheap relative to palladium, very cheap relative

to gold and moderately cheap relative to silver. This suggests the

potential for a big catch-up move.

As is the case for silver, for

platinum we have the 2016 top in mind as a minimum intermediate-term

upside target. Our maximum upside target is the gold price, that is, our

maximum target for the platinum price is whatever it needs to be to

achieve a platinum/gold ratio of 1. As we first mentioned a few years ago,

we think that 1 has gone from being a long-term floor to being a long-term

ceiling for the platinum/gold ratio.

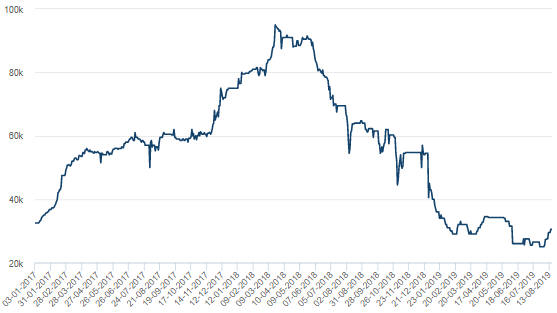

Cobalt makes another

attempt to bottom

The following chart shows that since the

beginning of this month the per-tonne cobalt price has risen from $25,000

to $30,500, or about 20%. This bounce doesn't look meaningful yet, but it

could develop into something significant. After all, cobalt is a useful

commodity that is becoming more useful over time due to the increasing

popularity of electric vehicles (EVs). There's a limit to how cheap it can

get.

The bounce from the early-August multi-year low will begin to

look significant if the price moves above the April-2019 rebound high,

that is, if the price moves above $35,000/tonne.

The surprising nickel rally

Over the past

several weeks most industrial metals markets have been in the doldrums,

but the nickel market has been 'on a tear'. The nickel price has gained

34% since early-July and is now at its highest level in more than four

years.

The most plausible explanation for the rapid rise in the nickel price

is a short-term supply shortage. This is evidenced in part by the

following chart, which shows that the amount of nickel in LME warehouses

has been in a steep downward trend and is now at a very low level. The

amount of an industrial metal in the reported LME inventory is often NOT a

good indicator of the overall physical supply-demand situation, but in

this case it is because a short-term tightness of physical supply is also

indicated by the LME futures curve (the nickel futures curve reveals a

slight backwardation over the remainder of this year).

We are long-term bullish on nickel due to the increasing demand for

this metal from the EV industry, but we didn't anticipate the recent price

surge and we have no opinion on what will happen to the price over the

next few months.

No evidence of a copper bottom, yet

The chart displayed below shows that the copper price is testing

intermediate-term support at $2.55-$2.60/pound. The support probably will

be breached before a sustainable low is in place, but there is at least

one reason to think that a breach of support will not be followed by a

substantial decline. The reason is sentiment.

The total speculative

net-short position in Comex copper futures is larger than it has ever

been. This limits the scope for additional short selling and creates a

set-up for a strong rebound.

Our guess is that the copper price

will bottom in the $2.40s within the next two months.

Oil: Short-term uncertain

Over the past two

months oil has traded in a choppy manner with a downward bias. It tested

its early-June low a couple of weeks ago and has since rebounded to a

confluence of resistance at $55-$57.

The futures curve tells us that the supply-demand situation in the

physical market is supportive for the price. We are referring to the fact

that the futures curve covering the next two years has a slight downward

slope. This indicates a market in slight backwardation, that is, a market

in which physical supply is a little tight (due to the cost of storage, if

the market were well supplied the futures curve would have an upward

slope).

Also, sentiment is constructive. Of particular relevance,

the "NonReportable" category of traders in NYMEX oil futures (the 'dumb

money') has built up its largest net-short position in almost three years.

The biggest short-term risk is linked to the positive correlation

between the oil price and the US stock market. Due to this relationship,

the oil price probably will come under irresistible downward pressure if

the US stock market does roughly what we expect and drops by 5%-10% within

the next few weeks.

Currently we are intermediate-term bullish on

oil and expect to become short-term bullish after we see evidence that the

stock market has made a multi-month bottom.

The Stock Market

The past as prologue

When the US stock market, as represented by the S&P500 Index (SPX),

makes a July high there is a strong tendency for it to fall by at least

10% to an August low and to reach an important turning point in October.

Most of the time the October turning point is a reversal from down to up.

This historical pattern is relevant at the moment, because the SPX

recently reversed downward from a July high.

Here are five examples

of the pattern described above:

1) 1998 contained the most common

version of the pattern. As illustrated below, the SPX plunged from a

mid-July high to an August low. It then rebounded to moving-average

resistance before dropping sharply to test its August low in

early-October. The October low marked the end of a multi-month correction.

2) In 1999, a mid-July high was followed by a sharp drop to an August

low. There was then a quick rebound that retraced about 70% of the initial

down-move followed by a choppy decline to a new 6-month low in

mid-October. The October low marked the end of a multi-month correction.

3) In 2007, a plunge from a mid-July high to a mid-August low was

followed by a rally to a marginal new all-time high in early-October. A

bear market then got underway.

4) 2011 was similar to 1998, with an October spike below the August

low proving to be a successful test of the low. As was the case in 1998

and 1999, the October low marked the end of a multi-month correction.

5) 2015 was similar to 1998 and 2011, but in this case the October low

did not mark the end of the correction. There was a strong rebound from

the October low to a secondary high in November, and then the

intermediate-term correction resumed. The correction low was in February

of the next year.

Turning to the 2019 year-to-date performance, the following chart

shows that we have a July high followed by a sharp pullback into August.

For the July-August decline to achieve the minimum magnitude suggested by

the pattern described above, this month's low will have to be 2725 or

lower. That is, at some point over the next two weeks the SPX will have to

trade at least 160 points (5.5%) below Friday's closing price. This is not

a forecast; it's an indication of what's possible in the near future given

what happened from a similar set-up in the past.

Current US Market Situation

The chart

displayed above shows that the SPX has oscillated in a fairly wide range

over the past two weeks, with plunges ending at around 2825 and rebounds

capped by the 50-day MA at around 2940. It ended last week near the

mid-point of this range.

The well-worn July-October pattern

discussed above suggests that the SPX will plunge to the low-2700s or

lower within the coming fortnight, but there is always more than one

possible outcome. Another possibility -- with a lower probability, in our

opinion -- is that a short-term correction ended last Thursday when the

early-August low was tested and that the SPX is now on its way to a new

all-time high. This lower-probability outcome likely would create an

excellent opportunity next month to purchase stock-index put options with

about 6 months to expiry, but we'll cross that bridge if we come to it.

The NASDAQ100 Index (NDX) has been stronger than the SPX, but its

chart position is similar. As with the SPX, the NDX was capped by its

50-day MA over the past two weeks.

Some US stock indices are positioned very differently than the SPX and

the NDX, however. For example, the following charts show that the Dow

Transportation Average (TRAN) and the Russell2000 SmallCap Index (RUT)

tested their 6-month lows last week. If the TRAN and the RUT soon take out

last week's lows it will confirm that the above-described July-October

pattern is in play for the SPX.

At the risk of muddying the waters, after being dangerously-optimistic

during the second half of June and the bulk of July, stock market

sentiment is now supportive. This is evidenced by the bottom section of

the following chart, which shows that late last week the 10-day MA of the

equity put/call ratio reached its second-highest level of the past three

years. The only time it was higher was near the December-2018 price

bottom.

The TSI Put/Call Indicator is not close to a buy signal,

but the recent surge in the equity put/call ratio suggests that the 'dumb

money' has become fearful very quickly. Sentiment being a contrary

indicator, this is bullish.

Summing up, other outcomes are certainly possible, but the following

comments from last week's Interim Update still reflect our assessment of

the highest-probability short-term outcome:

"...the short-term

downside target we have in mind for the SPX is the early-June low (around

2730). We expect this target to be reached within the next three weeks.

Given the bearish fundamental backdrop the SPX ultimately could drop a lot

further than that, but it should at least drop as far as its early-June

low before a multi-month bottom is reached."

Hong Kong

Anyone who hasn't been asleep for the past several weeks would know

that the people of Hong Kong (HK) have been protesting en masse and that

some of the protests have involved violent clashes with the police. The

protests initially were focused on a new law that would enable China's

government to extradite people from HK to the Mainland, but the demands of

the protesters have expanded to include an inquiry into police violence,

the granting of amnesty to everyone arrested during the protests to date,

the resignation of HK's current Chief Executive (Carrie Lam) and a change

to the political system to enable HK residents to elect their own Chief

Executive. For its part, China's government has made it clear that if the

large-scale civil disobedience continues then a branch of the Mainland

armed forces will be sent to HK to restore order.

Economically, the

biggest risk to HK is the possibility that China's military will intervene

to quell the protests. This would cause confidence to collapse and capital

to flee HK. It also would cause economic confidence to plunge globally, so

don't be thinking that what's happening in HK won't affect you

financially.

Military intervention from the Mainland is not the

most likely outcome, because it would be a reputational disaster for

China's government and an economic disaster for China. However, at this

point it is not clear how the conflict will end in the absence of military

intervention, because some of the protesters' demands are impossible

dreams. In particular, there is no way that China's government will allow

HK's Chief Executive to be elected via a true democratic process.

Our best guess at this time is that the HK government will make some

concessions to the protesters, including rescinding the extradition bill,

establishing an independent inquiry into the events of the past few months

and granting amnesty to many of those who were detained. This could be

enough to placate most of the protesters and enable order to be restored

peacefully. However, things could turn out much worse.

The

following chart of HK's Hang Seng Index (HSI) shows two 10%+ plunges over

the past four months. The first plunge was in May and was set in motion by

the rekindling of the US-China trade war. The second plunge began late

last month and was a reaction to the economic risks created by the

protests. A rebound began last week after the early-January low was

tested.

If the protests continue then the current rebound almost

certainly will be followed by a decline to new multi-year lows.

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date | Description |

| Monday Aug-19 | No important events scheduled |

| Tuesday Aug-20 | No important events scheduled |

| Wednesday Aug-21 |

FOMC Minutes Existing Home Sales |

| Thursday Aug-22 | No important events scheduled |

| Friday Aug-23 |

New Home Sales Jerome Powell speech at Jackson Hole |

Gold and the Dollar

As is the case with gold, the short-term risk/reward for the gold

mining indices/ETFs is now slightly bearish. There is a realistic chance

of a final surge to new highs for the year within the next couple of weeks

in dollar terms, but there's a high probability that the gold-mining

sector made a multi-month peak relative to gold bullion a few weeks ago.

Anyone with substantial exposure to gold (or silver) stocks should be

looking for opportunities to take money off the table or hedge in some

other way, for example by purchasing put options on ETFs such as GDX and

GDXJ. In particular, any strength over the next two weeks should be viewed

as a chance to hedge long positions.

The Currency Market

The week before last and early last week the Dollar Index (DX) tested

support at 97.2. After support held firm, the DX rose to test resistance

at 98.1.

We can't glean anything from this price action. The next

1-2 week move could be a rise to test the more important resistance at

around 98.7 or it could be continued 'choppiness' in the 97.2-98.1 range.

The Yen-gold relationship is interesting again.

As illustrated

by the following chart, there is a strong tendency for the Yen and the US$

gold price to trend in the same direction, but one generally leads the

other at short-term turning points. The Yen has been the leader since the

beginning of this year, having turned down before gold in Q1 and turned up

before gold in Q2.

At the moment the two markets are in synch, but

we are on the lookout for a divergence or non-confirmation. For example,

it would be significant if gold were to make a new high for the year

within the next two weeks while the Yen stayed below last week's high.

This would warn that a gold-price top was near.

Updates

on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() Company

news/developments for the week ending Friday 16th August 2019:

Company

news/developments for the week ending Friday 16th August 2019:

[Note: AISC = All-In Sustaining Cost, EBITDA = Earnings Before

Interest, Tax, Depreciation and Amortisation (a measure of cash flow), EV

= Enterprise Value or Electric Vehicle, FS = Feasibility Study, FY =

Financial Year, IRR = Internal Rate of Return, ISR = In-Situ Recovery, JV

= Joint Venture, MD&A = Management Discussion and Analysis, M&I = Measured

and Indicated, NAV = Net Asset Value, NPV(X%) = Net Present Value using a

discount rate of X%, NSR = Net Smelter Return or Net Smelter Royalty, P&P

= Proven and Probable, PEA = Preliminary Economic Assessment, PFS =

Pre-Feasibility Study]

*Alita Resources (A40.AX)

has requested (and been granted) the suspension of trading in its shares

pending an update regarding the previously announced Strategic Review,

offtake arrangements, operations at the Bald Hill Mine and discussions

with the Company's lenders. The voluntary suspension will remain in effect

until the earlier of an announcement to the market or 3rd September 2019.

We don't have any non-public information regarding what the company is

planning/negotiating and don't expect to know more until the

above-mentioned announcement is made.

*Alkane

Resources (ALK.AX) reported the initial results from a 60,000m

resource definition drilling program undertaken at the San Antonio and

Roswell targets, which are located within easy trucking distance of the

company's Tomingley Gold Operation (TGO). The initial 5,000m of drilling

included these significant gold intercepts from the San Antonio prospect:

36 metres grading 5.09g/t, 39 metres grading 3.59g/t and 9.7 metres

grading 8.01g/t.

There's a good chance that ore from the

aforementioned prospects eventually will enable a multi-year extension to

the TGO's life.

*Africa Oil (AOI.TO)

published its financial results for the June-2019 quarter.

At 30th

June the company had no long-term liabilities to speak of, US$312M of

working capital and US$67M of equity investments (a 34.5% stake in Africa

Energy Corp (AFE.V), an 18.8% stake in Eco (Atlantic) Oil and Gas (EOG.C),

and a 30.1% stake in private company Impact Oil and Gas), that is, the

company had US$379M of working capital plus equity investments (WC+EI).

This compares to US$393M of WC+EI at the end of the preceding quarter and

$407M of WC+EI at the end of last year.

Note that AOI accounts for

its equity investments at cost rather than current market value.

Currently, the market value of these investments adds up to about US$118M,

or US$51M more than the amount included on AOI's balance sheet.

The

company's main operating costs are expenditures associated with appraisal

activities and developments studies at the 25%-owned South Lokichar Basin

oil project in Kenya. It is expected that over the next few years South

Lokichar will be developed into a producing oil field with output of

around 100K barrels of oil per day (bopd).

In addition to its 25%

stake in South Lokichar and its equity investments, AOI is in the process

of acquiring 12.5% of a company that holds interests in multiple offshore

oil fields in Nigeria. This is a major acquisition that when complete will

immediately transform AOI from an oil explorer/developer to a profitable

oil producer. However, the completion time is unknown.

Accounting

for AOI's equity investments at market value and converting USD to CAD,

the WC+EI amount is C$573M. This equates to C$1.22/share, meaning that if

you buy AOI at the current price of C$1.12/share you effectively get the

company's South Lokichar stake for free.

*Cobalt 27

(KBLT.V) advised that the meeting of shareholders to vote on the

proposed takeover by Pala Investments has been scheduled for 12th

September.

More information regarding the takeover was provided in

a Management Information Circular (MIC) filed by the company on 14th

August. Here are two of the most interesting pieces of new information:

1) According to the MIC, when determining the value of the cobalt

assets to be acquired by Pala the current very-depressed market value was

used, whereas the other (mainly nickel) assets that would go into the new

company called Nickel 28 have been valued at cost or above cost. This

explains how management can claim that Nickel 28 is worth C$2.18/share at

the same time as the market is implying a value of only about

C$0.40/share.

2) We noted in the 15th July Weekly Update that if

the takeover is successful then KBLT's existing managers will receive

change-of-control payments and will manage the spin-out company (Nickel

28), that is, they will receive financial bonuses for having sold near an

all-time low AND continue to draw their salaries. We now know the

magnitudes of the change-of-control payments. According to page 46 of the

MIC, Anthony Milewski (CEO and Chairman) will receive a US$7.7M bonus and

Justin Cochrane (COO and President) will receive a US$5.3M bonus.

Also worth mentioning is that the press release that announced the meeting

date and the MIC filing contained the following statement: "Cobalt 27

is expected to have up to $48.5-million (U.S.) of net corporate debt on

closing of the arrangement ... [that] will be repaid by Pala. Absent the

transaction, Cobalt 27 would need to service and repay the majority of the

aforementioned debt using its own resources."

This creates the

impression that KBLT could be under financial pressure due to the US$48M

of outstanding debt if the Pala takeover is not approved, which absolutely

is not the case. First, repayment of the debt is not due for three years.

Second, KBLT has a US$100M credit facility plus a US$50M accordian

facility, meaning that it still has more than US$100M of unused credit.

Third, the company has cobalt in storage with a current market value of

about US$90M, or almost double the current amount of debt.

The

proposed takeover is a very bad deal for shareholders (other than Pala) so

we strongly suggest voting AGAINST it.

*Golden Arrow

Resources (GRG.V) advised that the meeting of shareholders to

vote on the proposed sale of GRG's 25% stake in the Pirquitas-Chinchillas

mining operation in Argentina has been scheduled for 16th September.

We aren't as 'anti' this deal as we are the KBLT deal mentioned above.

Unfortunately, it seems that the silver rally started about three months

too late for GRG and the company found itself in a difficult financial

situation.

If the sale is approved then GRG will end up with liquid

financial assets (cash plus SSRM shares) worth about C$0.24/share and a

portfolio of exploration-stage assets in Argentina, Chile and Paraguay. In

other words, the stock should be worth C$0.24 even if no value is assigned

to the exploration portfolio. We think it's fair to assign an option value

of at least C$10M to the exploration portfolio, resulting in a minimum

total value per share of C$0.33. This is double the current stock price.

*Peyto Exploration & Development (PEY.TO)

confirmed its monthly 0.02/share dividend. At the current share price the

annual dividend yield is about 8%.

The stock has been trading as if

the dividend is under threat. Up until now the company has been generating

more than enough cash to fund the dividend, so we expect it to be

maintained and eventually increased. However, we can't rule out the

possibility that the dividend will be reduced in the short term for risk

management purposes.

*Sabina Gold and Silver

(SBB.TO) published its financial statements for the June-2019

quarter. They show that the company had C$27.7M of working capital (and no

long-term debt) at 30th June, which is down from C$34.5M at the end of the

preceding quarter. During the June quarter the company raised C$5.2M to

fund an exploration program designed to expand the existing resource, so

cash consumption during the quarter was C$12M.

SBB's Back River

gold project is fully permitted and construction ready, but up until now

the company has been unable to raise the equity portion of the US$330M

needed to fund the pre-production capex on reasonable terms. It therefore

has focused on reducing project risk and growing the high-grade resource

pending an improvement in market conditions. Market conditions clearly

have improved over the past two months, but probably not by enough to

enable construction financing to be arranged at an acceptable cost.

We expect that SBB eventually will be taken over by a larger company

such as Agnico Eagle, but ideally the takeover bid won't come until after

the stock price has moved above C$2.00. In the meantime, the biggest

company-specific short-term threat to the stock price is an equity

financing to top-up the treasury. The company has enough cash to fund

itself until year-end, but management probably won't want the working

capital to drop below about C$15M. Therefore, it's likely that C$10M-C$20M

of new shares will be issued within the next three months.

![]() List

of candidates for new buying

List

of candidates for new buying

From within the ranks of TSI

stock selections the best candidates for new buying at this time, listed

in alphabetical order, are:

1) ALK.AX (last Friday's closing price:

A$0.41)

2) GRG.V (last Friday's closing price: C$0.16)

3)

KBLT.V (last Friday's closing price: C$3.86)

4) PEY.TO (last

Friday's closing price: C$3.18)

5) PG.TO in the low-C$2 area (last

Friday's closing price: C$2.16)

The above list is limited to five

stocks. It sometimes will contain less than five, but it never will

contain more than five regardless of how many stocks are attractively

priced for new buying.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/

https://www.lme.com/

https://www.kitco.com/