![]()

![]()

![]()

![]()

-- Weekly Market Update for the Week Commencing 19th December 2016

Big Picture

View

Here is a summary of our big picture

view of the markets. Note that our short-term views may differ from our

big picture view.

The BULL market in US Treasury Bonds that began in the early 1980s ended in early-2015, but there will be many years of topping action in bond prices and bottoming action in bond yields before major new trends get underway. (Last update: 29 June 2015)

The stock market, as represented by the S&P500 Index, commenced a secular BEAR market during the first quarter of 2000, where "secular bear market" is defined as a long-term downward trend in valuations (P/E ratios, etc.) and gold-denominated prices. This secular trend will bottom sometime between 2018 and 2020. (Last update: 29 June 2015)

A secular BEAR market in the US Dollar began during the final quarter of 2000 and ended in July of 2008. This secular bear market will be followed by a multi-year period of range trading. (Last update: 09 February 2009)

Gold commenced a secular bull market relative to all fiat currencies, the CRB Index, bonds and most stock market indices during 1999-2001. This secular trend will peak sometime between 2018 and 2020. (Last update: 29 June 2015)

Commodities,

as represented by the CRB Index, commenced a

secular BULL market in 2001 in nominal dollar terms. The first major

upward leg in this bull market ended during the first half of 2008, but

a long-term peak won't occur until 2018-2020.

(Last

update: 29 June 2015)

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Outlook Summary

|

Market |

Short-Term (1-3 month) |

Intermediate-Term (6-18 month) |

Long-Term (2-5 Year) |

| Gold | N/A |

Neutral (21-Nov-16) |

Bullish |

| US$ (Dollar Index) | N/A |

Neutral (17-Aug-16) |

Neutral (19-Sep-07) |

| US Treasury Bonds (TLT) | N/A |

Neutral (21-Nov-16) |

Bearish |

| Stock Market (DJW) | N/A |

Neutral (14-Nov-16) |

Bearish |

| Gold Stocks (HUI) | N/A |

Neutral (21-Nov-16) |

Bullish |

| Oil | N/A |

Neutral (26-Oct-15) |

Bullish |

| Industrial Metals (GYX) | N/A |

Neutral (10-Oct-16) | Bullish |

4. Long-term views are determined almost completely by fundamentals and intermediate-term views

are determined by a combination of fundamentals, sentiment and technicals.

Last week's posts at the TSI Blog

The second most overbought market since 1980

How the fundamental backdrop could turn bullish for gold

Summary of current

thinking/positioning

1) Continuing to expect that the

overall corrections/downturns for gold and the associated mining indices

will extend into Q1-2017, but anticipating an intervening rebound. The

rebound could get underway immediately, but it looks more like being

delayed until early-January.

2) Expecting that 2017 will be a

bullish year for commodities. Maintaining long-term exposure to non-gold

commodities while acknowledging that the early-2016 lows could be tested

in Q1-2017 prior to the start of the aforementioned bullish period.

3) Expecting a decline in the oil price to a January-February bottom

and positioned for this outcome via USO put options expiring in February.

In addition to being a speculation, these options have been purchased as a

hedge against short-term weakness in commodity-related equities.

4)

Thinking that government bonds have commenced a long-term bear market, but

that the US Treasury Bond is close to a short-term price bottom.

5)

Expecting a 6-12 month extension of the equity bull market and looking for

opportunities to add to general non-US equity exposure.

6) Thinking

that the Dollar Index is close to a 1-2 month top, but that it won't reach

a major top before the second quarter of 2017.

7) Maintaining a

large cash reserve in recognition of the short-term downside risk in most

equities (current cash percentage is about 35%), but putting some cash to

work in small-cap gold stocks that could rebound strongly within the next

6 weeks.

Reminder about

TSI Christmas schedule

As advised last week, there will

be no Interim Update this week and no Weekly Update next weekend. However,

we will send out a brief market update via email at the end of this week.

What is the US

Treasury up to?

A week ago we mentioned that the

US Treasury had just 'injected' $66B into the US economy and that this

monetary injection could have been partly responsible for the preceding

week's stock market surge. For ease of reference, here's what we wrote:

"The explanation [for the surprising recent stock market strength]

revolves around the US government's account at the Fed, called the US

Treasury General Account. When money goes into this account (due to tax

receipts and borrowing), the money is temporarily removed from the

economy. The money is then returned to the economy when it is spent by the

government.

As discussed in two blog posts (HERE

and

HERE) over the past few months and in the 17th October

Weekly Update, the government has been holding an unusually-large amount

of money in its Fed account and therefore causing monetary conditions to

be a little tighter than would otherwise be the case. Specifically, from

November of 2015 through to November of this year the US government

effectively removed almost $400B from the US economy.

During the

week ending Wednesday 7th December they 'returned' $66B to the economy.

It's possible that this sudden monetary injection had a positive effect on

the stock market."

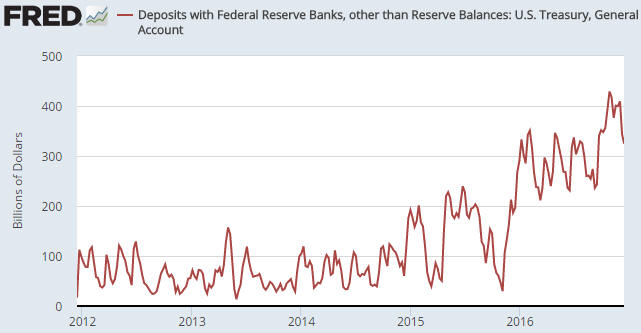

During the latest week the Treasury

released another $19B of cash into the economy, bringing the two-week

total to $85B.

Before we hazard a guess as to why this happened

it's worth taking a step back and quickly reviewing the shifts over the

past year in the amount of money held by the Treasury in its account at

the Fed. These shifts are illustrated below.

With reference to the

following chart, notice that there was a dramatic rise in the amount of

money held in the Treasury's account during the 3-month period beginning

in early-November of last year. Over this period the government added

about $320B to its cash deposit and therefore effectively removed this

amount from the economy and the financial markets. It's not a fluke that

this withdrawal of money occurred in parallel with a steep stock-market

decline.

The amount of money held in the Treasury's account then

oscillated within a $100B range for a few months before embarking on

another large rise in mid-September. Specifically, from mid-September

through to late-October the Treasury removed about $190B from the economy

and the financial markets.

The monetary value of the account peaked

in late-October at around $430B and has since declined to $325B, with the

bulk of the decline happening over the past two weeks.

The swings in the Treasury's account are strange, for two reasons.

First, they would have tended to reduce economic activity during the

months leading up to the election and boosted economic activity after the

election. This is strange because we are taking about an incumbent

Democratic administration taking actions that could only have hurt

Clinton's chances in the Presidential election and that fueled the

financial-market celebrations in the wake of the Trump victory. Second,

the main reason for the cash build-up was supposedly to provide a buffer

that could be used during the next 'debt ceiling stand-off' (the period of

inter- and intra-party haggling that occurs when the current federal debt

limit is reached or expires). With the next debt ceiling stand-off due to

begin by March-2017, this would seem to be an inopportune time to be

reducing the cash buffer.

The explanation for why the Treasury

added about 400 hundred billion dollars of cash to its Fed deposit -- and

therefore removed the same amount from the economy -- between November of

last year and October of this year appears to be relatively

straightforward. It was a response to a recommendation by the

Treasury Borrowing Advisory Committee (TBAC) to accumulate a $500B

emergency cash reserve. That establishing this reserve would dampen

economic activity during the 12 months leading up to the Presidential

election probably wasn't considered important, because it was probably

believed that a Clinton victory was 'a lock'.

The explanation for

why the Treasury is now disgorging cash and giving both the stock market

and the economy a TEMPORARY boost is less straightforward and relies on

guesswork. Our guess is that with a Republican moving into the White House

and with the Republican Party in control of both legislative chambers (the

Senate and the House of Representatives), the Obama Administration has

decided to spend whatever money it can before it departs. Having very

little cash in reserve prior to an imminent 'debt ceiling standoff' will

potentially create a substantial problem for the Trump Administration to

deal with. Also, the superficial impression will be created that the

Democrats left the economy in good shape.

The probability that our

guess is correct will increase if the Treasury's General Account continues

to be drawn down prior to Trump's 20th January Inauguration.

Lastly, we emphasised the word "temporary" above because injecting money

into an economy can never cause real progress and because we are talking

about a fixed amount of money that will soon be depleted if the injections

continue.

Commodities

Copper

The copper price made a double top in the $2.70s during November and has

pulled back to the mid-$2.50s. A normal correction could take the price as

far down as the low-$2.30s to 'test' the early-November upside breakout.

Despite no longer being 'overbought' in momentum terms there is still

significant short-term downside risk in the copper market. The risk stems

in part from the recent weakness in the gold price, in that gold could be

leading other metals to the downside just as it led to the upside a year

ago. It also stems from the fact that the speculative net-long position in

Comex copper futures hit an all-time high last week.

With

short-term speculators in copper futures now rampantly bullish about

copper's prospects there could soon be another surge to a new 12-month

high in the copper price, but this would only increase the risk. The

problem is that if/when it starts to look like copper's upward trend is

over, a lot of long-positioned speculators are bound to rush for the exit

at the same time.

Oil

The oil price broke

above its June and October highs early last week in response to the

re-cycling of the same old (irrelevant) OPEC news. It then reversed

course. This price action has altered the chart pattern and has possibly

defined a new price channel.

The breakout that happened early last week hasn't yet been negated and

suggests the potential for the oil price to rise to the low-$60s before

the start of the next tradable decline. However, if the channel we've

drawn on the above chart is valid then a) the entire rally from the

early-August low is probably a counter-trend move within an

intermediate-term correction/consolidation that began in June, and b) a

decline to below the August low has probably just begun.

The

divergence between the Canadian Dollar (C$) and the oil price was

magnified by last week's market action. As illustrated below, the C$ made

a clear-cut downward reversal from its channel top and its 200-day MA

during the first half of last week.

The divergence will most likely

be closed by the oil price making a catch-up move to the downside,

although the possibility that it will be closed by the C$ making a

catch-up move to the upside cannot be ruled out. In the financial markets

there are no guarantees, only probabilities.

The Stock Market

The US

The NASDAQ100 Index (NDX) broke above resistance near 4900 last week and

in doing so removed a short-term bearish non-confirmation. The breakout

projects a rise to at least 5100 over the weeks ahead.

In the TSI List there is a bearish NDX speculation in the form of QID

(a leveraged bear fund) $30 call options expiring in January. The same

options are in our own account*. There is still a chance that something

will happen to inject significant value into these options prior to their

20th January expiry date (a quick decline of about 15% would do it), but

the chance is now so small that we have assumed that they will expire

worthless and written them down to zero.

We expect that there will

be meaningful (8%-12%) declines in the senior US stock indices from

whatever highs are in place by early-January, but at this stage we don't

know if it will be appropriate to attempt a new short-term bearish trade

given that the market's overall upward trend looks set to extend into the

second half of next year.

Before leaving the US stock market we

want to point out that the Dow Jones Utility Average (UTIL) has broken

upward from the downward-sloping channel that began to develop at this

index's early-July peak. The utility sector is primarily a dividend play

that is influenced by the bond market and/or expectations regarding future

bond yields, so UTIL's up-turn is consistent with our view that the T-Bond

will soon begin to rebound.

*It's worth reiterating that while we will

generally have positions in most (not all) of the stocks/warrants/options

included in the TSI List, the TSI Stocks List is not a reflection of our

portfolio and neither is it supposed to be a recommended or model

portfolio. It is a list of speculating/investing ideas that TSI

subscribers can draw from.

Europe

Prior to the surge in the US money-supply growth rate over the past two

months, the main thing in the US stock market's favour was the major

basing patterns evident in European and Japanese stock indices. For

example, since July it has looked like the EURO STOXX 50 Index (STOX5E)

completed a double bottom during the first half of this year.

The

basing-pattern interpretation of the STOX5E's 2016 performance was

recently confirmed via a decisive break above resistance at 3150 (the top

of the base). There could be a pullback to around 3150 to 'test' the

breakout within the next two months, but the price pattern suggests that

STOX5E will challenge its 2015 high during 2017.

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date | Description |

| Monday December 19 | No important events scheduled |

| Tuesday December 20 | No important events scheduled |

| Wednesday December 21 | Existing Home Sales |

| Thursday December 22 |

Durable Goods Orders Q3 GDP (2nd revision) Personal Income and Spending Leading Economic Indicators |

| Friday December 23 | New Home Sales |

Gold and the Dollar