--

Weekly Market Update for the Week Commencing

20th August 2018

Big Picture

View

Here is a summary of our big picture

view of the markets. Note that our short-term views may differ from our

big picture view.

The BULL market in US Treasury Bonds

that began in the early 1980s ended in mid-2016, but there will be many years

of topping action in bond prices and bottoming action in bond yields before

major new trends get underway. A major decline in government bond prices will

unfold during the 2020s. (Last update: 11 September 2017)

The stock market, as represented by the S&P500 Index,

commenced

a secular BEAR market during the first quarter of 2000, where "secular

bear market" is defined as a long-term downward trend in valuations

(P/E ratios, etc.), gold-denominated prices and inflation-adjusted prices. This secular trend will bottom

in 2020 or later.

(Last update: 11 September 2017)

A cyclical BEAR market in the

US

Dollar

began in 2016-2017.

(Last

update: 11 September 2017)

Gold commenced a

secular bull market relative to all fiat currencies, the CRB Index,

bonds and most stock market indices during 1999-2001.

This secular trend will peak in 2020

or later.

(Last update: 11 September 2017)

Commodities,

as represented by the CRB Index, commenced a

secular BULL market in 2001 in nominal dollar terms. The first major

upward leg in this bull market ended during the first half of 2008, but

a long-term peak won't occur until 2020 or later.

(Last

update: 11 September 2017)

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

True

Fundamentals Summary

[Notes:

1) The date shown next to the current True Fundamentals Model (TFM) signal is

when the most recent change occurred. 2) Charts of the Gold and Equity

TFMs are included in the "Charts and Indicators" section of the TSI web

site]

|

Market |

True Fundamentals Model (TFM) |

|

Gold (US$ Price) |

Bearish (20 Jul 2018) |

|

US Equity (SPX) |

Bearish (29 Jun 2018) |

|

Currency (Dollar Index) |

Bullish (27 Apr 2018) |

|

Commodities (GNX) |

Bearish (01 Jun 2018) |

Last week's posts at the TSI Blog

Gold: Bearish fundamentals, bullish sentiment

The next

major gold rally

Summary of current

thinking/positioning

1) The Dollar Index has

consolidated its upside breakout and probably will extend its upward trend

into September.

2) Gold-market sentiment is extreme, but an upward

reversal has not been signaled. This leaves the door open to new 2018 lows

prior to a meaningful rally getting underway. Unlike recent years when the

gold market sold off during the final quarter and made a tradable low in

December, due to the extension of the downward trend into August and

possibly September there is more likely to be a final-quarter rally in the

gold market this year.

3) Last week, capitulation finally occurred

in the gold-mining sector. The price plunge prompted us to take profits on

GDX put options that were bought for hedging purposes, although it is not

clear that the capitulation has run its course.

4) There are

numerous divergences within the US stock market, but the senior stock

indices have not yet shown significant signs of weakness. This means that

new highs could be achieved before a tradable decline gets underway.

However, with monetary conditions tightening, the short-term downside risk

is high.

5) Most industrial commodities probably will remain in

correction mode for another 1-2 months. Also, after being relatively

strong for the bulk of the past 12 months the oil market looks set to be

relatively weak for the next few months.

6) The T-Bond price should

have an upward bias (meaning: the T-Bond yield should have a downward

bias) for at least the next two months.

7) We are holding a cash

reserve of around 35%.

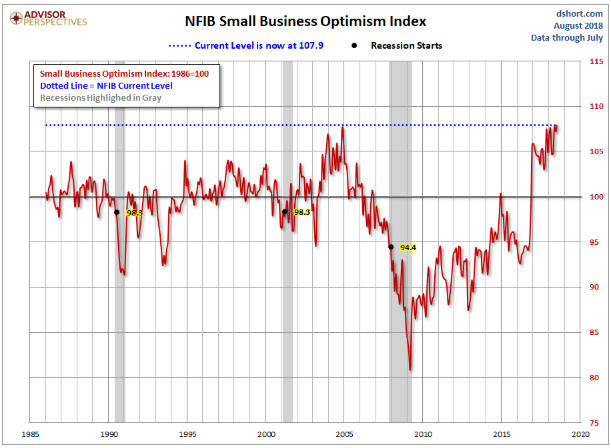

Another leading

indicator of US recession

Sorry to be the bearer of good

news, but the following chart shows that the NFIB Small Business Optimism

Index just hit an all-time high. While this probably means that the US

economy is as good as it is going to get, it also means that there is

little chance of a recession getting underway before next year. The reason

is that previous recessions didn't begin until after the Optimism Index

sunk below 100. Even if now is the economic peak it likely will be at

least 6-12 months before the index sinks below 100.

The message

from the Small Business Optimism Index is therefore consistent with the

message from our three favourite leading indicators of US recession.

Chart source:

dshort

The True

Fundamentals

The fundamentals of a market are

the underlying forces that drive the market's valuation. In the short-term

the valuation of a market can be dominated by changes in speculative

sentiment, but intermediate-term and long-term price trends are driven

primarily by fundamental factors.

Interestingly, most people who

write about the major financial markets don't understand the markets' most

important fundamentals. For example, it is common for all sorts of things

that have either no influence or very little influence on the gold price

to be cited as important gold-market fundamentals. We've mentioned these

fake gold-market fundamentals many times in the past, such as in the

second paragraph of the blog post linked

HERE.

For another example, it is widely believed that the rate of corporate

earnings growth is an important, perhaps even the most important, driver

of the stock market, but over the long-term there has been no correlation

between the S&P500's earnings growth during a 12-month period and the

S&P500's performance during the same period. The rate of earnings growth

therefore should not be part of a fundamentals-based stock market model.

The stock market is driven by the amount that investors are prepared to

pay for current earnings, which, in turn, is influenced by the rate of

money-supply growth, economic confidence as indicated by credit spreads,

inflation expectations, interest rates, confidence in the banking system

and the willingness to take on debt.

Based on logic and historical

correlations, we developed True Fundamentals Models (TFMs) for gold, US

equities, the US$/euro exchange rate (in effect, the Dollar Index) and

commodities in general. The outputs of these models are included in a

table that appears near the top of every Weekly Market Update.

We

have been taking the inputs to these models into account for a long time

(in gold's case, about 18 years) at a qualitative level, but it was only

about a year ago that we attempted to fully quantify the fundamental

backdrop. A big part of the reason for doing so was to remove our 'gut

feel' from the equation. If you are a gold bug or an Austrian economics

devotee then your gut feel will often be something like: "a global

economic collapse is imminent!"

We aren't sure, yet, how much

weight to place on the TFMs when analysing the various markets. After all,

it isn't uncommon for sentiment and technical considerations to override

the fundamentals in the short-term. Overall, though, the TFM signals have

been quite good to date. For example, apart from the first half of July

the output of our Gold TFM has been consistently bearish since

mid-January. Considering gold's performance, this was a useful signal. For

another example, our Commodities TFM shifted from bullish to neutral in

mid-April, about a month prior to the year-to-date top for GNX (the GSCI

Commodity Index), and shifted from neutral to bearish at the beginning of

June, just prior to steep price declines getting underway in many

commodities.

The fundamental situation as reflected by our TFMs

should be viewed as pressure, with a bullish situation putting upward

pressure on the price and a bearish situation putting downward pressure on

the price. Sentiment and technical considerations can override the

fundamentals in the short-term, but if the fundamental pressure is

maintained then the price should eventually move in that direction.

A recent example is the Dollar Index (DX). Apart from a single week in

April, our US$ TFM has been bullish since mid-December of last year. In

the face of this US$-bullish fundamental backdrop, the DX promptly fell

from 93.5 to 88 and then chopped around in the 88-90 range for about three

months before beginning to trend upward. The fundamental pressure

eventually gained the upper hand.

The US stock market is the one

market that hasn't yielded to fundamental pressure over the past few

months. Apart from one week in June, our Equity TFM has been bearish since

late-May. It has not been warning of a bear market (there are different

levels of bearishness), but for almost three months it has been warning of

an intermediate-term correction. That's far from unprecedented, though, as

this model tends to be much better at generating timely bear-market

warning signals than at warning in a timely manner of intermediate-term

bull-market corrections.

The longer we track these models the

better will be our understanding of how they can be used for speculating

and investing.

Don't be short

the US Treasury market

On a long-term basis the 10-year

T-Note appears to have completed a top. The long-term pattern suggests

that the price will be much lower and the yield will be much higher a year

from now. However, on a short-term basis a "head and shoulders" bottom

appears to be almost complete (see chart below). Also, the total

speculative net-short position in 10-year T-Note futures made a new

all-time high last week, meaning that the sentiment situation is very

supportive.

The combination of sentiment and price action indicates

that the 10-year T-Note has a favourable short-term risk/reward.

Therefore, it doesn't make sense to be betting against this market at the

moment.

Getting close to a

copper bottom

The copper price traded as low as

$2.55 last Wednesday, meaning that it came within a few cents of major

support and the target that was created when it completed its topping

pattern in June.

There could be a full test of major support at

$2.48-$2.50 before a multi-month bottom is in place, but in price terms at

least 90% of copper's downward correction is probably out of way.

The Stock Market

The US stock market managed to

get through another week without doing anything significant. As

illustrated by the following daily chart, the SPX traded in a narrow range

below resistance defined by its channel top and its January high.

That being said, the bottom section of the following chart shows that the

NYSE Advance-Decline line extended its upward trend by making a new high

on Friday. This warns that the SPX will break above resistance in the near

future.

While the SPX stands a good chance of making at least a marginal new

high soon, some important US stock indices are in dicey positions. For

example, the Homebuilders ETF (XHB) has dropped below the bottom of its

long-term channel and is not far from long-term lateral support at $38.50.

Ending a week below this lateral support would leave little room for doubt

that a major top was put in place in January of this year.

If XHB breaks below the aforementioned support it will be evidence

that the US real estate boom is over. On the other hand, if the support

holds then it will be reasonable to assume that the January-2018 peak was

just the intermediate-term variety and another bull-market leg lies ahead.

We currently have no position in XHB, but with the price so close to a

critical level it could make sense to buy both put options and call

options on the expectation that a big move in one direction or the other

will get underway soon.

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date |

Description |

|

Monday Aug-20 |

No important events scheduled |

|

Tuesday Aug-21 |

No important events scheduled |

|

Wednesday Aug-22 |

Existing Home Sales

FOMC

Minutes |

|

Thursday Aug-23 |

New Home Sales |

|

Friday Aug-24 |

Durable Goods Orders |

Gold and the Dollar

Gold

Sentiment vs Fundamentals

For gold, the

fundamental backdrop remains very bearish and the sentiment backdrop remains

very bullish. It is not possible for an intermediate-term rally to occur in the

gold market in the face of a bearish fundamental backdrop, but a strong 1-3

month rebound is certainly possible.

It should always be kept in mind

that sentiment typically follows price. There is nothing like a strongly-rising

price to get the speculating community and the general public bullish and there

is nothing like a steep price decline to get them bearish. Therefore, important

price lows will invariably coincide with mass negativity, but the fact that

there is mass negativity won't always imply that the price is close to its

nadir.

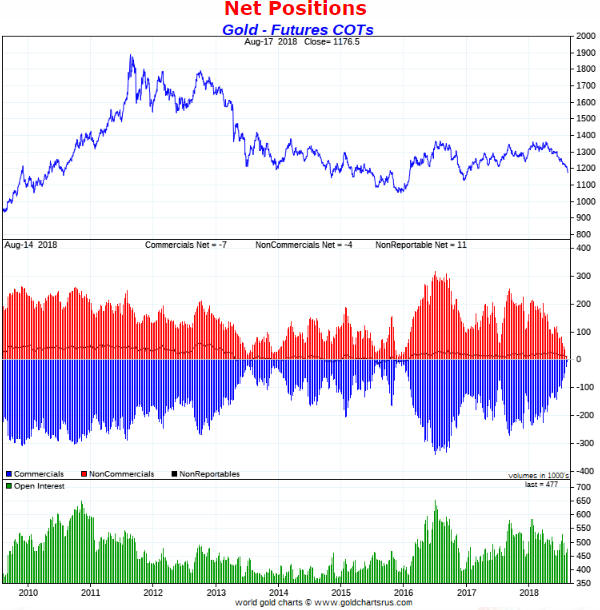

By some measures, speculative sentiment in the gold market is now

more negative than it has been at any time since 2001. For example, the

following chart shows that the total speculative net-long position in gold

futures is the smallest it has been since 2001 (the total speculative net-long

position is the inverse of the commercial net-short position, which is indicated

by the blue bars in the middle section of the chart).

What's not shown on

the following chart, though, is that speculators in gold futures were

consistently bearish and short throughout 1995-2001 while the price trended

downward. Therefore, if the price continues to trend downward with nothing more

than 1-3 month rebounds along the way, which it will if the fundamental backdrop

continues to be a head-wind, then the speculating community will become

increasingly bearish and the COT situation will become increasingly 'extreme'

compared to the post-2001 period.

To put it succinctly, the key to a

sustainable up-turn in the gold market is the fundamental situation, not

sentiment.

Current Market Situation

In last

week's Interim Update, we wrote:

"What we have is a market that is

now very 'oversold' with the sort of sentiment that is often associated with an

important price low, but also a market that is yet to provide any evidence that

a low is in place. The first sign would be a daily close above $1210 or the

20-day MA, whichever is lower."

Nothing has changed.

The

gold market was 'oversold' when it bounced off $1240 in early-July and when it

bounced off $1210 in mid-July. It is also 'oversold' now, having just bounced

from last week's low of $1167. At this time there is no way of telling whether

the latest bounce marked the start of a meaningful rally or the start of another

consolidation within a continuing short-term downward trend.

Taking a wider-angle view, the following weekly chart shows gold's performance

over the past 20 years.

Referring to the bottom section of the chart,

notice that the recent decline has taken the weekly RSI well below 30 and that

the only other times this happened over the past 20 years were Q2-2013 and

mid-1999. These were both bear-market years. During the bull-market years of

2001-2011 the weekly RSI never became anywhere near as low as it is now.

The extremely-low weekly RSI suggests that there will be a very strong, but

short-lived, rebound from last week's low or whatever new low is made over the

coming month.

Gold Stocks

Last week we got the capitulation in the

gold-mining sector that we were concerned about over the preceding few weeks. Is

that it? Is a sustainable low in place?

Probably not. While it is

certainly possible that the gold-mining indices and ETFs made short-term bottoms

on Thursday 16th August, at this time a reversal has not been signaled.

If Friday's rebound had started after a spike to well below Thursday's low then

there would be a good chance that the capitulation was over. However, it turned

out that Friday was an "inside day" for the gold-mining indices and ETFs. In

other words, Friday's trading took place inside Thursday's range. For an

illustration, refer to the following daily chart of the HUI. This doesn't

eliminate the possibility that the gold sector has bottomed, but it puts the

odds in favour of a spike to a new low prior to a price bottom that holds for at

least a few months.

Further to our comments in last week's Interim Update, it's likely that the

downward trend's momentum extreme, as measured by the daily RSI, is in place.

That's regardless of whether or not there are new price lows over the weeks

ahead. Also, the short-term scenarios outlined in last week's Interim Update

remain applicable. The most likely scenario involves a bottom, but not the final

bottom, before the end of this month at or not far below last Thursday's low,

while a sharp drop to a new low for the move during the first half of this week

could create a more sustainable bottom.

The Currency Market

Last week the Dollar Index (DX) consolidated the preceding week's upside

breakout. Additional upside is likely prior to a multi-month top.

Based on sentiment indicators, we expect that the DX's next multi-month top will

be in place by mid-September. That's regardless of whether or not the

fundamental backdrop remains US$-bullish. Also, although the odds are in favour

of additional gains prior to a multi-month top, a daily close below 95.5 during

this week would be a preliminary warning that such a top was already in place.

With regard to the technical situation, the next piece of important evidence

will be the August monthly close. The DX broke out to the upside on a weekly

closing basis when it closed above 95.1 during the week before last, but that

breakout has to be confirmed by a monthly close above the same number.

According to the US Treasury, the "Treasury International Capital (TIC)

reporting system collects data for the United States on cross-border portfolio

investment flows and positions between U.S. residents (including U.S.-based

branches of firms headquartered in other countries) and foreign residents

(including offshore branches of U.S. firms)." In other words, the TIC

reports quantify investment flows from other countries to the US and investment

flows from the US to other countries.

The TIC reports are published with

too much of a lag to be useful in real-time analysis (for example, the report

for June was only published last week), but they can still be interesting. This

is because they can reveal whether a prior move in the US$ was driven primarily

by investment capital flows (fundamentals) or speculative trading of currency

futures.

As noted in the article posted

HERE:

"The June TIC data was reported yesterday [15th August], and there was a

net purchase of $114.5 bln of US assets. It was the third month this year that

the inflows surpassed $100 bln, matching the number in all of 2017 and exceeding

the number of months in 2016. According to this authoritative even if not

comprehensive report, foreign investors bought $417.4 bln of US assets in Q2,

the most in any quarter for a decade. That brings the first half inflow to $538

bln, also the most since 2008 and sufficient to cover the entire year's current

account deficit."

That is, the TIC numbers for June suggest that the

US dollar's recent strength was mainly the result of relatively strong demand

for US$-denominated assets (fundamentals), although we won't know the full story

until the numbers for July and August are published in mid-September and

mid-October.

Updates

on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Company

news/developments for the week ending Friday 17th August 2018:

Company

news/developments for the week ending Friday 17th August 2018:

[Note: AISC = All-In Sustaining Cost, FS = Feasibility Study, FY = Financial

Year, IRR = Internal Rate of Return, ISR = In-Situ Recovery, MD&A = Management

Discussion and Analysis, M&I = Measured and Indicated, NAV = Net Asset Value,

NPV(X%) = Net Present Value using a discount rate of X%, NSR = Net Smelter

Return, P&P = Proven and Probable, PEA = Preliminary Economic Assessment, PFS =

Pre-Feasibility Study]

*Africa Oil (AOI.TO)

published its financial results for the June-2018 quarter.

At 30th June

the company had no long-term liabilities to speak of, US$380M of working capital

and US$59M of equity investments (stakes in Africa Energy Corp, Eco (Atlantic)

Oil and Gas, and Impact Oil and Gas), that is, the company had US$439M of

working capital plus equity investments (WC+EI). This compares to US$451M of

WC+EI at the end of the preceding quarter and US$453M at the end of last year.

AOI's flagship asset is 25% of the large development-stage South Lokichar

Basin in Kenya. The rest of the project is owned by Tullow Oil (operator, 50%

stake) and Total (25% stake). It is expected that over the next few years South

Lokichar will be developed into a producing oil field with output of around 100K

barrels of oil per day (bopd). The initial stage is estimated to have total

capex of US$2.9B and result in production of 60K-80K bopd.

AOI's share of

the initial capex would be US$725M, a significant chunk of which could be

required as soon as next year. Thanks to a) AOI's current cash hoard, and b)

Total's obligation, as part of an agreement that AOI had with Maersk Oil (Total

purchased Maersk Oil last year), to pay up to US$405M of AOI's development

expenses, funding this capex should not be problem. In any case, we suspect that

AOI will be taken over by Total after a Final Investment Decision (FID) is made

by the JV partners, that is, before it has to 'pony up' its share of the initial

capex. The current schedule is for the FID to be made in 2019.

At today's

exchange rate and total share count, the WC+EI amount of US$439M mentioned above

equates to C$1.22/share. This means that if you buy AOI shares at C$1.22 or less

you are, in effect, getting 25% of South Lokichar for free. AOI therefore

appears to be very under-valued at its current price of C$1.15/share.

*Aura Minerals (ORA.TO) published its financial statements and

MD&A for the June-2018 quarter. The financial statements showed that ORA had

US$33M of working capital and US$18M of long-term debt at 30th June, meaning

that it had US$15M of net cash. This is down from US$20M at the end of the

preceding quarter and US$21M at the end of last year. Therefore, ORA has

experienced some balance sheet deterioration during the first half of this year,

but its financial position remains healthy.

ORA has an extremely low

market value for a 140K-oz/year gold producer (at Friday's closing price of

C$1.69 it had an enterprise value of only US$41M). Also, note that ORA benefits

from weakness in the Brazilian Real, so the 15% year-to-date loss in this

currency should be giving a boost to ORA's profitability.

Prior to last

Wednesday ORA's major shareholder (Northwestern) had been successfully

supporting the stock price. Whenever the price dropped to the C$2.05-C$2.10

area, Northwestern stepped in and bought whatever was on offer. This was a

fairly inexpensive endeavour, because generally there wasn't much on offer. Last

Wednesday-Thursday, however, the supply of shares suddenly picked up.

Northwestern continued to buy, but its buying was temporarily overwhelmed by the

selling of shareholders who were obviously panicking in reaction to the

sector-wide pummeling. This caused the ORA stock price to collapse from the

low-C$2 area at Tuesday's close to C$1.48 at Thursday's close. On Friday the

price rebounded to C$1.69.

*Premier Gold (PG.TO)

reported the results of deep drilling at its exploration-stage Hasaga gold

project in Ontario, Canada. The best intercept was 23.4m (true width) grading

5.69 g/t gold.

The Hasaga project has an open-pit gold resource of about

1.7M ounces (1.1M "Indicated" plus 0.6M "Inferred") at an average grade of

around 0.8-g/t, but the deep, high-grade results reported over the past year

suggest that this project has the potential to have both an open-pit mine and an

underground mine.

At this time neither we nor the market is assigning

much value to Hasaga, but with additional exploration and engineering it could

become a valuable asset.

*Sprott Resource Holdings

(SRHI.TO) was removed from the TSI List at the beginning of this year,

but we kept the SRHI warrants. The warrants are impacted by a 1-for-20 share

rollback that took effect last Wednesday.

Due to the rollback, the number

of outstanding shares dropped from 682M to 34M and the price per share rose

accordingly. So, the owner of 20,000 shares pre-split owns 1,000 shares

post-split, with the 1,000 new shares having the same value as the 20,000 old

shares.

It's a similar but slightly different story with the warrants.

The owner of 20,000 warrants pre-split still owns 20,000 warrants, but the new

warrant exercise price is 20-times the old exercise price (the exercise price

has increased from C$0.3333 to C$6.66) and 20 warrants now have to be exercised

to purchase one share. The expiry date remains at February-2022, so there is

still a lot of time for something to happen that injects substantial value into

the warrants.

List

of candidates for new buying

From within the ranks of TSI stock

selections the best candidates for new buying at this time, listed in

alphabetical order, are:

1) AAU (last Friday's closing price: US$0.63)

2) KBLT.V (last Friday's closing price: C$6.03)

3) ORA.TO in the

C$1.50s (last Friday's closing price: C$1.69)

4) PG.TO (last Friday's

closing price: C$1.99)

5) SBB.TO (last Friday's closing price: C$1.25)

The above list is limited to five stocks. It will sometimes contain less

than five, but it will never contain more than five regardless of how many

stocks are attractively priced for new buying.

Adding

a trading position in Gold Fields Ltd. (NYSE: GFI). Recent price: US$2.49

GFI is a 2M-oz/yr gold producer with operations in Australia, South Africa,

West Africa and South America.

Last week, GFI's stock price crashed.

From its close at the end of the preceding week to its low point on Friday 17th

August it was down by 33%. It then recovered a little to end the week with a

loss of 29%.

The

sector-wide decline was part of the reason for GFI's crash, but it wasn't the

main reason. The main reason was news that the company's South Deep mine in

South Africa was performing much worse than expected and that the value of this

asset was going to be written down by about US$360M. In response to this news

and the negative sentiment towards gold, GFI's market cap was reduced by about

US$820M last week.

GFI's South African operation accounts for only 10% of

the company's production, but it makes a disproportionately large contribution

to the company's total production cost. During the first half of this year, for

example, the AISC for GFI's South African production was US$1700/oz while the

AISC for the rest of the business was about US$900/oz. It therefore makes sense

for GFI to scale-down the SA operation, which is exactly what is going to

happen.

We think that last week's collapse in the GFI stock price was a

big over-reaction and that the stock is a reasonable speculation near its

current price or lower in anticipation of a rebound. Consequently, a GFI trading

position with an expected duration of four months or less has been added to the

TSI List. The rebound target we have in mind is US$3.50.

Also, as a much

higher-risk/higher-reward speculation we will add the GFI January-2019 $3.00

call option to the TSI List if it trades at US$0.10 within the next two weeks.

It ended last week at $0.12-$0.15. A rebound in the stock price to near the

breakdown level of $3.50 would boost the price of this option to at least $0.50.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/

http://www.goldchartsrus.com/