![]()

![]()

![]()

![]()

-- Weekly Market Update for the Week Commencing 21st October 2019

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

True

Fundamentals Summary

[Notes:

1) The date shown next to the current True Fundamentals Model (TFM) signal is

when the most recent change occurred. 2) Charts of the Gold and Equity

TFMs are included in the "Charts and Indicators" section of the TSI web

site]

| Market | True Fundamentals Model (TFM) |

| Gold (US$ Price) | Bullish (04 Oct 2019) |

| US Equity (SPX) | Bearish (04 Oct 2019) |

| Currency (Dollar Index) | Neutral (15 Mar 2019) |

| Commodities (GNX) | Bearish (01 Jun 2018) |

Last week's posts at the TSI Blog

Monetary Inflation and the Next Crisis

Summary of current

thinking/positioning

1) The Dollar Index (DX)

confirmed a short-term downward trend reversal during the week before

last, but on a longer-term basis it remains in limbo. We expect that the

choppy price action of the past several months will be followed by a

substantial decline, but there remains a (diminishing) risk that the DX

will first move sharply higher for 1-3 months.

2) The US$ gold

price, the US$ silver price and the gold-mining indices are still immersed

in corrections and are at risk of experiencing sharp price declines within

the next couple of weeks, but new upward trends are expected to begin

before the end of November.

3) The SPX could be in the process of

setting an intermediate-term double top, but even if this is the case it

likely will make a marginal new all-time high prior to commencing a

sizable decline. At the same time, the Fed's new asset monetisation

program has increased the risk for bearish speculators and clear signs of

equity strength have started to emerge outside the US.

4) The

T-Bond probably has commenced a decline that will take it below its

September low within the next few weeks, but major price weakness (yield

strength) in the Treasury market could be postponed until next year.

5) We are holding a cash reserve of around 30%.

"Big Picture

View" removed from the Weekly Update

We have removed the "Big Picture

View" that until now was displayed near the top of every Weekly Market

Update. This has been done because the section covered such long

time-frames that it added no practical value. Investing and speculating

decisions should be based on the current risk/reward and potentially could

take into account forecasts of how the financial/economic landscape will

change over the coming year or two. Decisions should not be based on vague

notions of secular trends.

Yield Curve

Reversal

Last week there was a confirmed

reversal in the US yield curve from flattening to steepening. This is

evidenced in part by the recent up-turn in the 30yr-3mth yield spread

illustrated by the following chart. It is the first such signal since

Q4-2016 and differs from the previous signal in that it has come after an

inversion, which means that it is more significant. Whereas the Q4-2016

signal was part of a counter-trend move within a multi-year 'flattening'

trend, it's likely that the current signal is marking the start of a

multi-year steepening trend. What are the implications for the financial

markets and the economy?

The yield curve reversal increases the risk that a US economic

recession will start within the next few months, but it also could be

signaling the onset of a 1-2 year period of higher "inflation". The former

implies an equity bear market and strength in gold relative to industrial

commodities, whereas the latter implies a continuing equity bull market

and strength in industrial commodities relative to gold.

More

information is required to determine whether the yield curve reversal is a

boom-bust transition (recession) warning or an inflation warning, but in

either case the curve should continue to steepen over the months/quarters

ahead if last week's signal is genuine.

If the yield-curve reversal

is signaling higher "inflation" then future steepening will be primarily

the result of rising long-term interest rates. This is sometimes referred

to as a "bearish steepening" because it is driven by falling bond prices.

Alternatively, if the yield-curve reversal is signaling a transition from

boom to bust then future steepening will be primarily the result of

falling short-term interest rates. This is sometimes referred to as a

"bullish steepening" because it is driven by increases in the prices of

debt securities.

Do we think it will be a bearish or a bullish

steepening?

If not for the Fed's actions over the past few weeks we

would favour a bullish steepening, that is, we would assume that the yield

curve reversal was signaling a boom-to-bust transition. However, given the

Fed's recent reintroduction of QE we are leaning in the other direction.

Further to the discussion in the Stock Market section of today's report,

the new QE (or whatever the Fed wants to call it) program is a potential

game-changer.

Commodities

The palladium bubble

continues to inflate

There was a parabolic rise in the

palladium price to a peak in mid-March of 2019 and then a sharp 2-week

decline. In the 1st April Weekly Update we speculated that the decline

from the mid-March peak had marked the start of a multi-month correction,

but not the start of a bubble collapse. We followed up with similar

assessments in the 6th May and 15th July Weekly Updates, concluding in the

15th July commentary: "Palladium is in a bubble, but the bubble is not

yet fully inflated."

The bubble has continued to inflate and

now could be in its final blow-off phase.

The last palladium bubble

reached its ultimate high in early-2001 and the current bubble appears to

be following a similar path. The weekly charts inserted below illustrate

this. The first chart covers 1999-2001 and the second chart begins two

years ago.

If the rough similarity is maintained then today's

market will reach its final top between November of this year and March of

next year.

Consolidation in the copper market

In early

June the copper price was in the mid-$2.60s. It has since traded as high

as $2.80 and as low as $2.48, but has returned to the mid-$2.60s. For all

intents and purposes, therefore, it has gone nowhere over the past 4.5

months.

It's possible that an intermediate-term bottom was put in

place via the spike down to the $2.40s at the beginning of September, but

at this stage there is still a significant risk that a drop to a new

multi-year low will precede the start of an intermediate-term rally.

We think that copper will trade a lot higher within the coming 12

months, but the short-term risk/reward looks neutral.

The Stock Market

A potential game-changer

Once an equity bear market is well underway it runs its course,

regardless of the Fed's actions. For example, the Fed started cutting

interest rates in January of 2001, but the bear market that began in March

of 2000 continued until October-2002. For another example, the Fed started

cutting interest rates in September-2007, but a bear market commenced in

October-2007 and continued until March-2009 despite numerous Fed actions

designed to halt the price decline. On this basis it can be argued that

the Fed's introduction of a

new asset monetisation program roughly one week ago won't prevent the

stock market from rolling over into a major bearish trend. However, there

is a good reason to think that it could be different this time (dangerous

words, we know) and that the Fed's new money-pumping scheme will prove to

be game-changer.

The reason to think that it could be different

this time is that in one respect it definitely is different. We are

referring to the fact that although the Fed started cutting interest rates

in the early parts of the last two cyclical bear markets (2000-2002 and

2007-2009), it didn't begin to directly add new money to the financial

markets until the S&P500 Index had been trending downward with conviction

for about 12 months.

To further explain, when the Fed's targeted

interest rates follow market interest rates downward, which is what tends

to happen during at least the first half of an economic downturn, the

official rate cuts do not add any liquidity to the financial system. It's

only after the Fed begins to pump new money into the financial markets

that its actions have the potential to support asset prices.

During the last two bear markets, by the time the Fed started to pump

money it was too late to avoid a massive price decline. This time around,

however, the Fed has introduced a fairly aggressive money-pumping program

while the S&P500 is very close to its all-time high and seemingly still in

a bullish trend.

The Fed has emphasised that the new asset

monetisation program should not be called "QE" because it does not

constitute a shift in monetary policy. Technically this is correct, but in

a way it's worse than a shift towards easier monetary policy. The Fed's

new program is actually a thinly-disguised attempt to help the Primary

Dealers absorb an increasing supply of US Treasury debt. To put it another

way, the Fed is now monetising assets for the purpose of financing the US

federal government, albeit in a surreptitious manner.

This relates

to a point we made in a

recent

blog post. The point is that when the central bank is perceived to be

financing the government, as opposed to implementing monetary policy to

achieve economic (non-political) objectives such as "price stability",

there is a heightened risk that a large decline in monetary confidence

will be set in motion. One effect of this would be an increase in what

most people think of as "inflation".

Summing up, it's possible

that the Fed's new asset monetisation program will extend the current

cycle (prolong the equity bull market) and lead to more "price inflation"

than earlier programs.

Nearing an upside breakout in the

banking sector

With reference to the upper section of the

following weekly chart, notice that for the third time since July the US

Bank Index (BKX) is threatening to break out to the upside. A weekly close

above 103 would do it. Also, the lower section of the chart shows that the

BKX/SPX ratio is close to breaking the sequence of declining tops that

began early last year. It would do so by ending a week above its July

high.

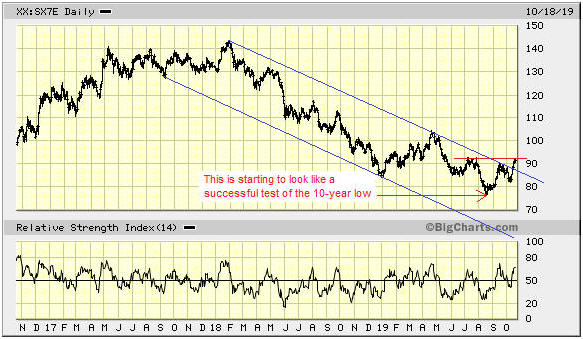

It isn't only the US banking sector that is showing signs of strength.

The following daily chart reveals that the Europe STOXX Banks Index (SX7E)

has been working its way upward since testing its 10-year low two months

ago. A weekly close above the April high would be a definitive reversal

signal.

Bank stocks in both the US and Europe have intriguing

intermediate-term upside potential. This is linked to the potential for

meaningful gains in interest rates and a substantial steepening of the

yield curve over the coming year.

Current Market Situation

The S&P500 Index (SPX) has spent the past 2.5 months making lower

highs and higher lows. In the process it has formed the contracting

triangle drawn on the following daily chart.

It tested the top of

its contracting range last week and then pulled back a little. This week

it could trade as low as 2890 without altering the short-term pattern.

Given that the NYSE Advance-Decline Line (ADL) made a new all-time

high last week, it's likely that over the next few weeks the SPX will do

no worse than test the bottom of its contracting range and at some point

move into new-high territory.

Interestingly, signs of equity-market strength are becoming apparent

outside the US. For example, the following daily chart shows that the EURO

STOXX 50 ETF (FEZ) made a new high for the year last week and that

European stocks have begun to out-perform US stocks (the FEZ/SPY ratio has

been rising since August and moved sharply higher over the past

fortnight).

For a second example, it looks like the Emerging Markets Equity ETF

(EEM) is about to break upward from the channel in which it has traded

since April.

Taken together, the new highs in the NYSE ADL and the recent signs of

strength in bank stocks, European stocks and Emerging-Market stocks point

to additional gains in equity prices in the short-term.

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date | Description |

| Monday Oct-21 | No important events scheduled |

| Tuesday Oct-22 | Existing Home Sales |

| Wednesday Oct-23 | No important events scheduled |

| Thursday Oct-24 |

Durable Goods Orders New Home Sales |

| Friday Oct-25 | Consumer Sentiment Index |

Gold and the Dollar