![]()

![]()

![]()

![]()

-- Weekly Market Update for the Week Commencing 22nd January 2018

Big Picture

View

Here is a summary of our big picture

view of the markets. Note that our short-term views may differ from our

big picture view.

The BULL market in US Treasury Bonds that began in the early 1980s ended in mid-2016, but there will be many years of topping action in bond prices and bottoming action in bond yields before major new trends get underway. A major decline in government bond prices will unfold during the 2020s. (Last update: 11 September 2017)

The stock market, as represented by the S&P500 Index, commenced a secular BEAR market during the first quarter of 2000, where "secular bear market" is defined as a long-term downward trend in valuations (P/E ratios, etc.), gold-denominated prices and inflation-adjusted prices. This secular trend will bottom in 2020 or later. (Last update: 11 September 2017)

A cyclical BEAR market in the US Dollar began in 2016-2017. (Last update: 11 September 2017)

Gold commenced a secular bull market relative to all fiat currencies, the CRB Index, bonds and most stock market indices during 1999-2001. This secular trend will peak in 2020 or later. (Last update: 11 September 2017)

Commodities,

as represented by the CRB Index, commenced a

secular BULL market in 2001 in nominal dollar terms. The first major

upward leg in this bull market ended during the first half of 2008, but

a long-term peak won't occur until 2020 or later.

(Last

update: 11 September 2017)

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

True

Fundamentals Summary

[Notes:

1) The date shown next to the current True Fundamentals Model (TFM) signal is

when the most recent change occurred. 2) Charts of the Gold and Equity

TFMs are included in the "Charts and Indicators" section of the TSI web

site]

| Market | True Fundamentals Model (TFM) |

| Gold (US$ Price) | Bearish (12 Jan 2018) |

| US Equity (SPX) | Neutral (12 Jan 2018) |

| Currency (Dollar Index) | Bullish (15 Dec 2017) |

| Commodities (GNX) | Bullish (29 Dec 2017) |

Last week's posts at the TSI Blog

Oil, the Yuan and the dollar-based monetary system

Summary of current

thinking/positioning

1) Expecting that gold will soon

make a short-term price top.

2) On the lookout for signs of trouble

in a very 'overbought' and over-valued US stock market, but at this time

not seeing any reason to expect something more bearish than a normal

short-term correction.

3) Thinking that industrial commodities such

as oil and copper will make short-term price highs during the first two

months of 2018.

4) Thinking that the Dollar Index (DX) has resumed

its longer-term downward trend, but that a counter-trend rebound will

begin within the next three weeks.

5) Thinking that the T-Bond has

almost completed an intermediate-term topping pattern within the context

of a long-term topping pattern.

6) Holding a cash reserve of about

25% and looking for opportunities to boost this reserve to 30%-35%.

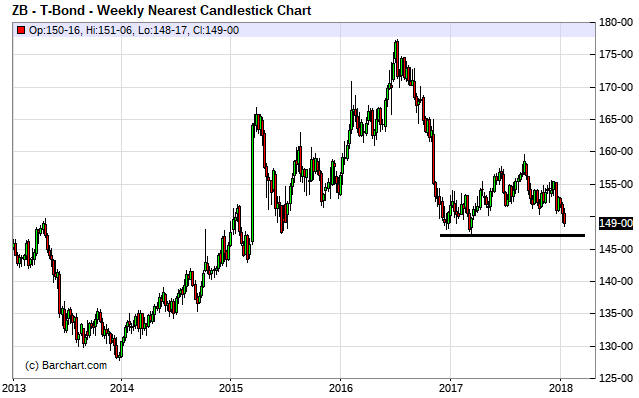

The Treasury

market is getting interesting

The T-Bond price ended last week

only 2 points above long-term support defined by its March-2017 low. A

weekly close below this support (147 for the nearest futures contract)

would, we think, sound the death knell for the secular bond bull market.

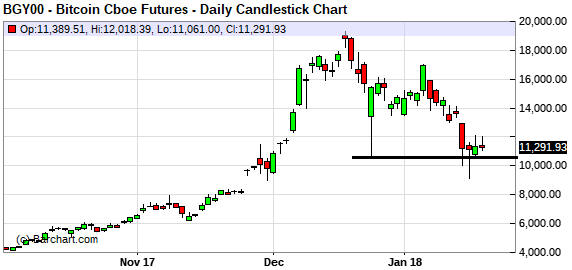

Cryptomania

Update

Still awaiting

confirmation of a major top

Our most recent "Cryptomania

Update" was in the 27th December Interim Update. Here's how we summed up

the Bitcoin situation at that time:

"Despite the ample evidence

that the enthusiasm for bitcoin and the associated "alt-coins" was an

extraordinary popular delusion and that the past few weeks was a major

speculative finale, there is still a realistic chance that last week's

price crash was a bull market correction. As mentioned above, confirmation

of a major top requires a price crash (done), a rebound to a lower high

(possibly in progress) and then a decline to below the crash low."

Amazingly given the size of the price plunge over the course of last

Tuesday-Wednesday, we still don't have confirmation of a major Bitcoin

price top. The reason is that although Bitcoin traded at a new post-crash

low on 17th January it is yet to CLOSE below its 22nd December low.

Therefore, what we have at the moment is a potential double-bottom, with

the 16-17 January price plunge constituting a successful test of the 22nd

December low. Refer to the following chart for details.

There's a

good chance that within the next few weeks the Bitcoin price will close

below its 22nd December low, removing most of the remaining doubt that the

price top on 18th December (the day that futures trading commenced on the

CME and a week after futures trading commenced on the CBOE) was the

ultimate top. It just hasn't happened yet.

The market-cap giveaway

There has been a lot

of talk over the past two years about the market caps of Bitcoin, the

"alt-coins" and the entire cryptocurrency universe. Even the most

outspoken advocates of the idea that private cryptocurrencies are the

future of money regularly refer to the market caps of these so-called

currencies. However, nobody ever refers to the market cap of an actual

money or commonly-used medium of exchange. For example, there is never any

mention of the euro's market cap or the Yen's market cap or gold's market

cap. This is something of a giveaway.

The market cap concept

doesn't apply to money; it applies to stocks. Therefore, when someone

refers to the market cap of Bitcoin they are -- unwittingly in most cases

-- treating Bitcoin as if it were a stock. This is appropriate, because

although a small fraction of its demand is associated with use as a medium

of exchange and although it is an important part of the first successful

attempt at creating a reliable distributed ledger, Bitcoin has always

traded more like a speculative stock than a type of money.

Bitcoin's effect on gold and gold stocks

We doubt that

2017's manic trading of Bitcoin and the other 'cryptocurrencies' siphoned

enough investment demand away from gold to make a noticeable difference to

the gold price. It is of course true that some of the people who are

interested in Bitcoin are also interested in gold, but cryptocurrency

traders would not, as a group, account for enough bullion demand to move

the gold market's dial.

It could be argued that while the bullion

market was not affected by 'cryptomania', the lacklustre performance of

the gold-mining sector in 2017 indicates that gold stocks were. However,

other stock-market-related bubbles and investment booms, such as the

marijuana stock bubble, could have drawn speculative interest away from

the gold-mining sector.

In any case, the hard reality is that while

the broad stock market is making substantial real progress there usually

will not be much enthusiasm for gold-related investments. Consequently, it

is not surprising that after the 2015-2016 weakness in the stock market

became widely perceived as nothing more than an intermediate-term

bull-market correction, the collective attention of equity speculators

drifted away from the gold-mining sector.

Gold and gold-mining

stocks can rally during a strong upward trend in the broad stock market,

which is exactly what they have done over the past few weeks. It's just

that if the equity bull market remains intact then most of the gains made

by gold-related investments will prove to be unsustainable.

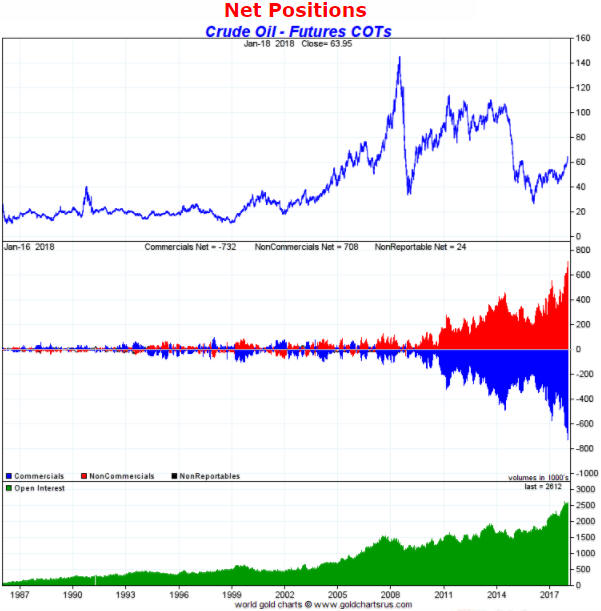

Commodities

Speculators get even

more enthusiastic about oil

Another week, another new

all-time high for the total speculative net-long position in Nymex crude

oil futures. The following chart tells the story. Speculators in oil

futures are more bullish about the oil price than they have ever been.

The aggressive betting on future gains in the oil price creates

downside risk, but the magnitude of the risk is mitigated by the

supply-demand situation in the physical market remaining price-supportive.

Due to the supportive fundamentals we continue to expect that the oil

price will make a new high for the year during the second quarter --

following a 1-2 month correction from a January-February (most likely

January) high.

Copper consolidation

Thanks

to the downward drift of the past three weeks the copper market is no

longer short-term 'overbought'.

This downward drift could turn into

a 2-3 month correction that takes the price down to around $3.00.

Alternatively, there could be a surge to a marginal new multi-year high

within the coming few weeks prior to the start of a more significant

correction. Either way, we expect the copper price to stay within 10% of

its current price over the next two months.

The Stock Market

The US stock market continued

its ascent last week. The relentlessness of the recent advance is clearly

evident on the following daily chart of the NASDAQ100 Index (NDX).

For important indices such as the SPX and the Dow, short-term momentum

indicators have reached multi-decade extremes. Paradoxically, this means

that there probably won't be anything more bearish than a 5%-10%

correction within the next three months, especially given that market

internals have confirmed the rally.

The bond market is the only

plausible threat to the above assessment of the stock market's short-term

prospects. We suspect that a break by the T-Bond to below last year's low

of 147 would stop the stock market rally and that downward acceleration by

the T-Bond after breaching 147 would lead to a large (15%-25%) decline in

the SPX.

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date | Description |

| Monday Jan-22 | No important events scheduled |

| Tuesday Jan-23 | No important events scheduled |

| Wednesday Jan-24 | Existing Home Sales |

| Thursday Jan-25 | New Home Sales |

| Friday Jan-26 |

Durable Goods Orders Q4 GDP (prelim) |

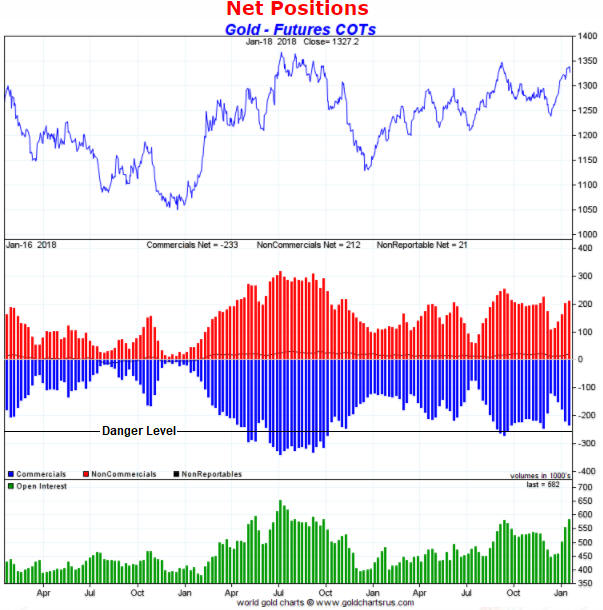

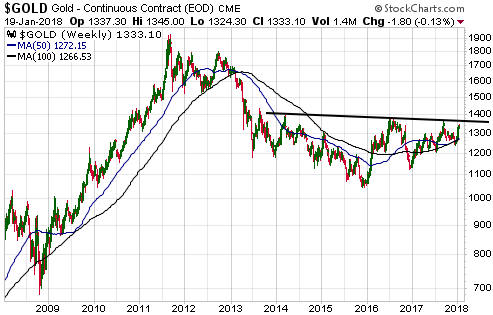

Gold and the Dollar

Turning to the price action, silver and the gold-mining indices

diverged bearishly from gold last week. This warns that a short-term price

top might have occurred a little sooner than expected. However, as

previously advised it will be reasonable to assume that the short-term

upward trend is intact while the gold price remains above its 20-day MA on

a daily closing basis. As illustrated by the following daily chart, this

MA has moved up to $1311 and is still rising.

The weekly chart (see below) indicates that important resistance

begins at around $1360. It's likely that a weekly close above this

resistance and the 2016 high of $1377 would prompt significant

follow-through to the upside as speculators piled into long positions.

This important longer-term resistance at $1360-$1377 probably won't be

breached during the first quarter of 2018 but it probably will be breached

during the second quarter. If/when it happens the breach of this

resistance undoubtedly will spur very aggressive bullish predictions that

won't come close to being fulfilled.

Platinum

Breaks below obvious and important

support levels that are quickly reversed are reliable bullish signals. A

recent example is the short-lived break by the US$ platinum price below

intermediate-term lateral support during the first half of December. The

false downside breakout was followed by a fast rebound that is still in

progress.

In the 8th January Weekly Update we wrote that the platinum market had

done enough to confirm that an intermediate-term bottom was put in place

in December, but that the rally was a little stretched on a short-term

basis. A week later we wrote:

"Platinum has channel resistance

and 'round number' resistance at $1000. Above that there is important

lateral resistance at $1025-$1050. It is currently short-term 'overbought'

and testing the lower of the aforementioned resistance areas. We expect a

multi-week price peak at around this level or following a near-term spike

to $1025-$1050."

A near-term spike to $1025-$1050 is almost

complete.

We will be surprised if the platinum price manages to

break above $1050 before experiencing a multi-week correction. Note that a

routine correction would retrace about half of the rally from the December

low, implying that the mid-$900s would be a realistic target for the next

tradable low if a correction were to begin near the current price.

Gold Stocks

A weekly chart of the HUI is displayed

below.

The HUI's rally from its December low has been unimpressive

to date. It is yet to achieve a weekly close above the 80-week MA and has

not come close to testing important lateral resistance at 220. The rally

also hasn't done anything yet to differentiate itself from the multi-week

rebounds that occurred during 2017.

Although this is not what we expect, the lack of meaningful upward

momentum in the gold-mining sector since the December-2017 low creates the

risk that the next multi-week correction in the bullion market will take

the HUI to a new 12-month low. This risk would be eliminated by a weekly

close above 220 and greatly diminished by even a test of 220.

Depending on personal money-management considerations such as the extent

of existing exposure, some selling of gold-mining stocks could be

appropriate in the near-term. That will especially be so if a rise in the

gold price to around $1360 fails to generate much additional enthusiasm

for gold mining stocks.

We can't single out any TSI gold stocks for

selling because none of them are close to being fully valued and in most

cases they are also not close to being short-term 'overbought'. We are

simply making the general suggestion that a reduction in exposure to the

gold sector could make sense for investors who presently have substantial

exposure.

The Currency Market

2018 forecast for the currency market

The expectations we had for the currency market at the start of last

year turned out to be wide of the mark. We expected the Dollar Index (DX)

to begin the year will a decline lasting up to three months and to then

rise to a major high during either the second or the third quarter. The

year kicked off as envisaged, but rather than being a downward correction

within a bull market the Q1-2017 decline proved to be the first leg of a

bear market.

This year has started with speculators extremely

bearish on the US$ relative to the euro (the DX is dominated by the

US$/euro exchange rate). It has also started with a downside breakout in

the DX (a break below the September-2017 low). The fact that the breakout

wasn't quickly negated suggests that it was genuine and will be followed

by additional weakness in the DX over the months ahead, despite the

sentiment situation. The sentiment extreme in the currency market, like

the sentiment extreme in the US stock market, warns of a significant

first-quarter correction but not a major reversal.

According to our

currency fundamentals model the fundamental backdrop is finely balanced at

the moment. Our model is currently DX-bullish, but both the interest-rate

and the relative-equity-strength inputs are very close to their

moving-average demarcation levels. This means that a small change could

flip the model to US$-bearish.

Despite the continuation of the

Fed's rate-hiking campaign in H1-2018 and the ECB still being at least a

year away from making its first rate hike, interest-rate differentials at

the long end could move in the euro's favour during the first half of 2018

just as they did during the first half of last year. This is mainly

because European bond yields are starting at much lower levels than the

equivalent US bond yields. For example, the US 10-year T-Note yield ended

last week at 2.64% whereas Germany's 10-year government bond ended the

week with a yield of only 0.57%.

In summary, we expect the DX's

downward trend to persist through the bulk of this year's first half. If

this happens then the anti-US$ sentiment will be even more extreme,

setting the stage for the DX to become very strong during the year's

second half.

Taking a broader view of the currency market, our

expectation that commodity prices will trend upward during H1-2018

combined with the A$'s bullish COT situation leads to a forecast that the

A$ and the C$ will be the strongest major currencies during the first half

of this year. Due to its bullish COT situation the Swiss Franc is also

poised to be relatively strong during the first half of this year.

During the second half of the year, substantial declines in the commodity

and equity markets will, we think, lead to the A$ and the C$ being among

the weakest major currencies and the Yen being the strongest.

Current Market Situation

Last

week there was a small additional rise in the euro and a small additional

decline in the Dollar Index (DX). It was an uneventful week and did not

provide any evidence that the DX's short-term downward trend has ended.

Consequently, the price action suggests that the DX will drop to a new

multi-year low within the next two weeks, with or without a few more days

of consolidation in the 90-91 range.

At the same time, speculative sentiment remains stretched in the

anti-US$/pro-euro direction by a sufficient amount to fuel a multi-week

rebound in the DX and pullbacks in most other currencies. The sentiment

extreme is evidenced by the COT numbers, which show that speculators in

currency futures have by far their largest-ever net and gross long

positions in the euro.

We expect that even if the DX extends its

recent sharp decline over the coming 2-3 weeks it will trade at 92 before

the end of Q1.

Updates

on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() Company

news/developments for the week ending Friday 19th January 2018:

Company

news/developments for the week ending Friday 19th January 2018:

[Note: AISC = All-In Sustaining Cost, FS = Feasibility Study, FY =

Financial Year, IRR = Internal Rate of Return, ISR = In-Situ Recovery,

MD&A = Management Discussion and Analysis, M&I = Measured and Indicated,

NAV = Net Asset Value, NPV(X%) = Net Present Value using a discount rate

of X%, P&P = Proven and Probable, PEA = Preliminary Economic Assessment,

PFS = Pre-Feasibility Study]

*Alkane Resources

(ALK.AX) advised that it has produced high-purity hafnium dioxide

products at its demonstration pilot plant using a proprietary process to

separate hafnium from zirconium. This is important because a) there may be

a global shortage of hafnium over the next few years, b) ALK's

construction-ready Dubbo Project (DP) is slated to produce 25 tpa of

hafnium, and c) although hafnium is expected to be a relatively minor part

of the DP's overall output, at the current hafnium price the

aforementioned production would result in annual revenue of about US$40M

for ALK.

The next major market-moving news from ALK is expected to

be the results of the modular construction study for the DP project. This

was scheduled to be complete before the end of 2017 but has been delayed

to Q1-2018.

*Blackham Resources (BLK.AX)

has provided the long-awaited details of its new recapitalisation plan,

the earlier plan having failed due to the withdrawal of Pacific Road

Capital (PRC). Although the new plan results in even greater per-share

value destruction, in one way it is better than the previous plan. This is

because the new plan enables shareholders who are eligible to participate

in the equity portion of the refinancing arrangement to largely avoid

having their stakes diluted, whereas the previous plan did not (the

previous plan involved PRC being issued a massive quantity of low-priced

options).

Here are the new plan's salient details:

-

Replacement of the A$14.3M Orion term loan that was due to be repaid this

month by a loan from MACA (BLK's primary mining contractor) under which

the first repayment isn't due until March-2019.

- An

underwritten A$36M Entitlement Issue (EI) with Hartleys Ltd. acting as the

lead underwriter.

- The EI will give eligible shareholders

the right to buy 5 new shares at A$0.04 for every 2 shares held at 24th

January (the day before the shares trade 'ex' the EI rights). Also, 1 free

January-2019 option with an exercise price of A$0.08 will be issued with

every 2 new shares. For example, an eligible shareholder with 20,000

existing shares would have the right to buy 50,000 new shares at 0.04

each, and if this right was taken up in full the shareholder would also

receive 25,000 January-2019 A$0.08 options.

- When small

Australian companies do these entitlement issues it is normal that only

shareholders with registered addresses in Australia or New Zealand are

eligible to participate. If that's the case here (BLK hasn't yet specified

if it is) then shareholders with addresses outside Australia-NZ would not

receive the EI rights associated with their shares. Instead, an attempt

would be made by an appointed broker to sell these rights on the ASX. The

proceeds of any sale would then be credited to the brokerage account of

the non-eligible shareholder.

- Eligible shareholders who do

not wish to exercise their rights would also have the opportunity to sell

their rights on the market. It is expected that the rights will trade on

the ASX from 30th January until 5th February.

- If the EI is

successfully completed then for TSI record purposes it will be assumed

that the EI rights were exercised. The BLK January-2019 option will be

added to the TSI List.

- The options are expected to trade

on the ASX and, depending on price, could be a worthwhile speculation. We

will discuss the merits of these options in a TSI commentary closer to the

time at which they start to trade (mid-February or later).

-

Upon completion of the EI, BLK will have net debt of about A$21M and a

share count of 1257M.

BLK reports that it is currently producing

gold at the rate of about 85K-oz/year at an AISC of A$1100-$1200/oz

(US$870-$950/oz). This constitutes a big improvement over last year's

performance, but the per-share value has collapsed -- thanks to the

massive addition of new 4c shares -- even assuming that this improved

production rate will be sustained.

Making the assumption that the

new recapitalisation plan is completed, we estimate that a BLK share has a

fair valuation range of A$0.07-A$0.11. If the company achieves its

guidance and there is no change in the A$-denominated gold price, then in

a year from now the fair value will rise to A$0.13 due to the repayment of

debt. Note that these figures don't allow anything for the project's

expansion potential.

*Golden Arrow Resources (GRG.V)

has a 25% stake in Puna Operations, the company that owns the

Pirquitas-Chinchillas silver-lead-zinc project in Argentina. During the

first half of this year the project's production will result solely from

the processing of stockpiled ore at Pirquitas, but the first ore from

Chinchillas should become available for processing during the second half.

Total silver production is expected to be 3.0M-4.4M ounces in 2018 and

increase to around 8M ounces in 2019 (GRG's share is 25% of these

figures).

Development of the Chinchillas mine is estimated to

require an additional US$70M of capital expenditure, which means that GRG

will have to pony up about US$17.5M (C$22M). This, we think, will

necessitate an equity financing of around C$10M at some point over the

next 6 months.

*Premier Gold (PG.TO)

reported that its 2017 gold production was 139.7K ounces. This is at the

top end of the company's upwardly-revised guidance range and is therefore

a good result.

As expected, 2018 production is going to be much

lower due to the completion of mining at the Phase 2 open pit at the South

Arturo project (Nevada). 2018 guidance is for gold production of 85K-95K

ounces at an AISC of US$800-$850/oz, with almost all of the production

coming from the Mercedes mine in Mexico.

At South Arturo, stripping

of the Phase 1 pit will commence around mid-year and development of the El

Nino underground mine is scheduled to begin in the third quarter. These

developments should ensure that South Arturo returns to being a

significant contributor to PG's total production during 2019-2020.

PG is a relatively low-risk junior gold producer with substantial in-built

growth potential.

*US Gold (USAU) made a

strange financing announcement last Thursday that was immediately followed

by a large decline in the stock price. The company announced that it was

selling $5M of shares of its Series E convertible preferred stock in a

non-brokered registered direct offering, but didn't state the price at

which the preferred shares could be converted into common shares. It also

announced the sale of warrants to purchase an aggregate of 1.25M shares of

common stock at an exercise price of $3.30 per share with a three-year

term, but didn't clarify how or if the warrants were related to the

preferred shares. As a result, USAU's management won the prize for the

most confusing financing announcement of the past 12 months.

The

details of the financing became clear the next day when a

Prospectus Supplement was filed with the SEC. This document specifies

that the conversion price is US$2.00 and that the warrants are being

issued to the buyers of the preferred shares.

In effect, USAU is

issuing 2.5M units at US$2.00 with each unit comprising one share and half

a $3.30 warrant.

The stock market's dramatic negative reaction to

the financing news on Thursday was due to the company effectively issuing

new shares at $2.00 at a time when the market price of the shares was

$3.10. We suspect that the unusually-large discount was caused by the

financing deal having been agreed 2-3 weeks ago when the market price was

well below $2 (because they rank ahead of common shares, preferred shares

will often be issued at a premium to the market). In other words, it's

likely that a large discount emerged due to the stock price approximately

doubling in the short period between the terms of the financing being

agreed and the announcement being made.

![]() List

of candidates for new buying

List

of candidates for new buying

From within the ranks of TSI

stock selections the best candidates for new buying at this time, listed

in alphabetical order, are:

1) ALK.AX (last Friday's closing price:

A$0.34)

2) EGD.V (last Friday's closing price: C$0.34)

3)

ESM.TO (last Friday's closing price: C$1.28)

4) NSU (last Friday's

closing price: US$2.36)

5) PRQ.TO (last Friday's closing price:

C$1.52)

The above list is limited to five stocks. It will sometimes

contain less than five, but it will never contain more than five

regardless of how many stocks are attractively priced for new buying.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://www.goldchartsrus.com/

http://www.barchart.com/