-- Weekly Market Update for the Week Commencing 22nd February 2016

Big Picture

View

Here is a summary of our big picture

view of the markets. Note that our short-term views may differ from our

big picture view.

The BULL market in US Treasury Bonds

that began in the early 1980s ended in early-2015, but there will be many years

of topping action in bond prices and bottoming action in bond yields before

major new trends get underway. (Last update: 29 June 2015)

The stock market, as represented by the S&P500 Index,

commenced

a secular BEAR market during the first quarter of 2000, where "secular

bear market" is defined as a long-term downward trend in valuations

(P/E ratios, etc.) and gold-denominated prices. This secular trend will bottom sometime between 2018 and 2020.

(Last update: 29 June 2015)

A secular BEAR market in the

US

Dollar

began during the final quarter of 2000 and ended in July of 2008. This

secular bear market will be followed by a multi-year period of range

trading.

(Last

update: 09 February 2009)

Gold commenced a

secular bull market relative to all fiat currencies, the CRB Index,

bonds and most stock market indices during 1999-2001.

This secular trend will peak sometime between 2018 and 2020.

(Last update: 29 June 2015)

Commodities,

as represented by the CRB Index, commenced a

secular BULL market in 2001 in nominal dollar terms. The first major

upward leg in this bull market ended during the first half of 2008, but

a long-term peak won't occur until 2018-2020.

(Last

update: 29 June 2015)

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Outlook Summary

Market

|

Short-Term

(1-3 month)

|

Intermediate-Term

(6-18 month)

|

Long-Term

(2-5 Year)

|

|

Gold

|

N/A |

Bullish

(26-Mar-12) |

Bullish

|

|

US$ (Dollar Index)

|

N/A |

Neutral

(22-Jun-15) |

Neutral

(19-Sep-07) |

|

US Treasury Bonds (TLT)

|

N/A |

Bearish

(19-Oct-15)

|

Bearish |

|

Stock Market

(DJW)

|

N/A |

Bearish

(30-Dec-15) |

Bearish

|

|

Gold Stocks

(HUI)

|

N/A |

Bullish

(23-Jun-10) |

Bullish

|

|

Oil |

N/A |

Neutral

(26-Oct-15) |

Bullish

|

|

Industrial Metals

(GYX)

|

N/A |

Neutral

(09-Nov-15) |

Bullish

(28-Apr-14) |

Notes:

1. Our short-term expectations are discussed in the commentaries, but except in

special circumstances we won't attempt to assign a "bullish", "bearish" or

"neutral" label to these expectations.

2. The date shown below the current outlook is when the most recent outlook change occurred.

3. "Neutral" means that we think risk and reward are roughly in balance with respect to the timeframe in question.

4. Long-term views are determined almost completely by fundamentals and intermediate-term views

are determined by a combination of fundamentals, sentiment and technicals.

Last week's posts at the TSI Blog

There is nothing inherently wrong with market manipulation

Changes in gold location say nothing about the gold price

Can a US recession occur without an inverted yield curve?

Long-term price targets

are meaningless

Bullish pundits routinely tout

very high long-term price forecasts. Although less common, there are also

bearish pundits who regularly tout very low long-term price forecasts.

Furthermore, the touting of extremely high or extremely low price targets seems

to be more common with gold and silver than with any other market. For example,

even during the precious-metals depression of the past year it wasn't difficult

to find predictions that the gold price will reach $5000/oz or more within the

next few years. Such predictions are always meaningless, although they are a

tried and true method of generating subscription revenue.

There are always a myriad of factors affecting price. Since it is impossible to

not only take all of these factors into account but also to predict how each

factor will change in the future, nobody has a clue what the gold price or the

price of anything else will be in a few years' time. Of course, the long-term

price predictions of some people will end up being correct for the same reason

that completely random predictions will sometimes be correct.

One of the unpredictable factors is the changing value of the money in which

prices are expressed. What use, for example, is a forecast that gold is going to

US$5000/oz in a certain number of years unless there is a way of knowing what

the purchasing power of a dollar will be at that future time. To explain what we

mean we point out that a rise in the nominal gold price to $5000/oz by some

future time will represent a DECLINE in the real worth of gold if the price of a

loaf of bread rises to $30 over the same period.

So, whenever you see/hear a prediction that the gold price is going to be 'X'

thousand dollars an ounce within 'Y' years, just laugh and move on.

The Fed is now expected

to do nothing

A report put out by the Fed a

couple of months ago predicted that there would be four 0.25% hikes in the Fed

Funds Rate (FFR) in 2016, but traders operating in the interest-rate futures

market never bought into that forecast. According to the price of the

December-2016 Fed Funds Futures (FFF) contract, at the point of maximum

interest-rate bullishness late last year 'the market' was expecting 2-3 Fed rate

hikes in 2016. In other words, two months ago there was a significant gap

between what the Fed was expecting to do and what 'the market' was expecting the

Fed to do. The gap is now much wider.

The Fed has not yet officially backed away from its 'four rate hikes' forecast,

but according to the current price of the December-2016 FFF contract (see chart

below) 'the market' now expects the number of 2016 rate hikes to be zero or one,

with the odds slightly favouring the former. In other words, traders operating

in the interest-rate-futures market are now collectively of the opinion that

there will be NO Fed rate hikes this year.

This is a remarkable change in interest-rate expectations, and all it took to

bring about the change was an 8% drop in the stock market and a decision by the

Bank of Japan to set a negative interest rate on a small portion of the reserves

held by Japanese banks.

It doesn't take much imagination to figure out what will happen to the Fed's

interest-rate plans and market expectations regarding the Fed's likely actions

if the S&P500 Index breaks solidly below its January low and the economic data

start pointing more definitively towards recession. It doesn't take much

imagination because to become a central banker you must believe that the key to

a stronger economy is more borrowing and spending. What will happen is that

negative interest rate policy (NIRP) will be 'on the table' in the US, although

we doubt that it will ever actually be implemented.

The world's most powerful central bankers have dug themselves into a giant hole

and they strongly believe -- because this is what their models and Keynesian

theories tell them -- that the solution is to keep digging.

The Stock Market

The US

The S&P500 Index (SPX) pulled back a little over the final two days of last

week. This didn't change anything.

There is short-term lateral resistance at 1950 that in a couple of days will

coincide with the falling 50-day MA. It's a good bet that this resistance will

soon be tested. More important resistance lies at 1990-2000. What's the

probability of this higher resistance being tested prior to the resumption of

the longer-term bearish trend?

We don't know the probability, but clues regarding the possible extent of a

continuing SPX rebound from the February low can be found in the two measures of

sentiment discussed below.

The following chart shows the S&P100 Index (OEX), the 10-day MA of the equity

put/call ratio and the 10-day MA of the OEX put/call ratio. The equity put/call

ratio indicates the public's (the dumb money's) concern about downside risk and

the OEX put/call ratio indicates the professionals' (the smart money's) concern

about downside risk, with a high put/call ratio implying high concern and a low

put/call ratio implying low concern.

The chart tells us that during November-December the smart money was worried

about downside risk while the dumb money was complacent. AFTER the market

tanked, the dumb money became very worried about downside risk and the smart

money became less concerned than usual.

At the end of last week the dumb money was still very worried and the smart

money was relatively unconcerned. The put/call situation therefore points to

higher prices over the weeks ahead.

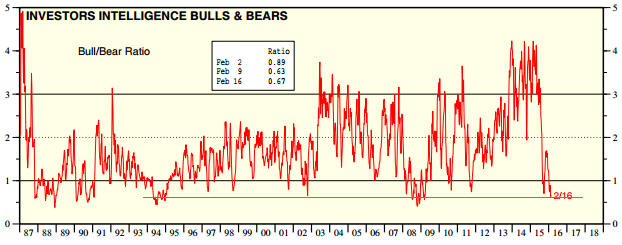

The other measure of sentiment we'll deal with is the weekly Investors

Intelligence survey.

The following chart from Yardeni.com shows that the Investors Intelligence

Bull/Bear ratio recently reached an unusually low level. In fact, during the

week before last the Bull/Bear ratio reached a level that over the past 20 years

was only exceeded near the crescendo of the 2008 crash.

The sentiment situation suggests that we should be open to the possibility of a

meaningful rally over the coming 2 months. For instance, although we don't

expect the rally to go this far it is not inconceivable that the SPX will move

all the way back to the vicinity of its December high before the next short-term

downward trend gets underway.

The sentiment situation also suggests that there is very little chance of the

SPX dropping well below its January-February double bottom within the next few

weeks. The double bottom could be briefly undercut, but it would probably

require bearish sentiment to break all records for the market to drop more than

a few percent below this level in the near future.

The one thing that could possibly cause bearish sentiment to break all records

and lead to a sharp decline to well below the January-February double bottom is

a dramatic escalation in the war raging in and around Syria. In particular, if

Turkey and Saudi Arabia invade Syria then those two countries will find

themselves at war with Russia and all bets will be off.

For safety reasons (to partially hedge the long exposure to non-gold commodity

stocks that we've begun to build) we purchased about 25% of what we would

consider to be a full position in EEM put options shortly after the start of

trading last Thursday, but we probably won't add to this position anytime soon.

For now, it makes sense to give the benefit of the doubt to the bullish side.

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date |

Description |

| Monday

Feb 22 |

No important events

scheduled |

| Tuesday

Feb 23 |

Existing Home Sales

Case-Shiller Home Price Index

Consumer Confidence |

| Wednesday

Feb 24 |

New Home Sales |

| Thursday

Feb 25 |

Durable Goods Orders |

| Friday

Feb 26 |

Q4 GDP (revised)

Personal Income and Spending

Consumer Sentiment |

Gold and the Dollar

Gold

The gold price plunged to the low-$1190s last Tuesday and then rebounded. The

price pattern didn't change over the final two days of last week, so the

following comment from the 17th February Interim Update remains applicable:

"There is currently no way of telling whether this sharp decline [to around

$1190] was a routine pullback to 'test' the preceding upside breakout prior to

the resumption of the rally or the start of a correction that will run for at

least a few weeks. A daily close below $1190 would point to the latter."

According to the latest data, gold's Commitments of Traders (COT) situation

remains neutral (it was bullish until two weeks ago and has since been neutral).

What we mean is that the speculative net-long position has risen to the point

where the COT situation is no longer a tail-wind for the US$ gold price, but it

hasn't yet risen far enough to become a head-wind.

Although it is not something we would bet on, with support at $1190 having

passed its first test and with the COT situation not yet bearish a quick move to

a new high for the year is a realistic possibility. Round-number resistance at

$1300 and the January-2015 peak at $1308 will be obvious near-term targets if

the February high of $1264 is breached.

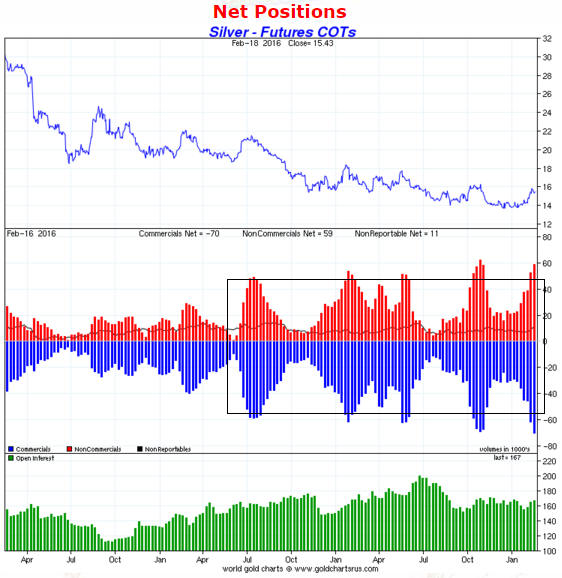

Silver

The optimism about silver's price prospects is nothing if not stubborn and the

breathlessly-bullish commentary on the silver market is nothing if not

persistent.

Every year, without fail, stories get circulated about a looming global silver

shortage. These stories seem to start when someone walks into a coin shop in a

town somewhere (usually in the US) and discovers that the shop is temporarily

out of silver coins. This information is then passed onto someone else who

writes an article claiming that the world is running short of silver, which

leads to widespread speculation that a silver-price moon-shot is about to

happen. The problem is that if the speculation is not supported by the

underlying supply-demand situation for physical silver, a situation that

absolutely cannot be understood by visiting coin shops, it will not lead to a

sustained price advance.

Over the past three weeks the bullish speculation about silver's prospects has

ramped up, as it almost always does whenever the gold price rallies, but as has

consistently been the case over the past couple of years the speculation has not

been supported by the underlying supply-demand situation for physical silver. We

know that this is the case because the increase in the speculative net-long

position in silver futures was large in comparison with the increase in price.

To put it another way, it took a disproportionately large increase in

speculative buying in the futures market to lift the price.

As illustrated by the red and blue bars moving beyond the edges of the box drawn

on the following chart, silver's short-term COT situation is now clearly

bearish. This should be viewed as a red flag, but it doesn't guarantee

significant price weakness in the near future. It's possible, for example, that

a rise to a new high for the year in the gold price will prompt an additional

surge in silver-related speculation.

Chart source: www.sharelynx.com

In silver's favour is the evidence that gold has commenced a bull market and the

fact that the silver/gold ratio is very low by historical standards. The

silver/gold ratio will probably extend its multi-year downward trend over the

months ahead, but it probably won't get a lot lower.

Platinum

Apart from gold, which always warrants special treatment, platinum was the only

commodity we singled out for discussion in our 2016 Yearly Forecast. Here's how

we concluded the discussion: "We expect platinum to make a major bottom in US$

terms, inflation-adjusted terms and gold terms during the first quarter of

2016."

The first evidence that a major bottom is in place for platinum came a couple of

weeks ago when the price broke above the top of a well-defined 18-month channel.

More evidence of a major bottom will be in place if the platinum price holds at

or above $900 during a correction and then moves decisively above its 200-day

MA.

Gold Stocks

Current Market Situation

In the email sent to subscribers following Thursday's US trading session, we

wrote:

"In situations such as this it's best to take the evidence and review the

situation day by day. No short-term forecasting (that is, guessing) is

necessary. For example, if the HUI simply closes higher on Friday it will open

up the possibility of next week being similar to each of the past two weeks,

with a sharp 1-2 day pullback early in the trading week followed by a quick move

back to or above the year's high. Alternatively, a lower close on Friday

followed by a second lower close next Monday would indicate that a short-term

top was probably in place."

There was a small decline in the HUI on Friday. This tells us nothing in

isolation, but if it is followed by a significantly larger decline on Monday

then we will have evidence of a short-term top.

With regard to price levels that would have to be breached to confirm a

short-term top, for the HUI it's 140 (see chart below). This is more than 10%

below the current price and is therefore too low for practical purposes.

However, the XAU, by virtue of its relative weakness over the past several

months, is closer to important support and would therefore have to fall by a

lesser amount to confirm a short-term reversal.

In the XAU's case (see chart below), critical daily-closing support lies at

57-58. The lower end of this support range is only about 5% below the current

price, which means that it is high enough to act as a timely indicator of a

downward reversal. That is, it would be reasonable to interpret a daily XAU

close below 57 as confirmation that a short-term top is in place.

The gold-mining indices remain very 'overbought' on a short-term basis, but the

evidence of a long-term bullish reversal is continuing to build-up. For one

example, the HUI has just achieved a second weekly close above its 80-week MA.

For another example, at the same time as it points to near-term downside risk,

the unusual extent to which the HUI has become stretched to the upside on a

short-term basis is longer-term bullish. The explanation was outlined as follows

in last week's Interim Update:

"Although the above chart indicates an 'overbought' extreme and suggests that

a correction will soon begin (if it hasn't already), it also supports the view

that a cyclical bull market has started. The reason is that the only times in

the past that the HUI got close to being as stretched to the upside on a

short-term basis as it was last Friday was during the first 6 months of the

multi-year rally that began in November-2000 and the first few months of the

multi-year rally that began in October-2008."

It will probably take a decline to the vicinity of the HUI's 50-day MA to create

the next sector-wide short-term buying opportunity, but in the meantime there

will be opportunities to buy individual gold stocks.

What to do?

The primary focus at this time should be on raising cash by gradually scaling

out of stocks that have moved rapidly upward over the past several weeks, while

maintaining 'core' exposure to the gold sector. Unless you sell into the

periodic surges you won't be in a position to buy during the subsequent purges.

At this stage, however, we can't rule out the possibility of an over-stretched

market becoming even more so or the possibility that the overbought condition

will be worked off via a choppy sideways consolidation. In either of these

cases, the gold stocks that are likely to outperform are the ones that offer

substantial leverage to changes in the gold price and are still at depressed

levels. Three examples are Orvana Minerals (ORV.TO), Resolute Mining (RSG.AX)

and Timmins Gold (TGD). RSG and TGD are members of the TSI List. ORV is not a

TSI stock selection, but it has been discussed at TSI over the past few months

(refer to the 21st December Weekly Update for the most recent note).

The above-mentioned stocks are current producers that transition from being

loss-making or marginal at $1150-$1200/oz to being profitable at $1250-$1300/oz.

This transition dramatically changes the value of the company.

Of course, if it starts to look like gold's rally is over then these stocks will

quickly give up their gains.

The Currency Market

The chart displayed below compares the SPX/MSWORLD ratio with the Dollar Index

over the past 15 years. MSWORLD is a proxy for global equity performance

excluding the US, so the SPX/MSWORLD ratio is an indicator of US equity

performance relative to the performance of equities in the rest of the world.

It is clear from the chart that on an intermediate-term basis the Dollar Index

usually trends in the same direction as the SPX/MSWORLD ratio. Moreover, the

chart also shows that the SPX/MSWORLD ratio tends to lead the Dollar Index at

important turning points. In other words, it shows that relative strength in US

equities tends to be followed by strength in the Dollar Index and relative

weakness in US equities tends to be followed by weakness in the Dollar Index.

A downward correction in the SPX/MSWORLD ratio during the first quarter of last

year has been followed by a strong rally to new highs. The following chart's

overarching message is therefore that the Dollar Index will break decisively

above its March-2015 peak sometime this year.

There's a good chance that the Dollar Index will trade at least a few points

above its March-2015 peak before this year is over. The main question is: will

the start of a rally to new multi-year highs be preceded by a decline to near

the bottom of the 12-month range (the low-90s)?

Based on the recent price action the answer to the above question is: yes, it

probably will be. However, all it would take to negate the recent short-term

bearish evidence is a weekly close above 97.5.

Unless the facts change in the meantime, our intermediate-term outlook for the

Dollar Index will shift from "neutral" to "bullish" following either a decline

to the low-90s or a weekly close above 97.5.

By the way, the Dollar Index is dominated by the USD/EUR exchange rate. A

bullish view on the Dollar Index therefore implies a bearish view on the euro,

but it doesn't necessarily imply a bearish view on other currencies. In

particular, we wrote in our 2016 forecast that we expected the Yen to be this

year's strongest major currency. That expectation is intact.

Updates

on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Company

news/developments for the week ending Friday 19th February 2016:

Company

news/developments for the week ending Friday 19th February 2016:

[Note: AISC = All-In Sustaining Cost, FS = Feasibility Study, FY = Financial

Year, IRR = Internal Rate of Return, MD&A = Management Discussion and Analysis,

M&I = Measured and Indicated, NAV = Net Asset Value, NPV(X%) = Net Present Value

using a discount rate of X%, P&P = Proven and Probable, PEA = Preliminary

Economic Assessment, PFS = Pre-Feasibility Study]

*Dalradian Resources (DNA.TO) reported the results from the fourth

batch of holes from a 50,000m infill drilling program at its Curraghinalt gold

project in Northern Ireland. The purpose of this drilling program is to convert

Inferred resources to Indicated resources in support of a Feasibility Study

scheduled for completion in Q3-2016. As was the case with earlier results, the

latest drilling results included some good intercepts and appear to be

consistent with the resource estimate.

To date, the results associated with about 40,000m of the 50,000m program have

been released. The program's remaining holes are almost complete and will

probably be reported in a single batch within the coming 2 months.

If the figures in DNA's Oct-2014 PEA are in the right ballpark then DNA offers

very good value near its current share price assuming a gold price of $1200. In

fact, based on the PEA figures we can easily justify a C$2/share valuation for

DNA at the current gold price. However, the 'P' is in PEA for a good reason. The

economic analysis is Preliminary and might not be substantiated by the far more

rigorous Feasibility-level analysis. That, of course, is why you can currently

buy DNA shares in the C$0.80s.

*Evolution Mining (EVN.AX) published its half-year report for the

2016 Financial Year.

The company made what it refers to as an "underlying net profit" (the net profit

excluding acquisition-related charges) of A$108M. If we annualise this figure

and divide the result by the total share count (1463M) we get A$0.15/share.

Applying a 10-15 multiple to this net earnings figure gives us a fair value for

EVN of A$1.50-$2.25 per share.

This is consistent with our previously-expressed view that EVN is worth around

A$2.00/share at the current gold price.

The balance sheet included with the half-year report shows that EVN had A$25M of

working capital and long-term debt of A$409M at 31st December, for net debt of

A$374M. This is a comfortable amount of debt for a profitable 800K-oz/year gold

producer with a market cap of around A$2.6B (at A$1.80/share).

*Pretium Resources (PVG) advised that construction at the

Brucejack gold mine remains on track for commissioning in Q3-2017. PVG also

published its updated capital cost estimate for the mine. This is important new

information that was originally scheduled (by the company) to be provided in

Q4-2015.

The estimated capital cost has fallen by US$106M from US$747M to US$641M.

Looking at the details we see that the updated capex estimate includes a $145M

exchange-rate benefit and the transfer of $23M of cost from initial capital to

sustaining capital. It could therefore be said that the capital cost has

increased by $62M, but the increase has been more than offset by a fortuitous

movement in the C$/US$ exchange rate and the shifting of some cost from pre- to

post-production.

In any case, it's good news that the mine is now expected to cost significantly

less than originally estimated.

The lower capex and other changes have improved the economics of the Brucejack

project. Assuming a gold price of $1100/oz and a silver price of $14/oz, the

project is now estimated to have an NPV(5%) of US$1.55B. This compares to the

NPV of $1.45B estimated in the June-2014 FS assuming the same gold price and a

$3/oz higher silver price.

Taking into account the revised capex estimate and the amount of working capital

that will be needed between now and when the mine is expected to become

cash-flow positive, PVG will need to raise about US$100M. This will most likely

happen via an equity financing. Furthermore, although PVG probably won't need to

raise the additional money until next year, it's possible that the recent

relative sluggishness of PVG's share price is at least partly due to

anticipation of a sizable equity financing happening in the near future. The

recent relative weakness in PVG's share price could also be related to the

on-going concern regarding the validity of the Brucejack resource estimate.

Assuming that PVG has to issue 20M new shares, the Brucejack economics presented

in last week's press release suggest a valuation of about US$9.40/share at a

gold price of $1100/oz, about US$11.30/share at a gold price of $1200/oz, and

about US$14.30/share at a gold price of $1400/oz. Given the uncertainty about

the resource estimate and therefore the published economics, it is not

unreasonable to apply a 50% discount to these figures. Doing so gives us a fair

value estimate for PVG of US$5.50-$6.00 (C$7.50-$8.20) at the current gold

price. PVG ended last week at US$5.13 (C$7.05).

*Ramelius Resources (RMS.AX) published its half-year report for

the 2016 Financial Year.

The 6-month after-tax profit was A$21.9M, which was slightly higher than we

estimated last week. Annualising the 6-month profit and dividing the result by

the total share count of 470M gives us an earnings-per-share estimate of A$0.092

for the current financial year. If we then assume that the company is worth 5-10

times its current annual earnings we arrive at a back-of-the-envelope valuation

range of A$0.46-A$0.92.

As stated last week, we think it makes sense to use the low (5X) earnings

multiple and, therefore, the lower end of the aforementioned valuation range.

The reason is that RMS's profitability currently depends on adding high-grade

ore from small satellite deposits to the ore obtained from its Mt Magnet mine.

As also stated last week, if we became confident that the company was going to

at least maintain its current level of production for several more years then we

would use a higher earnings multiple.

RMS has a strong balance sheet, with A$31.5M of working capital and no long-term

debt.

List

of candidates for new buying

From within the ranks of TSI stock selections the best candidates for new buying

at this time, listed in alphabetical order, are:

1) DNA.TO in the low-C$0.80s (last Friday's closing price: C$0.88)

2) FCG (last Friday's closing price: US$3.36)

3) IVN.TO (last Friday's closing price: C$0.66)

4) PRQ.TO (last Friday's closing price: C$3.00)

5) TGD at around US$0.20 (last Friday's closing price: US$0.22)

Note that the above list is limited to five stocks. It will sometimes contain

less than five, but it will never contain more than five regardless of how many

stocks are attractively priced for new buying.

Second

RGLD call option exited

From the email sent to subscribers after Thursday's US trading session:

"...for TSI record purposes we are going to exit the remaining Royal Gold (RGLD)

Jan-2017 $40 call option position at Thursday's closing price of US$11.00. Based

on our December entry at $4.90, the result was a profit of 125%. Traders who

scaled into the options during the weeks following our original buy suggestion

should have achieved a much higher profit result."

We will consider new long-dated gold-stock call options following a significant

correction.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://www.barchart.com/