![]()

![]()

![]()

![]()

-- Weekly Market Update for the Week Commencing 23rd April 2018

Big Picture

View

Here is a summary of our big picture

view of the markets. Note that our short-term views may differ from our

big picture view.

The BULL market in US Treasury Bonds that began in the early 1980s ended in mid-2016, but there will be many years of topping action in bond prices and bottoming action in bond yields before major new trends get underway. A major decline in government bond prices will unfold during the 2020s. (Last update: 11 September 2017)

The stock market, as represented by the S&P500 Index, commenced a secular BEAR market during the first quarter of 2000, where "secular bear market" is defined as a long-term downward trend in valuations (P/E ratios, etc.), gold-denominated prices and inflation-adjusted prices. This secular trend will bottom in 2020 or later. (Last update: 11 September 2017)

A cyclical BEAR market in the US Dollar began in 2016-2017. (Last update: 11 September 2017)

Gold commenced a secular bull market relative to all fiat currencies, the CRB Index, bonds and most stock market indices during 1999-2001. This secular trend will peak in 2020 or later. (Last update: 11 September 2017)

Commodities,

as represented by the CRB Index, commenced a

secular BULL market in 2001 in nominal dollar terms. The first major

upward leg in this bull market ended during the first half of 2008, but

a long-term peak won't occur until 2020 or later.

(Last

update: 11 September 2017)

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

True

Fundamentals Summary

[Notes:

1) The date shown next to the current True Fundamentals Model (TFM) signal is

when the most recent change occurred. 2) Charts of the Gold and Equity

TFMs are included in the "Charts and Indicators" section of the TSI web

site]

| Market | True Fundamentals Model (TFM) |

| Gold (US$ Price) | Bearish (12 Jan 2018) |

| US Equity (SPX) | Neutral (20 Apr 2018) |

| Currency (Dollar Index) | Neutral (20 Apr 2018) |

| Commodities (GNX) | Neutral (20 Apr 2018) |

Last week's posts at the TSI Blog

Bull market correction or bear market?

A dramatic upward reversal in US monetary inflation

Summary of current

thinking/positioning

1) A number of markets are set

up for trend reversals or accelerations, with the US$ being the linchpin.

If the DX breaks out to the downside from its recent narrow range, rallies

should begin or accelerate across the commodity world with silver bullion

and gold-mining stocks leading the way higher. However, if the DX breaks

out to the upside from its recent range then the commodity world will be

pressured downward for at least a few weeks thereafter.

2) The SPX

is about to either end its correction or escalate the significance of the

January-2018 top by breaking to a new low for the year. The former outcome

is the more likely, but mainly due to rising interest rates there remains

the threat of a trend-ending plunge to a new low for the year.

3)

The multi-year upward trend in commodity prices that got underway in

early-2016 appears to have resumed. If so, the Australian and Canadian

dollars should be relatively strong over the next few months.

4) We

expect the next downward leg in the bond bear market to begin within the

next few weeks, but due to the huge speculative net-short position in

10-year T-Note futures we aren't yet interested in placing a new bearish

bet.

5) Holding a cash reserve of around 30%.

The burgeoning

economic war between governments

The US government has threatened

to implement tariffs on $150B of imported goods from China. It isn't yet

known what the final tariff tally will be and which products will be

affected, because there will be a great deal of lobbying between now and

when the threats are transformed into actions. China's government, of

course, has threatened to retaliate. The full details of the Chinese

retaliation also aren't yet known, but US companies that are heavily

reliant on doing business in China should be worried. The war recently

moved beyond tariffs, though, when the US government fired a shot against

Russia by imposing sanctions on a number of Russian oligarchs and major

Russian commodity-producing companies. This led to rapid rises in the

prices of aluminium and nickel. Then, over the past week, there was

another development in the expanding economic war, with the US government

firing potentially the most important shot to date.

Potentially the

most important shot to date is the US ban on sales of American components

to ZTE Corp, a large Chinese manufacturer of telecommunications equipment.

The ban was put in place because ZTE broke a 2017 settlement agreement

relating to the sale of equipment to off-limit countries such as Iran.

Regardless of whether or not ZTE's actions justified severe

punishment, the US government has inserted itself between international

trading partners in a way that not only could destroy a large Chinese

company, but also could have negative effects on many US companies and the

overall US economy. In the short-term the negative effects will be limited

to the US companies that were suppliers to ZTE (e.g. Qualcomm) and the US

companies that end up getting targeted for punishment by China's

government in retaliation for the heavy-handed treatment of ZTE, but there

is a much bigger issue here. The bigger issue is that the US government

has, in effect, just made the following announcement to the world: "If at

all possible, do not put yourself in the position where you are reliant on

US technology".

Many governments and corporations around the world

will take notice. Moreover, the US government's ban on the sale of US-made

components to ZTE has been a propaganda victory for Xi Jinping, China's

dictator. Xi has warned for years that it was dangerous to depend on

technology purchased from the US, and he has just been proved right. This

will give additional impetus to the "Made

In China 2025" program. Refer the article posted

HERE for more information on how the ZTE decision is being portrayed

in China.

Furthermore, the increasing politicisation of

international trade and the retaliations of other governments to the

actions of the US government will make US corporations more wary about

relying on foreign suppliers, especially foreign suppliers of critical

commodities. In an effort to avoid a politically-motivated supply

disruption it is therefore conceivable that in the future US manufacturers

and utilities will be willing to pay substantially higher prices for

locally-sourced commodities and will encourage local supply by making

investments in US-based commodity producers.

In summary,

economically-important parts of the world are being forced to turn inward.

The economies of all countries will be hurt by this war, with

consumers taking the brunt of the punishment. Economic progress will be

slowed, many consumer goods will become more expensive and living

standards will be lowered. However, there will be winners. For example,

gold and gold-mining shares are potential winners from declining

confidence associated with the economic war, and some industrial-commodity

producers will be able to sell at higher prices due to being 'local'.

Also, there will be winners from specific policy missteps, such as the

aluminium and nickel producers that benefited from the Russia sanctions

and the phone makers that will benefit from the destruction of ZTE's

business.

Oil & Gas

Oil versus oil stocks

Last week the oil price made a small gain, thus solidifying the break

to a new 3-year high that happened during the preceding week. Speculative

sentiment remains riskily stretched into optimistic territory, but the

physical supply-demand situation remains bullish. So, there was no change

of significance in the oil market last week.

Today we'll take a

look at how oil equities trade relative to the commodity, using XLE (the

Energy Select Sector SPDR ETF) and XOP (the SPDR S&P Oil and Gas E&P ETF)

as proxies for oil equities.

Displayed below are charts that

compare the oil price with the XLE/oil ratio and the XOP/oil ratio. These

charts show that there is a strong INVERSE correlation between the price

of oil and the performances of oil stocks relative to oil. Putting it

another way, the charts show that there is a strong tendency for oil

stocks to rise by less than the spot price of oil when the oil price is in

an upward trend and to fall by less than the spot price of oil when the

oil price is in a downward trend.

Oil stocks are generally the opposite of leveraged plays on the oil

price because most oil producers do not sell most of their oil in the spot

market. Instead, they make extensive use of hedging, so that in a rising

oil-price environment they typically will be delivering the bulk of their

production into contracts that were entered into at lower prices and in a

falling oil-price environment they typically will be delivering most of

their production into contracts that were entered into at higher prices.

Also of significance is that when oil fundamentals are bullish the spot

oil price will tend to be high relative to prices for delivery in 1-2

years' time, which means that new hedging will be undertaken at prices

that do not fully reflect the rise in the spot price. The opposite occurs

when oil fundamentals are bearish.

This doesn't mean that you

shouldn't buy oil stocks if you are bullish on oil. The reality is that

unless you have a large oil-storage facility and the financial ability to

fill the facility, it will be difficult for you to purchase an investment

that tracks or leverages changes in the spot price of oil. You will have

to make do with oil futures or ETFs that hold oil futures contracts or the

stocks of companies that deliver oil into futures contracts. An

alternative would be to buy the stocks of companies that are focused on

oil exploration, but these stocks will tend to be driven as much or more

by exploration results than by changes in the oil price.

The natgas market is overdue for a rally

The oil-price

strength of the past 8 months has done nothing for the natural gas (NG)

market. As illustrated by the following chart, the NG price has been

working its way downward in 'choppy' fashion since the end of 2016. It

made a new 12-month low in February-2018 and remains close to its 12-month

low.

The relatively low NG price has affected supply in a predictable way

(supply has reduced). This is evidenced by the next chart, which shows

that the amount of NG in below-ground storage in the US is 26% below the

5-year average for this time of the year and 38% below the year-ago level.

It's likely that a significant price increase will be required to

encourage producers to boost NG supply. At the same time, the market is

now acutely vulnerable to a positive shift in demand.

The upshot is

that there's a good chance of a tradable rally in the NG price over the

coming few months.

One of the simplest and safest ways to

participate in the rally would be by purchasing shares of the

First Trust Natural Gas ETF (FCG), a chart of which is displayed

below. This ETF has languished along with the NG market since late-2016

but is beginning to show signs of life.

A higher-risk/higher-reward

alternative to FCG would be a beaten-down junior producer such as Petrus

Resources (PRQ.TO).

The Stock Market

Sentiment, the yield

curve and credit spreads

Here's how we concluded a

post at the TSI blog early last week:

"While sentiment was

consistent with a major top and valuations, on average, were definitely

high enough to usher in a major top, an end to the long-term upward trend

was not signaled by several important indicators. For example, there would

normally be a pronounced widening of credit spreads at or before a bull

market top, but credit spreads remain near their narrowest levels of the

past 10 years. For another example, there is likely to be a reversal in

the yield curve from flattening to steepening at or prior to a bull market

top, but at the end of last week the US yield curve was at its 'flattest'

in more than 10 years. For a third example, there has been more strength

in market internals over the past two months than there normally would be

if we were dealing with the early stage of a bear market.

So,

despite the rampant optimism evident in January-2018, the decline that

followed the January peak probably will turn out to be a bull-market

correction."

The blog post referred to the absence of

reversals in the yield curve and credit spreads, but didn't provide any

evidence. The relevant evidence is in the following two charts.

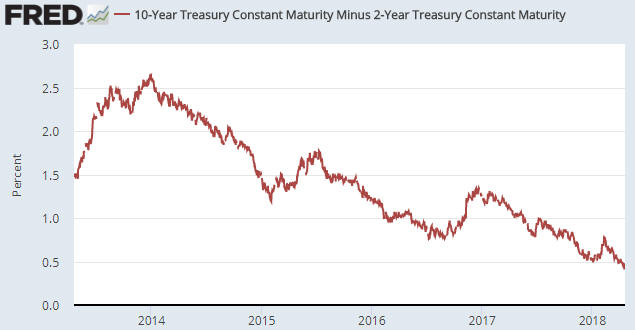

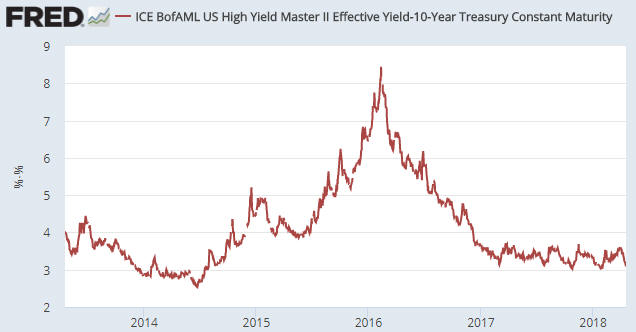

The

first chart shows that the 10yr-2yr yield spread, a proxy for the US yield

curve, has been in a major downward (flattening) trend since early-2014.

This yield spread hit its lowest level in more than 10 years last Tuesday.

The second chart shows the spread between an index of non-investment grade

publicly-issued corporate debt yields and the 10-year T-Note yield -- a

proxy for US credit spreads. This spread did not widen to a significant

degree during the January-March stock market turmoil and has since

returned to near its narrowest level in many years.

Current Market Situation

In last week's

Interim Update we mentioned the sudden and pronounced relative weakness in

the banking sector as indicated by a plunge, over the first three days of

the week, in the BKX/SPX ratio. We went on to write:

"We can't

come up with a good explanation for the sudden bout of relative weakness

in the banking sector. It could be argued that the demand for bank stocks

is declining due to a rise in the banking industry's interest expense

relative to its interest income, but the contraction of bank interest

margins is not a new development and therefore cannot be the main reason.

Also, the valuations of most US bank stocks are low relative to the

S&P500's valuation, so the problem isn't that bank stocks are too richly

priced.

Before we dive more deeply into this issue we want to see

if the relative weakness persists. If it does it will have implications

for other markets, most notably the gold market."

We were

right to wait to see if the relative weakness persisted before delving

deeper into the possible causes, because all the ground lost by the

BKX/SPX ratio during the first three days of last week was recouped during

the final two days of the week. In fact, over the course of the week the

ratio made a small gain.

Here's a chart showing the current

situation. The BKX is still precariously positioned slightly above a vital

support level, but its relative performance over the final two days of the

week was very good.

With the notable exception of the Bank Index, the important US stock

indices pulled back over the final two days of last week. In the cases of

the Dow Transportation Average (TRAN) and the Russell2000 SmallCap Index

(RUT), the pullbacks followed tests of resistance. As illustrated by the

following daily charts, TRAN has resistance at 10800 and RUT has

resistance at 1590. Getting above these resistance levels would project

new all-time highs within the ensuing month.

We ended the stock market section of last week's Interim Update by

noting:

"The biggest short-term threat facing the stock market

now is the same as the biggest threat that has faced it since the

beginning of the year: higher interest rates. The stock market has become

accustomed to a 10-year bond yield in the 2.80%-3.00% range, but it's

likely that at some point over the coming three months the 10-year yield

will move well above 3.00%. When it does it should usher in the next bout

of extreme stock-market volatility."

Interest rates moved

higher over the final two days of last week and the 10-year yield is now

perilously close to 3.0%. Just as importantly, the 30-year T-Bond price is

not far from its February low.

The following chart compares the

T-Bond price with the SPX. This chart shows that the sharp

January-February decline in the stock market came on the heels of a

downside breakout in the T-Bond. Stabilisation of the T-Bond then helped

the stock market to stabilise.

We expect that when the resumption

of the T-Bond's long-term bearish trend is signaled by a breach of the

February low (around 141.5), selling pressure will ramp up in the stock

market and the SPX will begin a decline to a new low for the year. Given

its position at the end of last week there is a risk that the T-Bond will

break below support as soon as this week. However, the odds favour a

T-Bond rebound over the coming few weeks.

Tesla (TSLA) Update

The TSLA price made a

short-term bottom in the $240s at the beginning of April and then, within

the space of only 4 days, rocketed back to former support (now resistance)

at $310. It has since consolidated in the $290-$310 range.

It's

possible that TSLA's rebound is over and that a decline to a new 12-month

low has begun, but it's also possible that the rebound will continue.

We don't understand why so many analysts and investors remain

steadfastly bullish on TSLA. After all, it's not like the numerous large

risks facing this company have been fully discounted by the stock market,

thus creating a situation where the high risk is more than offset by the

potential reward. The stock is being valued as if the company were about

to become enormously profitable, whereas the main question is: how long

will it be before the company's creditors 'pull the plug'?

The

stubborn optimism about Tesla's prospects makes it possible for the

company's carnival-barker-like CEO to periodically whip-up enthusiasm for

the stock. Anyone betting against this stock should keep this in mind and

manage risk accordingly. Our suggestion has been (and still is) to limit

the loss on a bearish speculation by exiting if the share price achieves

consecutive daily closes above $310.

On a related matter, recall

that a TSLA April-2018 put option was removed from the TSI List at a large

profit in late March. Our exit price of around $13 was far from ideal

given that the options traded above $20 at the beginning of April, but

note that these options expired worthless last Friday. Consequently, if

the options had been held for an additional 3 weeks then a 370% profit

would have turned into a 100% loss. On the other hand, IF the stock's

sharp decline had continued for 2-3 more weeks, which it could well have

done, then the same options potentially could have been exited for a

2,000% profit.

The above paragraph highlights the risks and

opportunities associated with options trading. In a fast-moving market,

exiting an option position a little early can result in a lot of money

being left on the table, but exiting a position a little late can result

in a very negative outcome.

One way to balance the risks and

opportunities is to scale out of a long option position as its price

rapidly rises.

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date | Description |

| Monday Apr-23 | Existing Home Sales |

| Tuesday Apr-24 |

Case-Shiller Home Price Index New Home Sales Consumer Confidence |

| Wednesday Apr-25 | No important events scheduled |

| Thursday Apr-26 | Durable Goods Orders |

| Friday Apr-27 |

Q1-2018 GDP (prelim

estimate) Employment Cost Index Chicago PMI Consumer Sentiment |

Gold and the Dollar

A final point is that there has been an important early-May turning

point for the C$ during each of the past three years. There were highs in

early-May of 2015 and 2016 and a low in early-May of 2017. This is not

what we currently expect to happen, but if the C$ were to fall by enough

within the next two weeks to test or breach its March-2018 low it probably

would mean that we were getting another important early-May turning point

(in this case, from down to up).

Updates

on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() Company

news/developments for the week ending Friday 20th April 2018:

Company

news/developments for the week ending Friday 20th April 2018:

[Note: AISC = All-In Sustaining Cost, FS = Feasibility Study, FY =

Financial Year, IRR = Internal Rate of Return, ISR = In-Situ Recovery,

MD&A = Management Discussion and Analysis, M&I = Measured and Indicated,

NAV = Net Asset Value, NPV(X%) = Net Present Value using a discount rate

of X%, NSR = Net Smelter Return, P&P = Proven and Probable, PEA =

Preliminary Economic Assessment, PFS = Pre-Feasibility Study]

*Alio Gold (ALO) reported Q1 gold production of 17.6K

ounces. This news actually came out on 11th April but accidentally was

omitted from last week's TSI commentary.

Q1 guidance was 18K-20K

ounces, so the result was below plan. However, the company has maintained

its overall 2018 production guidance of 90K-100K ounces.

*Blackham

Resources (BLK.AX) published its quarterly report for the

March-2018 quarter. Most of the important information contained in this

report had been provided in earlier press releases.

The company

produced 20.6K ounces of gold at an AISC of A$1092/oz during the March

quarter and has maintained its guidance for the first half of this

calendar year at 40K-45K ounces at an AISC of A$1100-$1200. Considering

that sustaining capital expenditure should be lower during the June

quarter than during the March quarter, we expect that the actual AISC for

the half year will be well below the bottom of the aforementioned guidance

range.

There are historical tailings at BLK's Wiluna project that

are estimated at 37M tonnes averaging 0.71-g/t gold. This implies a gold

resource of about 800K ounces. Metallurgical testwork carried out to date

indicates gold recovery of 45%-50%, which suggests the potential for BLK

to add 350K-400K ounces of relatively low-cost production to its overall

mine plan.

The tailings opportunity (called "Wiltails") will have

to be confirmed by drilling, additional metallurgical testing and economic

studies, but it could give the per-share value a significant boost.

*Continental Gold (CNL.TO) reported a new

batch of results from its 2018 drilling program. The best intercepts were

0.55m of 606-g/t gold and 1.95m of 110-g/t gold. These intercepts have

potentially identified new shoots of very high-grade gold on two different

veins within part of the M&I resource envelope.

*Energold

Drilling (EGD.V) published its 2017 annual financial results.

Revenue for the year was about C$10M higher than the preceding year.

This is clear-cut evidence that EGD's drilling business has turned the

corner, but unfortunately the higher revenue did not translate into a

better overall financial performance.

EGD's balance sheet remains

strong, with adjusted working capital (current assets minus current

liabilities and long-term debt) of C$36M. However, this is down by C$9M

from the end of the preceding quarter, so the company has continued to

bleed cash despite the increasing demand for its services.

The

adjusted working capital equates to about C$0.65/share, which suggests

that EGD is cheap near its current share price of C$0.41. It must convert

its growing revenue into free cash-flow, though, for there to be a large

and sustained increase in its stock price.

*Premier

Gold (PG.TO) reported a good overall production result for the

March quarter, with lower-than-planned production at the company's

100%-owned Mercedes gold mine in Mexico being more than offset by

well-above-plan production at the 40%-owned South Arturo gold mine in

Nevada. Total production for the quarter was 30.5K ounces.

This

puts PG on track to exceed its 2018 gold production guidance of 85K-95K

ounces.

![]() List

of candidates for new buying

List

of candidates for new buying

From within the ranks of TSI

stock selections the best candidates for new buying at this time, listed

in alphabetical order, are:

1) ALK.AX (last Friday's closing price:

A$0.28)

2) AOI.TO (last Friday's closing price: C$1.24)

3)

EGD.V (last Friday's closing price: C$0.41)

4) PG.TO (last Friday's

closing price: C$2.64)

5) PRQ.TO (last Friday's closing price:

C$1.24)

The above list is limited to five stocks. It will sometimes

contain less than five, but it will never contain more than five

regardless of how many stocks are attractively priced for new buying.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://research.stlouisfed.org/