![]()

![]()

![]()

![]()

-- Weekly Market Update for the Week Commencing 23rd December 2019

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

True

Fundamentals Summary

[Notes:

1) The date shown next to the current True Fundamentals Model (TFM) signal is

when the most recent change occurred. 2) Charts of the Gold and Equity

TFMs are included in the "Charts and Indicators" section of the TSI web

site]

| Market | True Fundamentals Model (TFM) |

| Gold (US$ Price) | Bearish (20 Dec 2019) |

| US Equity (SPX) | Bullish (20 Dec 2019) |

| Currency (Dollar Index) | Neutral (15 Mar 2019) |

| Commodities (GNX) | Bearish (01 Jun 2018) |

Last week's posts at the TSI Blog

Gold is not a hedge against "CPI inflation"

Summary of current

thinking/positioning

1) The Dollar Index (DX) remains

range-bound, needing a weekly close below 96.5 to signal an

intermediate-term reversal to the downside or a weekly close above 99.5 to

signal an intermediate-term rally. We are anticipating the former, but we

are uncertain as to whether it will happen in the near future or during

the first few months of next year.

2) The gold bullion market is at

odds with the gold mining sector, in that the latter has signaled an

upward reversal of its short-term trend whereas the former has not.

There's a good chance that this conflict will be resolved within the

coming week.

3) The senior US stock indices probably will make

multi-month tops between late-December and mid-January.

4) The

T-Bond made a short-term bottom in early-November, but there is still risk

of downward acceleration over the coming month or two. Regardless of what

happens in the short-term, there's a good chance that major price weakness

will be seen in 2020. In other words, it looks like higher interest rates

are on the way.

5) Industrial commodities such as oil and copper

appear to be in the process of bottoming, with intermediate-term price

lows either already in place or likely to be set early next year.

6) We are holding a cash reserve of 25%-30%.

TSI Holiday

Season Schedule

Due to Christmas, New Year and

related personal plans/commitments, for the next three weeks there will be

no Interim Update. However, we will continue to publish the Weekly Update

at around the usual time each week. For example, there will be no Interim

Update on Thursday 26th December, but there will be a Weekly Update on

Sunday 29th December.

I wish you a happy Holiday Season and the

best of luck in 2020!

The T-Bond is on

the edge

The T-Bond price has pulled back

to within one point of its November low and its 200-day MA. Refer to the

following chart for the details. Therefore, to avoid a potentially serious

downside breakout it will have to rebound soon.

If it fails to

embark on a significant rebound and instead ends a week below 155, the

scene would be set for a larger and faster decline.

A downward move in the bond price means an upward move in the bond

yield, which usually goes hand-in-hand with a rise in the copper price

relative to the gold price (a rise in the copper/gold ratio, that is). The

positive correlation between the copper/gold ratio and the 10-year bond

yield is illustrated below.

Jeffrey Gundlach, a famous bond fund manager, says that the

copper/gold ratio is a good predictor of the 10-year bond yield, but we

disagree because there is no consistent lead-lag relationship between the

two. The 10-year yield generally moves in the same direction as the

copper/gold ratio, but more often than not they change direction at the

same time. For example, both the 10-year yield and the copper/gold ratio

turned upward in early-September of this year and have since risen

together.

An implication is that the recent performance of the

copper/gold ratio can't be used reliably to predict the future performance

of long-term interest rates. Instead, to use the copper/gold ratio as an

indicator of what will happen to long-term interest rates in the future

you first must develop an opinion about what will happen to the

copper/gold ratio in the future. Looking from a different angle, a view

about the future direction of long-term interest rates leads to a view

about the future performance of copper relative to gold. For example, one

of the reasons we currently expect strength in copper relative to gold

over the next 12 months is that we expect bond yields to trend upward over

this period.

Anyhow, whether or not the T-Bond holds support

defined by its November price low will be one of the keys to what happens

throughout the financial world over the coming month or so. If the T-Bond

breaks support and accelerates downward it could precipitate a sharp

sell-off in the gold market. Also, it could be the catalyst for a sizable

stock market correction.

Time for the

palladium bubble to deflate?

Our most recent comment on the

palladium bubble was in the 21st October Weekly Update. At that time we

noted the similarities between the current bubble and the final stages of

the bubble that reached its zenith in early-2001. We concluded: "If

the rough similarity is maintained then today's market will reach its

final top between November of this year and March of next year."

It's too soon to be certain or even confident, but last week's

downward reversal in the palladium price could have marked the bursting of

the bubble and the start of a major decline.

Here, again, are the

weekly charts that illustrate the similarities between the current period

and the final stages of the palladium bubble that 'blew out' during

2000-2001.

The Stock Market

Sentiment Alert

Stock market sentiment has been optimistic over the past two months,

but not dangerously so given the steady rise in the S&P500 Index and the

positive market breadth. However, the situation changed last week.

Last week there was a surge in optimism that constitutes a loud warning

signal. The optimism surge is clearly evident in the latest calculation of

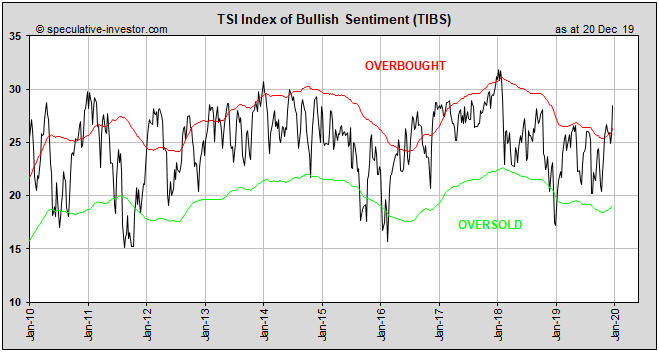

the TSI Index of Bullish Sentiment (TIBS).

TIBS is a weighted

average of six sentiment indicators. Most of the time it is not relevant,

because most of the time it simply follows the price and oscillates within

the moving-average (MA) envelope shown on the following weekly chart. It

only becomes relevant when it moves well below or well above the MA

envelope.

Moves by the TIBS to well below or well above its MA

envelope don't happen very often, which is why TIBS rarely gets mentioned

in TSI commentaries. The last time it happened was 12 months ago, when

TIBS spiked well below the lower boundary of its MA envelope and in doing

so signaled that the market was close to a multi-month bottom. The current

signal is the opposite. TIBS is now warning that the US stock market is

close to a multi-month top.

It isn't just stock market optimism that is immersed in what appears

to be a trend-ending surge. Despite the obvious weakness in the

manufacturing sector of the US economy, there also is evidence of a

trend-ending surge in economic optimism. We are referring to the sudden

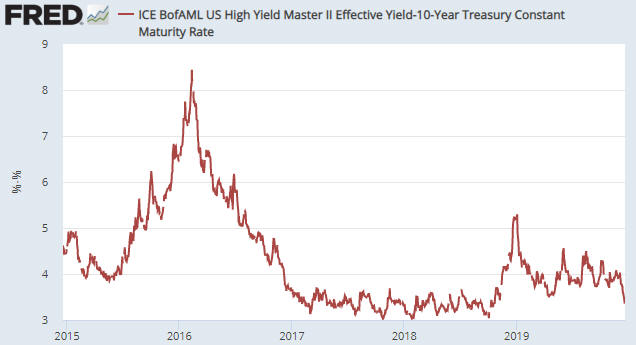

narrowing of credit spreads over the past few weeks.

The following

chart of a credit-spread indicator shows that credit spreads were rapidly

widening at this time last year, which signaled burgeoning fear of

economic weakness. The same indicator is now in the midst of a sharp

decline, indicating that whatever concerns there have been about economic

prospects are quickly evaporating.

In the same way that last

December's spike in economic pessimism marked a multi-month bottom for the

stock market, this December's spike in economic optimism could be marking

a multi-month top for the stock market.

Current Market Situation

The S&P500 Index

(SPX) continued its relentless advance last week. Seasonal/cyclical forces

suggest that the short-term upward trend will extend into the first half

of January, but the 1999 analogue warns that the top could occur at

year-end.

At this stage we are still anticipating nothing more

bearish than a 10% correction. The reason is that market breadth, one

indicator of which (the NYSE Advance-Decline Line) is shown in the lower

section of the following chart, continues to confirm the SPX's new highs.

The US stock market has never commenced a cyclical bearish trend

or suffered a crash with the Advance-Decline Line in an upward trend and

regularly making new all-time highs.

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date | Description |

| Monday Dec-23 | New Home Sales |

| Tuesday Dec-24 | Durable Goods Orders |

| Wednesday Dec-25 | Markets closed for Xmas Day |

| Thursday Dec-26 | US markets open, but many other markets closed for Boxing Day |

| Friday Dec-27 | No important events scheduled |

Gold and the Dollar

The HUI, a proxy for the gold-mining sector, managed to draw-out its

coiling pattern for an additional week by pulling back to near its 20-day

MA. The HUI looks like it is preparing to accelerate upward to a new

multi-year high, but for it to do so the gold price almost certainly will

have to break upward from its channel and also break above lateral

resistance in the $1520s.

The HUI and the other gold-mining sector proxies have been

strengthening relative to gold since the second week of October. This

recent relative strength is evidenced by the rising line on the following

chart of the HUI/gold ratio. The ratio pulled back last week, but it is

close to a multi-year high and will maintain a bullish posture as long as

it holds above its 40-day MA (the blue line on the chart).

Our Gold True Fundamentals Model (GTFM) flipped from bullish to

bearish last week, but as we explained a week ago: "The GTFM...is more

vulnerable than usual to being 'whipsawed' at the moment because four of

its seven inputs are very close to their tipping points. Consequently,

it's best to view the current fundamental backdrop as finely balanced."

With regard to the gold market, it's still best to view the fundamental

backdrop as finely balanced. The same, by the way, applies to the stock

market.

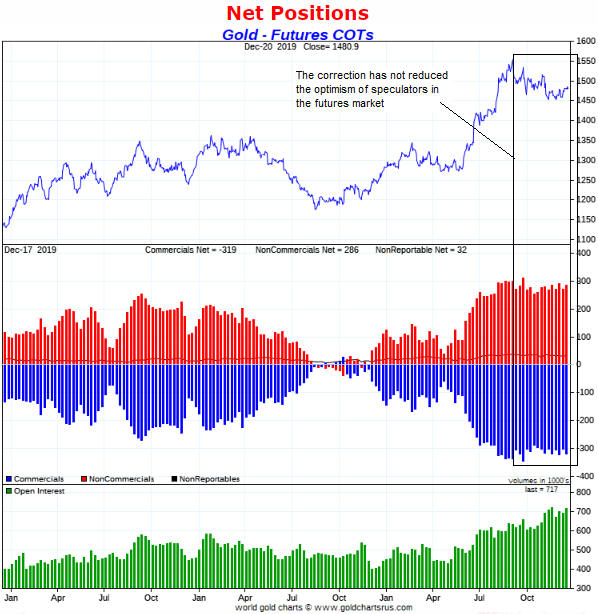

As has been the case for about four months, speculator

sentiment is the biggest obstacle facing the gold price. The total

speculator net-long position (the inverse of the blue bars in the middle

section of the following weekly chart) reached an extreme in August and

has remained at/near an extreme despite the downward drift in the gold

price since early-September.

The sentiment situation doesn't

preclude a rally that tests the 2019 high, but it makes a rally to well

above the 2019 high very unlikely and creates downside risk.

Based on the way the markets usually have traded relative to each

other over the past 10 years, for there to be significant strength in the

gold price over the next few weeks the T-Bond price will have to hold

above its November low. To put it another way, if the T-Bond makes a

sustained break to new multi-month lows then the US$ gold price probably

will end its coiling pattern by reversing downward.

The

Currency Market

On Friday 13th December the March-2020

Dollar Index (DX) successfully tested support at 96.5. Last week it

rebounded. Move along, nothing to see here.

A weekly close below 96.5 would warn that the DX was on its way to

94.5 or lower. We expect this to happen sooner or later, with later (after

January of next year as opposed to the next three weeks) being the more

bearish scenario. To further explain, if the DX were to break to the

downside within the next three weeks there would be a much greater risk of

the breakout being a 'fakeout' than if the break to the downside happened

in February or later.

The DX has been drifting with a slight upward

bias since the third quarter of last year, so it isn't surprising that

over the same period the euro has been drifting with a slight downward

bias. A weekly close above 1.12 would signal that this long period of

aimless drifting had ended and that a meaningful rally had begun,

especially if the break above 1.12 were to happen after January.

As

illustrated by the following weekly chart, the euro could move as high as

1.18 within the next 6 months while remaining within the confines of its

long-term downward-sloping channel. That's the sort of upside move we are

anticipating.

For the umpteenth time since March of 2018 the Australian dollar (A$)

has risen to its 200-day MA. Within the next few months it should break

out to the upside and signal an end to its long decline.

Updates

on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() Company

news/developments for the week ending Friday 20th December 2019:

Company

news/developments for the week ending Friday 20th December 2019:

[Note: AISC = All-In Sustaining Cost, EBITDA = Earnings Before

Interest, Tax, Depreciation and Amortisation (a measure of cash flow), EV

= Enterprise Value or Electric Vehicle, FS = Feasibility Study, FY =

Financial Year, IRR = Internal Rate of Return, ISR = In-Situ Recovery, JV

= Joint Venture, MD&A = Management Discussion and Analysis, M&I = Measured

and Indicated, NAV = Net Asset Value, NPV(X%) = Net Present Value using a

discount rate of X%, NSR = Net Smelter Return or Net Smelter Royalty, P&P

= Proven and Probable, PEA = Preliminary Economic Assessment, PFS =

Pre-Feasibility Study]

*Fortuna Silver Mines (FSM)

was added to the TSI List late last week. The stock has the right

attributes to be a long-term holding, but the current position is a

short-term trade with an expected duration of less than three months.

An initial daily-closing stop has been set at US$3.15, which means

that we won't give this trade much rope. It should either start working or

get stopped out within the next two weeks.

*Premier Gold (PG.TO) issued an operations

update that, as far as we can tell, provided no new information. According

to the update the Mercedes gold-silver mine in Mexico continues to

struggle, but actions have been that should lead to improved performance

in 2020. Also, the South Arturo project in Nevada continues to perform

well, with the El Nino underground mine having reached commercial

production ahead of schedule.

*Tinka Resources

(TK.V), an exploration-stage zinc miner operating in Peru,

announced a large equity financing. Most of the time, equity financings

that are done when the stock price is trading near a multi-year low -- as

was the case when TK arranged its financing -- have bearish implications.

However, TK's financing was/is very bullish. The reason is that almost all

of the new shares have been purchased under a subscription agreement by

Compania de Minas Buenaventura SAA ("Buenaventura"), a senior Peru-based

precious and base metals mining company listed on the NYSE (symbol: BVN)

and the Lima Stock Exchange, at a premium of 100% to TK's pre-announcement

share price.

Buenaventura will be investing C$16M at C$0.243/share

to purchase about 19% of TK. In addition, TK's largest shareholder, the

Sentient Global Resources Fund, has exercised its participation rights in

respect of the financing and will be purchasing C$2.5M of new shares at

the same price. Post-financing, Sentient will own about 22% of TK.

The aforementioned financing means that TK has become fully funded for at

least the next 12 months at a very attractive price in the context of the

current lousy market for base-metal explorers. Even more importantly, it

signals that Buenaventura is interested in eventually acquiring TK's

Ayawilca zinc project.

This is not just a vote of confidence in the

Ayawilca project from the smart money, it's a vote of confidence from the

smartest money and confirms that TK suits our modified approach to dealing

with speculative resource stocks. Given that we no longer can rely on the

periodic aggressive buying of the public to create excellent profit-taking

opportunities in junior resource stocks and that ETFs are diverting

investment away from the juniors and toward the stocks of larger

companies, we want to focus our attention on the mining juniors that own

mineral deposits of sufficient size and quality to be of interest to the

mining majors.

![]() List

of candidates for new buying

List

of candidates for new buying

From within the ranks of TSI

stock selections the best candidates for new buying at this time, listed

in alphabetical order, are:

1) ALK.AX (last Friday's closing price:

A$0.56)

2) AOI.TO (last Friday's closing price: C$1.18)

3)

FSM (last Friday's closing price: US$3.36)

4) JRV.AX/JRV.V (last

Friday's closing price: A$0.19/C$0.17)

5) TGB (last Friday's

closing price: US$0.42)

The above list is limited to five stocks.

It sometimes will contain less than five, but it never will contain more

than five regardless of how many stocks are attractively priced for new

buying.

![]() New

TSI stock selection: Galaxy Resources (ASX: GXY). Shares: 410M. Recent

price: A$0.89

New

TSI stock selection: Galaxy Resources (ASX: GXY). Shares: 410M. Recent

price: A$0.89

GXY was added to the TSI Stocks List in last

week's Interim Update. The company is a lithium producer/developer with a

strong balance, a production-stage lithium asset in Western Australia and

two development-stage lithium assets in the Americas.

GXY's Mt

Cattlin mine in Western Australia produces spodumene concentrate with an

average grade of around 6% LiO2 (lithium oxide). For the bulk of this year

the annualised production rate was around 200Kt.

Despite being a

low-cost producer, the decline of almost 50% in the market price of

spodumene concentrate over the past year, from above US$900/t to around

US$500/t, has caused part of the Mt Cattlin resource to become uneconomic.

In response, GXY's management has decided to emphasise value over quantity

in 2020 to ensure that the operation remains profitable. 2020 production

therefore is expected to be about half the 2019 level, but a return to the

2019 production level or higher will occur after it becomes clear that the

lithium market has turned around.

We are valuing Mt Cattlin at

one-times annual revenue, assuming the 2019 production level (190Kt) and

the current low spodumene price of US$500/t. This means that we are

currently valuing the asset at US$95M (A$138M).

Although it is

more than two years from production, GXY's most valuable asset is its Sal

de Vida (SDV) lithium brine project in Catamarca Province, Argentina. The

project is adjacent to Livent's Fenix lithium operation and could become a

large-scale producer of lithium carbonate (Li2CO3). The current schedule

is for a Final Investment Decision (FID) to be made in Q2-Q3 of 2020 and

for production to begin in 2022.

The FS completed in May-2018

estimated that it would cost US$474M to put SDV into production and that

the operation would have a post-tax NPV(8%) and IRR of US$1.5B and 26.9%

assuming US$14,000/t for Li2CO3. The estimated NPV and IRR drop to

US$1.05B and 22% assuming US$11,700/t for Li2CO3, which is still good.

However, the current Li2CO3 price is only about US$9,000/t.

It's

likely that SDV remains economically viable, because GXY has further

optimised the project over the past 18 months. Also, to reduce the initial

capex the company now plans to develop the project in two or three stages.

To arrive at a value for SDV we have applied a 50% discount to the

NPV figure that is based on a lithium carbonate price of US$11,700/t. That

is, we currently value SDV at US$500M (A$725M). The assumed selling price

is well above the current market price, but the 50% discount and the

post-FS improvements mean that the valuation is far from aggressive.

GXY's third lithium asset is the feasibility-stage James Bay spodumene

project in Quebec, Canada. This asset will become very valuable after the

lithium market turns around, but over the next year it probably will be on

the backburner. To be conservative, we are assigning no value to it at the

moment.

The most recent financial statements show that GXY has no

long-term debt and net cash of A$176M. This implies that the company will

be able to survive until growing EV-related demand causes a sustained

upward reversal in the lithium price trend. We expect that the turnaround

will happen in 2020.

Adding the company's net cash to the asset

valuations mentioned above results in a valuation of A$1,039M, or

A$2.53/share, for the company. This compares very favourably with the

current share price of A$0.89.

Also worth mentioning is that GXY is

attempting to sell a minority stake in its SDV project. In addition to

injecting a lot of cash into the company, if the sale process is

successful it should highlight the large gap between GXY's market cap and

its underlying value. In other words, there is a potential

company-specific catalyst for an upward re-rating of the stock.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/

http://www.goldchartsrus.com/

https://www.barchart.com/

https://research.stlouisfed.org/