--

Weekly Market Update for

24th June 2019

Big Picture

View

Here is a summary of our big picture

view of the markets. Note that our short-term views may differ from our

big picture view.

The BULL market in US Treasury Bonds

that began in the early 1980s ended in mid-2016, but there will be many years

of topping action in bond prices and bottoming action in bond yields before

major new trends get underway. A major decline in government bond prices will

unfold during the 2020s. (Last update: 11 September 2017)

The stock market, as represented by the S&P500 Index,

commenced

a secular BEAR market during the first quarter of 2000, where "secular

bear market" is defined as a long-term downward trend in valuations

(P/E ratios, etc.), gold-denominated prices and inflation-adjusted prices. This secular trend will bottom

in 2020 or later.

(Last update: 11 September 2017)

A cyclical BEAR market in the

US

Dollar

began in 2016-2017.

(Last

update: 11 September 2017)

Gold commenced a

secular bull market relative to all fiat currencies, the CRB Index,

bonds and most stock market indices during 1999-2001.

This secular trend will peak in 2020

or later.

(Last update: 11 September 2017)

Commodities,

as represented by the CRB Index, commenced a

secular BULL market in 2001 in nominal dollar terms. The first major

upward leg in this bull market ended during the first half of 2008, but

a long-term peak won't occur until 2020 or later.

(Last

update: 11 September 2017)

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

True

Fundamentals Summary

[Notes:

1) The date shown next to the current True Fundamentals Model (TFM) signal is

when the most recent change occurred. 2) Charts of the Gold and Equity

TFMs are included in the "Charts and Indicators" section of the TSI web

site]

|

Market |

True Fundamentals Model (TFM) |

|

Gold (US$ Price) |

Bullish (04 Jan 2019) |

|

US Equity (SPX) |

Bearish (19 Apr 2019) |

|

Currency (Dollar Index) |

Neutral (15 Mar 2019) |

|

Commodities (GNX) |

Bearish (01 Jun 2018) |

Last week's posts at the TSI Blog

There were no blog posts last week.

Summary of current

thinking/positioning

1) The Dollar Index (DX) has

commenced a downward trend, but it could be a few months before the new

trend becomes consistent. In the meantime the price action could be

choppy, beginning with a counter-trend rebound that kicks off within the

next two weeks.

2) The US$ gold price went straight to a 5-year

high (above $1377) without any intervening correction. Significant

additional gains are likely within the next three months, but a test of

last week's upside breakout probably will occur within the next three

weeks. The US$ silver price stands a good chance of making a catch-up move

over the months immediately ahead.

3) The gold-mining indices/ETFs

have blown through resistance levels and signaled that we are dealing with

intermediate-term upward trends rather than counter-trend reactions.

However, on a short-term basis they are now as 'overbought' as they ever

get, so a correction should begin soon.

4) The SPX made a marginal

new all-time high last week. The new high was not confirmed by other stock

indices and does not affect our view that a significant decline will get

underway by mid-July at the latest.

5) An upside blow-off has set

the stage for a large T-Bond decline. The decline should begin by early

July at the latest.

6) Oil's correction is probably very close to

complete, at least in terms of price, although stock market weakness

during July-August could push the oil price to a new multi-month low.

7) We are holding a cash reserve of 25%-30%.

The coming T-Bond

decline

A large divergence between two

fundamentally-correlated market prices is important because such a

divergence usually will be closed via a big move in one or both prices.

However, divergences sometimes build for an inconveniently long time

before they start to matter.

The gold/commodity ratio (the US$ gold

price divided by the GSCI Spot Commodity Index) and the T-Bond are

strongly correlated over the long term. They also tend to be well

correlated over shorter timeframes, but significant short-term divergences

sometimes occur. One such divergence has been developing since the

beginning of this year, with the T-Bond making a sequence of higher highs

while the gold/commodity ratio stays below its late-December high. Note

that even last week's impressive up-move and break to a new 5-year high by

the US$ gold price was not enough to push the gold/GNX ratio above its

late-December high.

The current divergence and previous similar

divergences (higher highs for the T-Bond in parallel with lower highs for

the gold/commodity ratio) are illustrated by the following chart. The

previous similar divergences led to large declines in the T-Bond price and

we can think of no reason to expect that it will be different this time.

Commodities

Oil confirms its double

bottom

A week ago we wrote that the oil price probably had

made a 'double bottom' that would hold for at least a few weeks. That

probability became a virtual certainty last week.

Last week the oil

price gained 9.4% and in doing so broke above resistance at $55. It has

moving-average resistance at $59-$60 that probably will limit the

near-term upside unless there is a further escalation of geopolitical

tension in Middle East.

Due to the strong positive correlation between the oil and stock

markets, there is still a risk that the oil price will breach its June low

before the overall correction is complete. However, market sentiment (as

indicated by the COT data) and fundamentals (as indicated by the oil

futures curve) are both supportive, so if there is a breach of the June

low it probably will be short-lived.

Copper Update

The copper price has spent the past 12 months oscillating between

support at $2.55-$2.60 and resistance at $2.95-$3.00. We won't be

surprised if it continues to 'chop around' aimlessly for up to three more

months, but the next substantial move is more likely to be higher than

lower.

Our intermediate-term bullish outlook for copper is based

more on macroeconomic factors and inter-market relationships than on

copper-specific supply/demand fundamentals. We think that inflation

expectations are bottoming and that the next 12 months will be

characterised by rising bond yields, a weakening US$ and strength in

late-cycle investments/speculations.

The Stock Market

The Fed and the "trade

war"

As we warned could happen a couple of weeks ago, the

S&P500 Index (SPX) has made a new all-time high. The buying pressure that

led to this new high was generated, at least in part, by optimism

regarding easier monetary policy and a cease-fire in the US-China "trade

war". Hope that the Fed will soon start cutting its targeted interest

rates was bolstered last week by strong hints from the Fed, while hope for

a US-China trade deal was rekindled by news that presidents Trump and Xi

will meet on the sidelines of the G20 meeting to be held in Osaka on June

28-30.

The best that can be reasonably expected from a trade deal

at this time is the removal of the tariffs put in place over the past

year, although if a deal is done it certainly will have other aspects. For

example, the Chinese government probably will agree to the purchase of

more US-produced agricultural and energy commodities, because they already

agreed to that a year ago, and commit to doing more to protect

"intellectual property rights", because it wouldn't cost them anything to

make such a commitment. They also could promise to maintain a stable

Yuan/US$ exchange rate, because they most likely see it as in their

interest to do so in order to minimise capital flight and reduce the costs

of imported goods. What they won't do (regardless of any promises to the

contrary) is slow the pace of the "Made in China 2025" program or the pace

at which China's sphere of influence is broadened via strategies such as

the "Belt and Road Initiative".

Ironically, if the stock market

gets what it wants on the international trade front then the chance of it

getting what it wants (and currently expects) from the Fed will be greatly

reduced. The reason is that the removal or scaling-back of the government

actions that are crimping international trade and depressing economic

growth will make a series of pre-emptive rate cuts seem less appropriate.

Therefore, we suspect that if a trade deal is done within the next few

weeks then the Fed either won't cut its targeted rate at the next FOMC

meeting (scheduled for end-July) or will make a 0.25% cut in July and use

words that imply a wait-and-see approach regarding further cuts. Putting

it another way, getting what the market currently expects from the Fed

over the next six months probably requires the continuation of the "trade

war".

Is there any evidence of a bear market?

Late last year there were signs that US equities had commenced a

cyclical bear market, but most of these signs disappeared in January. One

long-term bearish sign that didn't disappear early this year and remains

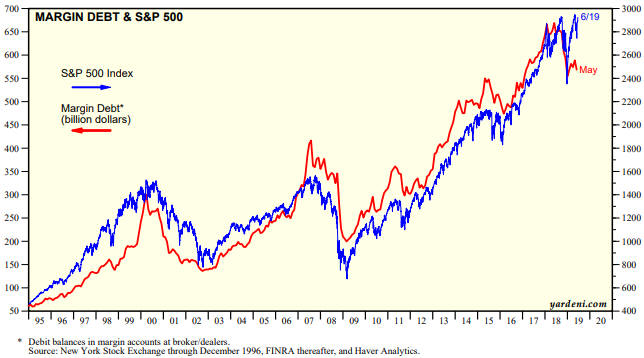

in place today is the downward reversal in Margin Debt. The following

chart shows that last year's downward reversal in NYSE Margin Debt is

similar to the reversals that occurred around major price tops in 2000 and

2007. It also shows that Margin Debt did not recover with the SPX during

the first half of this year.

The measure of margin debt displayed above could be providing a

misleading signal, however, because it isn't adjusted for the size of the

market. In the same way that government-debt/GDP is a more meaningful

figure than government debt in nominal currency terms, to get a feel for

the extent of debt-based leverage in the stock market it probably makes

more sense to look at margin debt as a percentage of total stock market

capitalisation than to look at the dollar value of margin debt.

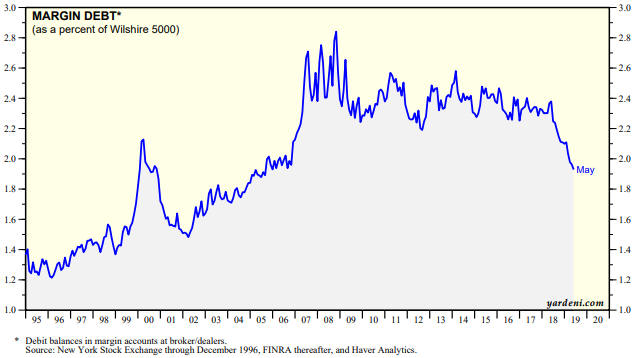

When margin debt is calculated relative to the overall market, a very

different picture emerges. The picture is shown below, using the

Wilshire5000 to represent the entire US stock market.

The following

chart shows that unlike 2007-2008 and 1999-2000, there was no surge in the

adjusted Margin Debt in the lead-up to last year's price top. Instead,

this measure of debt-based leverage was essentially flat during 2009-2017

and turned down without first rocketing upward. It is now at its lowest

level since 2005.

Note that the above charts were taken from

https://www.yardeni.com/pub/stmkteqmardebt.pdf.

Perhaps it is

different this time and a major price top has been put in place without a

preceding surge in the adjusted Margin Debt figure, but when we consider

all the evidence (more to the point: the absence of bear-market evidence)

we arrive at the conclusion that the cyclical bull market probably will

extend into 2020.

Current Market Situation

The following daily chart shows the new all-time high made late last week.

If this marginal new high had been accompanied by a bearish divergence in

the NYSE Advance-Decline Line (ADL) then, given that a put/call sell

signal is in effect, we now would be very enthusiastic about bearish stock

market speculations. However, the chart also shows that the ADL remains

very strong and actually led the SPX into new high territory. This tempers

our enthusiasm for bearish stock market bets, although we bought some SPY

September $270 put options late last week as much for hedging purposes (to

hedge exposure to non-gold commodity stocks) as for speculating purposes.

Aside from the put/call sell signal, the main reason to be concerned

at the moment about short-term downside risk is that most US stock indices

are not showing as much strength as the SPX. For example, the following

chart shows that the June rebound in the Dow Transportation Average (TRAN)

has, to date, only retraced about half of the May decline and that TRAN

ended last week below its 50-day and 200-day MAs.

We continue to expect that another multi-week stock market decline

will begin by mid-July at the latest.

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date |

Description |

|

Monday Jun-24 |

No important events scheduled |

|

Tuesday Jun-25 |

Case-Siller Home Price Index

Consumer Confidence

New Home Sales |

|

Wednesday Jun-26 |

Durable Goods Orders |

|

Thursday Jun-27 |

Q1 GDP (revised)

Pending

Home Sales |

|

Friday Jun-28 |

Personal Income and Spending

Chicago PMI |

Gold and the Dollar

Gold

While we were putting together last week's Interim Update the US$ gold price was

breaking out to the upside. This prompted us to write:

"Gold's

correction from its early-June high turned out to be very brief and shallow. The

gold price has now broken above multiple important resistance levels on an

intra-day basis, but the key will be how it finishes the week. A weekly close by

the August contract above $1362 would be a confirmed breakout that would point

to additional gains prior to the next multi-month peak."

As shown by

the following weekly chart, gold not only managed to end the week above $1362,

it also managed to end the week above long-term resistance in the $1370s. The

following chart also shows that gold's weekly RSI, an intermediate-term momentum

indicator, ended last week at its highest level since 2011. Although this

implies that the market is stretched to the upside and in need of a correction,

it is a sign of strength.

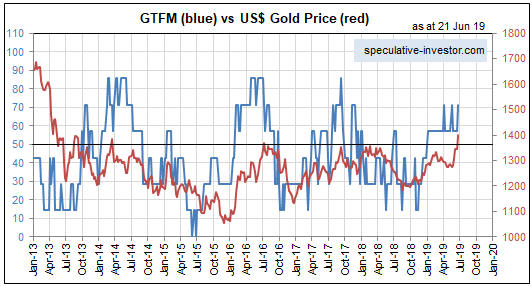

The price action is in line with the fundamentals as indicated by our Gold

True Fundamentals Model (GTFM). Refer to the following chart comparison of the

GTFM and the US$ gold price for more detail. Note that the GTFM moved a little

further into bullish territory last week due to the US dollar's downside

breakout.

Speculators have been getting more optimistic and adding to their collective

long positions in gold futures as the price has risen, but as at 18th June (the

date of the latest COT report) speculative optimism was not close to a dangerous

extreme.

With the fundamental backdrop still gold-bullish and speculative

optimism not yet at a level that warns of large downside price risk, we have no

reason to expect anything more bearish over the weeks ahead than a routine

correction that tests last week's breakout.

The one concern we have is

that part of the sharp upward move in the gold price during the second half of

last week was due to rising fear of military conflict in the Middle East. As

we've mentioned many times in the past, the idea that gold is a hedge against

military conflict is a widely-held superstition that leads to a price rise

whenever the risk of war appears to increase, but the market has NEVER sustained

such price gains and there is no good reason that it should. Therefore, whatever

proportion of last week's price gain was war-risk related will be given back

within the next few weeks.

We would be more concerned about the effect on

the gold price of war-related fear if not for the fact that the true

fundamentals (the things that really matter) have been gold-bullish all year and

became a little more so last week.

Another point is that last week's

upside breakout in the US$ gold price does not imply or confirm that gold is in

a bull market. As illustrated by the following weekly chart, the gold/SPX ratio

barely moved over the past two weeks and remains well below both its 200-week MA

and its late-December top.

It's possible that a new cyclical gold bull

market began last August, but it hasn't been confirmed yet.

Finally, this week is the final week of the month and the quarter, so the

closing prices on Friday 28th June could be critical. If gold manages to end

this week above US$1378 (the July-2016 high) it would be a breakout on the

monthly chart.

Silver

Last week the US$ gold

price broke above its July-2016 high. If silver had done the same it would now

be trading north of US$21.00/oz. Instead, although it was strong enough last

week to break above some notable resistance around $15.00, the following weekly

chart shows that the US$ silver price remains mired in a multi-year

downward-sloping 'wedge'.

The extent to which silver is lagging gold

suggests that the silver market has a lot of catching-up to do.

Silver has considerable resistance at $15.50-$16.20. Getting above this

resistance on a weekly closing basis would project a rather quick move up to

$21-$22.

Gold Stocks

GDX's daily RSI(14), a

short-term momentum indicator, hit its second-lowest level ever last August.

What this meant was outlined as follows in the 15th August 2018 Interim Update:

"Based on what tends to happen when a sell-off generates the sort of

momentum extreme achieved by the gold-mining indices and ETFs on Wednesday 15th

August, here's a likely short-term scenario for GDX:

1) A multi-week

price low within the next two weeks, probably not far below the 15th August low.

2) A sharp rebound to the 50-day MA or lateral resistance (former support)

at $21.00, whichever is the lower.

3) A decline that tests and possibly

breaches the August price low, with a positive RSI divergence.

4) A

stronger and longer rebound."

Apart from the initial rebound from

the momentum low (step 2) not reaching the 50-day MA, the pattern unfolded

exactly as described above.

When we wrote last week's Interim Update the

gold mining indices and ETFs were already short-term 'overbought'. This

suggested: "...a top that holds for at least a few weeks is close in terms

of time, but not necessarily in terms of price. If gold can hold the bulk of its

after-hours gains during Thursday's US trading session then the gold-mining

sector could make significant additional headway over the next few trading days."

In response to the upside breakout in the gold price, the gold-mining sector

moved sharply higher over the final two days of the week. As a result, GDX's

daily RSI, which hit its second-lowest level ever last August, is now at its

highest level ever. What does this tell us about the future?

Unfortunately, the price pattern following an upward momentum extreme is not as

predictable as the price pattern following a downward momentum extreme. What we

can say is that when an upward momentum extreme occurs within a few weeks of an

important bottom it usually will be followed by some consolidation, but it tends

to have BULLISH implications with regard to the ensuing 2-4 months. Also,

following a momentum extreme such as the one just achieved by GDX, a new

short-term buying opportunity is created by a correction of sufficient magnitude

or duration to test the 50-day MA or push the daily RSI(14) down to 50.

Here are some other implications of last week's moon-shot in the gold-mining

sector:

1) GDX ended last week at long-term resistance. Perhaps there

will be a spike above this resistance early in the new trading week, but this

increases the probability that a correction/consolidation will begin very soon.

2) The more short-term bullish of the two 1980s models discussed a week ago

is now the more relevant.

3) The HUI/gold ratio has blasted above its

40-day and 150-day MAs (see chart below). This is what should happen during the

first few weeks of a strong intermediate-term advance and is in stark contrast

to what happened during all other gold-mining rallies since early 2017.

As advised in last week's Interim Update, for new buying it makes more sense

to pick away at the stocks that have not moved by much from their lows --

provided that they are fundamentally sound -- than to jump into stocks that have

rallied hard already. In general, this means that new buying should be focused

on high-potential juniors that are still trading at depressed levels.

The Currency Market

The following daily chart shows that

the DX broke out to the downside from its 'rising wedge' last week. This is more

evidence that an intermediate-term downward trend is in progress. If so, the DX

will make a series of lower highs and lower lows over the coming 6-12 months.

We doubt that the DX will extend its short-term decline by more than one

point before it commences a multi-week rebound. The reason is that the currency

market is becoming a little stretched on a short-term basis. In particular, the

DX is almost 'oversold' and the currencies that have led the anti-dollar move

are now short-term 'overbought'. An example is the Swiss Franc (SF). The SF has

made a solid break above a confluence of resistance at 100-101, but a 'pause for

breath' involving a pullback to 101-101.5 to test its recent upside breakout

would be normal.

The

Australian dollar (A$) has been one of the worst-performing major currencies

over the past 12-18 months and has just tested its 10-year low. Here's the

relevant chart:

However, there is a good reason to expect that the A$ will be one of the

best-performing major currencies over the coming two years. The reason has to do

with the very strong performance over the past two years of the A$-denominated

gold price (gold/A$).

Here's a chart showing that gold/A$ has been

trending upward since mid-2017 and is now immersed in an upside blow-off (quite

possibly a trend-ending move).

Gold/A$ tends to lead A$/US$ by 2 years plus/minus 6 months. (Note: There is

a fundamental reason for the lead-lag relationship, but we won't get into that

right now.) Most recently, for example, the late-2015 bottom in gold/A$ led to

the late-2017 bottom in the A$, the mid-2016 top in gold/A$ led to the

early-2018 top in the A$, and the gold/A$ correction from mid-2016 to mid-2017

led to weakness in the A$ over the past 12 months.

The large rise in

gold/A$ since mid-2017 suggests that A$/US$ will trade a long way above its

current level in 2021, but it doesn't provide any information about the likely

short-term twists and turns.

We would take a weekly close above 71 as an

early warning signal that a multi-year A$ upward trend had begun.

Updates

on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Company

news/developments for the week ending Friday 21st June 2019:

Company

news/developments for the week ending Friday 21st June 2019:

[Note: AISC = All-In Sustaining Cost, EBITDA = Earnings Before Interest, Tax,

Depreciation and Amortisation (a measure of cash flow), EV = Enterprise Value or

Electric Vehicle, FS = Feasibility Study, FY = Financial Year, IRR = Internal

Rate of Return, ISR = In-Situ Recovery, JV = Joint Venture, MD&A = Management

Discussion and Analysis, M&I = Measured and Indicated, NAV = Net Asset Value,

NPV(X%) = Net Present Value using a discount rate of X%, NSR = Net Smelter

Return or Net Smelter Royalty, P&P = Proven and Probable, PEA = Preliminary

Economic Assessment, PFS = Pre-Feasibility Study]

*When

Golden Arrow Resources (GRG.V) published its latest quarterly report

3-4 weeks ago it was clear that the company would have to do another equity

financing very soon. A small financing (6M shares at C$0.20/share to raise

C$1.2M) was completed last week.

This financing will keep the lights on

for another month or two, but unless the company's minority-owned

Pirquitas-Chinchillas project is now cash-flow positive there will be yet

another equity financing within the coming three months.

GRG can be

likened to a long-dated out-of-the-money call option on the silver price. In the

absence of a significant silver rally, a long-dated silver call option will lose

value steadily due to a shrinking time premium and GRG shares will lose value

steadily due to a growing supply of shares. The difference is that GRG shares

don't have a fixed expiry date.

If the silver price gains a few dollars

at some point over the next several months, which is quite likely in our

opinion, then the prices of both GRG shares and long-dated silver call options

should rocket upward.

*US Gold Corp. (USAU) has

raised US$2.5M by indirectly issuing new shares at US$1.14/share (the financing

involves "Preferred Stock" exercisable into common stock). The financing also

includes share purchase warrants exercisable at US$1.14 that should bring in

another US$1.25M before year-end.

The main purpose of this financing is

to fund this year's drilling at the highly prospective, but very early stage,

Keystone gold project in Nevada.

List

of candidates for new buying

From within the ranks of TSI stock

selections the best candidates for new buying at this time, listed in

alphabetical order, are:

1) A40.AX (last Friday's closing price: A$0.15)

2) CGT.TO (last Friday's closing price: C$0.18)

3) KBLT.V at C$4.00

or lower (last Friday's closing price: C$4.13)

4) PPLT (last Friday's

closing price: US$76.46)

5) TK.V (last Friday's closing price: C$0.27)

The above list is limited to five stocks. It sometimes will contain less

than five, but it never will contain more than five regardless of how many

stocks are attractively priced for new buying.

Some

speculating ideas

1) Osisko Gold Royalties Warrants

(TSX: OR.WT). Recent price: C$0.57

Our most recent mention of

these warrants was in the 27th February 2019 Interim Update, when they were

trading at C$0.44. The price subsequently rose to the C$0.90s and then dropped

all the way back to the C$0.40s before rebounding to the mid-C$0.50s.

The

warrants have an exercise price of C$36.50, meaning that they are a very long

way out of the money (OR ended last week at C$14.78). However, they don't expire

until 18th February 2022, so there is still a lot of time for the sort of

increase in the stock price that would inject substantial value into the

warrants.

We doubt that OR will ever trade above the C$36.50 exercise

price of these warrants, but we estimate that it would take only a 30%-40% gain

in the stock price within the next 6 months -- to around C$20-$21/share -- to

generate a gain of around 200% in the warrant price.

Here's a weekly

chart of OR.TO.

2) Taseko Mines (TGB, TKO.TO). Recent price: US$0.53

TGB has 246M shares outstanding, current copper production of around 100M

pounds/year at a mine in British Columbia, an interesting development-stage

copper project in Arizona that could be put into production over the coming 12

months, and a couple of potentially-valuable exploration-stage projects. It has

been in and out of the TSI Stocks List multiple times in the past, most recently

entering the List in July-2016 at US$0.54 and exiting in January-2017 at

US$1.47.

The company has mediocre management and its balance sheet is far

from healthy (there is long-term debt of C$340M), but it does not appear to be

at risk of going broke. Importantly, the stock can be relied on to provide

substantial upside leverage during copper-price rallies and offers reasonable

liquidity.

We think that copper will perform well in US$ terms and also

outperform gold over the coming 6-12 months. If so, TGB could do extremely well

over this period -- potentially returning to the US$1.50-$2.00 area.

TGB

appears to be building a base in the US$0.45-US$0.75 range and we won't be

surprised if the base-building process continues for a few more months.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/