![]()

![]()

![]()

![]()

-- Weekly Market Update for the Week Commencing 28th October 2019

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

True

Fundamentals Summary

[Notes:

1) The date shown next to the current True Fundamentals Model (TFM) signal is

when the most recent change occurred. 2) Charts of the Gold and Equity

TFMs are included in the "Charts and Indicators" section of the TSI web

site]

| Market | True Fundamentals Model (TFM) |

| Gold (US$ Price) | Bullish (04 Oct 2019) |

| US Equity (SPX) | Bearish (04 Oct 2019) |

| Currency (Dollar Index) | Neutral (15 Mar 2019) |

| Commodities (GNX) | Bearish (01 Jun 2018) |

Last week's posts at the TSI Blog

A potential game-changer from the Fed

Summary of current

thinking/positioning

1) The Dollar Index (DX)

confirmed a short-term reversal to the downside three weeks ago and must

end a week below 96 to confirm an intermediate-term reversal to the

downside. We are anticipating such a reversal, but there remains a

(diminishing) risk that the DX will first move sharply higher for 1-3

months.

2) The US$ gold price, the US$ silver price and the

gold-mining indices are still immersed in corrections and are at risk of

experiencing sharp price declines within the next couple of weeks, but new

upward trends are expected to begin before the end of November.

3)

The Fed's new asset monetisation program has increased the risk for

bearish stock-market speculators and clear signs of equity strength have

started to emerge outside the US. However, the senior US stock indices

probably will reach short-term tops within the next two weeks and the

final few weeks of the year could involve a 'flight to safety'.

4)

The T-Bond probably will trade below its September low in the near future,

but we expect that major price weakness (yield strength) in the Treasury

market will be postponed until next year.

5) Industrial commodities

such as oil and copper could be in the process of bottoming, but we expect

that meaningful price strength won't show up until next year.

6) We

are holding a cash reserve of 25%-30%.

Interest Rates

What will the Fed do?

There is an FOMC meeting on Tuesday-Wednesday of this week, which

means that the Fed will make its next formal monetary-policy announcement

on Wednesday 30th October. What is this announcement likely to say about

interest rates?

In the minutes of the July FOMC meeting the Fed

admitted that it was taking into account market expectations regarding

rate cuts when deciding what to do. As we noted in a

blog post on 27th August, the implication of this admission is that if

the market expects the Fed to cut rates, then to avoid disappointing the

market the Fed will cut rates. In the weeks leading up to an FOMC meeting

the Fed's senior representatives have the opportunity to alter market

expectations through their regular speeches, but if we get to the week

before an FOMC meeting and the market is assigning a high probability to

an X% rate cut then an X% rate cut is almost certainly what the Fed will

deliver.

According to the

CME FedWatch Tool, at the time of writing there is a 94% probability

that the Fed Funds Rate (FFR) target range will be reduced from 175-200

basis points (bp) to 150-175bp at this week's FOMC meeting. Also, the CME

FedWatch Tool shows a 73% probability of the FFR target range being

150-175bp after the 11th December FOMC meeting. These figures imply a near

certainty of a 25bp rate cut on 30th October and a high probability that

the Fed will then be on hold for the remainder of the year.

The Fed

will cut rates by 0.25% this week, but what it does at the 11th December

meeting will be determined by what happens in the markets in the meantime.

For example, a sizable stock market decline during the weeks leading up to

the December FOMC meeting would tip the scales decisively in the direction

of another rate cut at that time.

Assuming that on Wednesday of

this week the Fed does what most market participants expect, which is cut

by 0.25% and signal that future rate cuts will depend on future data, a

big market reaction is unlikely. However, there is a risk that the main

'safe havens', meaning gold and the T-Bond, will sell off.

Lower interest rates lead to slower growth

In one

important respect, the average central banker is like the average

politician. They both tend to focus on the direct and/or short-term

effects and ignore the indirect and/or long-term effects of policies. In

the case of the politician, this is understandable if not excusable. After

all, the overriding concern of the average politician is winning the next

election. The desire to be popular also influences the decisions of

central bankers, but there is a deeper reason for the members of this

group's short-sightedness. The deeper reason is their unwavering

commitment to Keynesian economic theory.

All central bankers are

Keynesians at heart (if they weren't they wouldn't be central bankers),

and Keynesian economic theory revolves around the short-term and the

superficial. It's all about policy-makers in the government and the

central bank attempting to 'manage' the economy by stimulating demand

under some conditions and dampening demand under other conditions, with

the conditions determined by measures of current or past economic

activity. For example, if certain statistics move an arbitrary distance in

one direction then an attempt will be made to boost "aggregate demand".

That the concept of "aggregate demand" is bogus is never acknowledged,

because acknowledging that the economy comprises millions of distinct

individuals as opposed to an amorphous blob would call into question the

entire basis for central control of money and interest rates.

In

the short-term, the manipulation of money and interest rates often seems

to work. In particular, pumping money and forcing interest rates below

where they otherwise would be can lead to increased economic activity in

the form of more consumption and more investment. What's happening,

however, is that false signals are causing people to make mistakes.

One problem is that people are incentivised by cheaper credit to

consume more than they can afford, which guarantees reduced consumption in

the future. The bigger problem, though, is on the investment front, in

that projects and businesses that would not be financeable at free-market

rates of interest are made to appear economically viable. This could seem

like a very good thing for a while, but it means that a lot of resources

get used in ventures that eventually will fail. It also means that the

businesses that would have been viable in a non-manipulated rate

environment suffer profit-margin compression due to the ability, created

by the abundance of artificially-cheap credit, of relatively inefficient

and/or unprofitable competitors to remain in operation.

Thanks to

the investing errors and the general profit-margin compression that result

from it, the policy of interest-rate suppression leads to reduced economic

growth over the long term. Furthermore, it's not so much that central

bankers weigh the long-term negatives against the short-term positives and

opt for the latter; it's that their chosen theoretical framework doesn't

even allow them to consider the long-term negatives.

A final plunge in

the T-Bond?

On a short-term basis the T-Bond

and gold markets are in similar positions. Both markets reached

'overbought' extremes about two months ago and have since been in

correction mode. Also, it's likely that both markets are close to

correction lows in terms of time, but in each case there is a high risk of

a price plunge prior to a sustained turn to the upside.

The T-Bond

market is represented on the following daily chart by the iShares 20+ Year

Treasury Fund (TLT). We mentioned three weeks ago that TLT probably was

about to commence a sharp multi-week decline and we noted two weeks ago

that $130-$135 was a reasonable target for a short-term bottom. We still

have this target in mind.

We suspect that whatever additional

downside is going to materialise will do so within the next three weeks.

It's the same story with gold, because there's a good chance that concerns

about economic weakness and the trade war will soon return to

centre-stage.

The Stock Market

Stock market volatility was low

last week, but the price action was interesting nonetheless. Here are the

most significant recent developments:

1) Although the S&P500 Index

(SPX) only made a small gain last week, the upper section of the following

daily chart shows that it was enough to enable the world's most important

stock index to break above the top of its contracting triangle. The lower

section of the same chart shows that this breakout was accompanied by

impressive strength in the NYSE Advance-Decline Line (ADL).

2) Last week the Bank Index (BKX) moved above intermediate-term

lateral resistance to a new high for the year. We've been expecting this

breakout for a few months. Moreover, the BKX/SPX ratio broke the sequence

of declining tops that dates back to early 2018.

Bank stocks are

poised to perform well over the coming 12 months, both in nominal dollar

terms and relative to the broad market. Note, though, that a weekly BKX

close below 100 would invalidate last week's upside breakout.

3) Last week the NASDAQ100 Index (NDX) made a marginal new all-time

high.

4) The Dow Transportation Average (TRAN) has gone from an 8-month low

to a 5-month high in the space of only three weeks. It is now a little

stretched to the upside and less than 3% from resistance defined by this

year's high, so significant additional gains are unlikely in the

near-term.

5) The Semiconductor Index (SOX) broke above the top of the rising

'wedge' that formed over the past 6 months and ended last week at an

all-time high.

6) A week ago we wrote: "...it looks like the Emerging Markets Equity

ETF (EEM) is about to break upward from the channel in which it has traded

since April." Last week it broke above its channel top.

Last week's upside breakouts and other bullish developments were

caused at least in part by the Fed's recent introduction of a new

money-pumping program. The new program has the potential to extend the

long-term equity bull market well into next year, but there are two

reasons, one technical and the other fundamental, to believe that the

market won't make much additional headway before commencing its next

significant correction.

The technical reason is illustrated by the

following weekly chart. The chart shows that over the past 18 months the

SPX has commenced a sizable multi-week decline soon after making a new

all-time high. If the pattern continues, the SPX won't go higher than

about 3070 before reversing course.

The fundamental reason is that the so-called "Phase 1" US-China trade

deal could be in trouble. Everything was supposedly agreed and all that

was left was for presidents Trump and Xi to put pen to paper when they met

on the sidelines of the APEC Economic Leaders' Meeting in Chile in

mid-November. However, there now appears to be a difference of opinion as

to what has been agreed. In particular, the US side is saying that the

Chinese side has agreed to buy $40B-$50B per year of US agricultural

products and that existing tariffs will remain in place for now, but the

Chinese side is saying something along the lines of: "Let's go back to the

way things were in 2017. We'll buy about $20B/year of US agricultural

products and you eliminate most tariffs."

If the "Phase 1" trade

deal were to disintegrate there would, we think, be a rapid shift away

from general equities and a surge in demand for gold and T-Bonds.

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date | Description |

| Monday Oct-28 | No important events scheduled |

| Tuesday Oct-29 |

Pending Home Sales Consumer Confidence Index Case-Siller Home Price Index |

| Wednesday Oct-30 |

FOMC Statement Q3 GDP (preliminary) |

| Thursday Oct-31 |

Personal Income and Spending Chicago PMI |

| Friday Nov-01 |

Monthly Employment

Report ISM Mfg Index Construction Spending Motor Vehicle Sales |

Gold and the Dollar

The most positive recent development for the gold mining sector is the

performance of the HUI/gold ratio. As illustrated by the following chart,

HUI/gold bounced off its 150-day MA in mid-October and closed above its

40-day MA last Friday. This is a preliminary signal of an upward trend

reversal.

To solidify the reversal the HUI/gold ratio must hold

above its 40-day MA this week. By the same token, if the gold sector is

still in correction mode then HUI/gold probably will move back below its

40-day MA within the next few days.

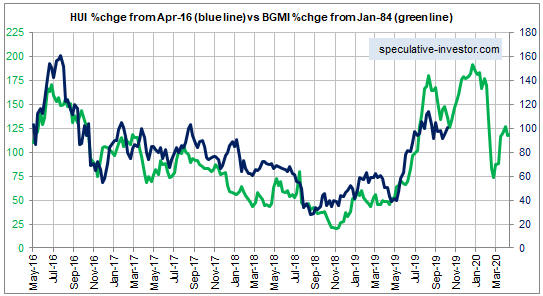

Turning to our comparison of the present-day HUI and the Barron's Gold

Mining Index (BGMI) of the 1980s, the updated chart displayed below

suggests that the correction could be complete. However, a

correction-ending plunge within the next two weeks also would be roughly

in line with this model.

The upshot is that the gold sector's short-term risk/reward is

neutral. There is still a high risk of a final correction-ending plunge

that takes GDX and the HUI down to their 200-day MAs, but we are into the

time window when the correction was/is expected to end and it wouldn't

take much additional strength from here to shift the odds in favour of a

sustainable up-turn.

The gold sector's intermediate-term

risk/reward is bullish.

The Currency Market

The following daily chart shows that the Dollar Index (DX) has been

oscillating within a channel since August of last year. The channel has an

upward slope, but, as mentioned in earlier commentaries, the choppy price

action does not have the look of an upward trend.

We think that a

1-2 year period of US$ weakness, driven by weakness in US equities

relative to European equities and the narrowing of the US-Europe

interest-rate gap, has begun or will begin within the next few months.

It's possible that there will be a US$ surge in response to fear of a

global recession prior to the start of an intermediate-term decline in the

DX, but such a surge would be short-lived because it would provoke the Fed

into becoming very 'easy' very quickly.

Last week the DX rebounded from its 200-day MA. Unfortunately, this

doesn't tell us anything useful about the future, because the rebound

could be a counter-trend move within a short-term downward trend or the

start of a larger rally.

Updates

on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() Company

news/developments for the week ending Friday 25th October 2019:

Company

news/developments for the week ending Friday 25th October 2019:

[Note: AISC = All-In Sustaining Cost, EBITDA = Earnings Before

Interest, Tax, Depreciation and Amortisation (a measure of cash flow), EV

= Enterprise Value or Electric Vehicle, FS = Feasibility Study, FY =

Financial Year, IRR = Internal Rate of Return, ISR = In-Situ Recovery, JV

= Joint Venture, MD&A = Management Discussion and Analysis, M&I = Measured

and Indicated, NAV = Net Asset Value, NPV(X%) = Net Present Value using a

discount rate of X%, NSR = Net Smelter Return or Net Smelter Royalty, P&P

= Proven and Probable, PEA = Preliminary Economic Assessment, PFS =

Pre-Feasibility Study]

*Alkane Resources (ALK.AX)

published its quarterly report for the September-2019 quarter (the first

quarter of FY2020). The report was generally positive (as discussed

below), but with one exception it contained no important new information.

The one exception is the following comment:

"A demerger and

listing of Australian Strategic Materials is under active consideration by

the Alkane Board. Consultation with regulators is underway."

In other words, the separation of ALK into two companies, one focused on

gold and the other focused on the Dubbo specialty metals project, is under

consideration. This is exactly what we have been saying the company should

do for the past two years, as it could unlock substantial value for

shareholders. Due to the opportunities to expand the gold business that

have cropped up this year, the separation makes even more sense now than

it did a year ago.

The quarterly report included another above-plan

performance from the Tomingley Gold Operation (TGO), with gold production

of 7.5K ounces at an AISC of A$1268/oz (US$862/oz). This has led to

production guidance for FY2020 (the financial year ending 30th June 2020)

being improved from 27K-32K ounces of gold at an AISC of A$1300-$1450 to

30K-35K ounces of gold at an AISC of A$1250-$1400. Note: The current A$

gold price is around $2200/oz.

The Tomingley open pit is depleted

and the current production is solely from the processing of stockpiles.

However, the life of the operation has been extended by the construction

of an underground mine that is scheduled to go into production during the

March quarter of 2020. Also, exploration results indicate the potential to

establish a new pit within a few kilometres of the existing plant.

With regard to the Dubbo specialty metals project, the commercial scale

pilot plant being constructed as part of the investment in Clean Metal

Processing Technology with Ziron Tech of South Korea is due to be

commissioned in the March quarter of 2020.

ALK's balance sheet is

strong. The company is debt free with cash, bullion plus listed

investments of about A$74M. This figure is down by about A$7M since the

end of the preceding quarter due to investments in exploration drilling,

underground mine development and the Dubbo project's pilot plant.

*Columbus Gold (CGT.TO) had noteworthy news over the past

week. First, the company announced early last week that it had raised

C$2.5M by selling 15.6M new shares to Sandstorm Gold at C$0.16/share. This

means that Sandstorm now owns about 8% of CGT. Second, late last week the

company noted conclusions from a recent government report that suggest

increasing government support for the Montagne d'Or gold project in French

Guiana. CGT's 45% stake in this project is by far its most important

asset.

Project permitting is taking longer than expected and

probably won't be complete before mid-2020. Permitting risk is probably

the main reason that CGT is trading at a small fraction of the estimated

net present value of its Montagne d'Or stake.

![]() List

of candidates for new buying

List

of candidates for new buying

From within the ranks of TSI

stock selections the best candidates for new buying at this time, listed

in alphabetical order, are:

1) AAU (last Friday's closing price:

US$0.66)

2) AOI (last Friday's closing price: C$1.18)

3)

JRV.AX, JRV.V (last Friday's closing price: A$0.21, C$0.19)

4) OIH

(last Friday's closing price: US$11.77)

5) TGB (last Friday's

closing price: US$0.44)

The above list is limited to five stocks.

It sometimes will contain less than five, but it never will contain more

than five regardless of how many stocks are attractively priced for new

buying.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/