-- Weekly Market Update for the Week Commencing 29th February 2016

Big Picture

View

Here is a summary of our big picture

view of the markets. Note that our short-term views may differ from our

big picture view.

The BULL market in US Treasury Bonds

that began in the early 1980s ended in early-2015, but there will be many years

of topping action in bond prices and bottoming action in bond yields before

major new trends get underway. (Last update: 29 June 2015)

The stock market, as represented by the S&P500 Index,

commenced

a secular BEAR market during the first quarter of 2000, where "secular

bear market" is defined as a long-term downward trend in valuations

(P/E ratios, etc.) and gold-denominated prices. This secular trend will bottom sometime between 2018 and 2020.

(Last update: 29 June 2015)

A secular BEAR market in the

US

Dollar

began during the final quarter of 2000 and ended in July of 2008. This

secular bear market will be followed by a multi-year period of range

trading.

(Last

update: 09 February 2009)

Gold commenced a

secular bull market relative to all fiat currencies, the CRB Index,

bonds and most stock market indices during 1999-2001.

This secular trend will peak sometime between 2018 and 2020.

(Last update: 29 June 2015)

Commodities,

as represented by the CRB Index, commenced a

secular BULL market in 2001 in nominal dollar terms. The first major

upward leg in this bull market ended during the first half of 2008, but

a long-term peak won't occur until 2018-2020.

(Last

update: 29 June 2015)

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Outlook Summary

Market

|

Short-Term

(1-3 month)

|

Intermediate-Term

(6-18 month)

|

Long-Term

(2-5 Year)

|

|

Gold

|

N/A |

Bullish

(26-Mar-12) |

Bullish

|

|

US$ (Dollar Index)

|

N/A |

Bullish

(29-Feb-16) |

Neutral

(19-Sep-07) |

|

US Treasury Bonds (TLT)

|

N/A |

Bearish

(19-Oct-15)

|

Bearish |

|

Stock Market

(DJW)

|

N/A |

Bearish

(30-Dec-15) |

Bearish

|

|

Gold Stocks

(HUI)

|

N/A |

Bullish

(23-Jun-10) |

Bullish

|

|

Oil |

N/A |

Neutral

(26-Oct-15) |

Bullish

|

|

Industrial Metals

(GYX)

|

N/A |

Neutral

(09-Nov-15) |

Bullish

(28-Apr-14) |

Notes:

1. Our short-term expectations are discussed in the commentaries, but except in

special circumstances we won't attempt to assign a "bullish", "bearish" or

"neutral" label to these expectations.

2. The date shown below the current outlook is when the most recent outlook change occurred.

3. "Neutral" means that we think risk and reward are roughly in balance with respect to the timeframe in question.

4. Long-term views are determined almost completely by fundamentals and intermediate-term views

are determined by a combination of fundamentals, sentiment and technicals.

Last week's posts at the TSI Blog

An oil glut doesn't preclude an oil price bottom

The "Streetlight Effect" in the gold market

It's finally time to

bet against the T-Bond

When discussing the US

government bond market in mid-January and again in early-February, we wrote:

"Although we are intermediate-term bearish on long-dated US treasury

securities, we aren't yet interested in establishing a bearish speculation. Our

reasons are 1) there's a decent chance of some additional short-term upside (in

response to stock market weakness) as part of the long-term topping pattern, 2)

the decline in the Treasury market is more likely to be a steady grind than a

plunge, and 3) there are speculative opportunities with better reward/risk

ratios."

We are now interested in establishing a bearish T-Bond speculation. The first

reason is that while there is still the risk of additional short-term upside in

the T-Bond price in response to stock market weakness, it will probably take a

lot of stock market weakness just to stop T-Bond and T-Note prices falling from

their current elevated levels. The second reason is the price action illustrated

by the following chart of the iShares 20+ Year Treasury Bond Fund (TLT).

The chart shows that TLT reversed downward after testing long-term resistance

during the first half of February and made a slightly lower high last week. We

obviously can't be sure, but this looks like a top.

If TLT has just topped, then TBT (the ProShares UltraShort 20+ Year Treasury

Fund) has just bottomed.

There are numerous ways to establish a bearish T-Bond speculation. Examples

include shorting TLT, buying TLT put options, buying TBT, and buying TBT call

options. For TSI record purposes we are choosing the most leveraged of the

aforementioned examples, meaning that we are adding a TBT call option position

to the TSI List. The selected option is the June-2016 $40 call, which ended last

week at US$1.24.

A 10% decline in TLT within the next three months would likely lift the price of

this TBT call option to around $5. As always with out-of-the-money options, the

downside risk is 100%.

Copper Update

The copper price has moved above

the top of its 10-month channel, but still needs to achieve a daily close above

lateral resistance at $2.15 to indicate that something more than a short-term

counter-trend rebound is underway. This resistance was tested last Friday.

As noted two weeks ago, the evidence that the US$ gold price made a multi-year

bottom last December is a reason to believe that a sustained upturn in the

copper price might not be far away.

The Stock Market

The US

The S&P500 Index (SPX) closed above its 50-day MA on Thursday and Friday of last

week, but hasn't quite managed to break above lateral resistance at 1950.

If/when it does, the target will be the more important lateral resistance at

1990-2000.

Our guess is that the SPX's rebound will extend, in fits and starts, to the

200-day MA (currently in the 2020s), although we'll take the evidence as it

comes and we are certainly open to other possibilities.

In assessing the market's upside potential we'll be paying close attention to

measures of market breadth such as the number of individual stocks making new

52-week highs/lows, and to sentiment indicators such as put/call ratios. For

example, near the end of a counter-trend rebound we would expect to see a

divergence between the number of individual stocks making new highs and the

senior indices, with the former not confirming the strength in the latter. We

would also expect to see a relatively high level of concern on the part of the

smart money and complacency on the part of the dumb money, which is the opposite

of what put/call ratios were revealing 2 weeks ago.

Also worth mentioning is that even though a rebound to as high as or even higher

than the 200-day MA could be on the cards, we will probably BEGIN to build a new

US stock-market bearish position if the SPX rises to the high-1900s within the

coming 2 weeks. Furthermore, although the SPX is our main index proxy for the US

stock market, our next bearish speculation -- like the ones that preceded it

over the past 8 months -- will focus on the NASDAQ100 Index (NDX). The reason is

that the NDX is where the greatest over-valuation, and hence the greatest

vulnerability, lies.

Here's a daily chart of the NDX showing lateral resistance at 4300. The 4300

level for the NDX is equivalent to the 1950 level for the SPX.

Note that if the NDX breaks above 4300, the measured objective will be the

December high of 4700. This means that a lot of technical analysts will have

4700 as a short-term target following a daily close above 4300, but it

absolutely does not mean that a break above 4300 will necessarily be followed by

a rise to as high as 4700. Markets aren't that simple.

If, like us, you plan on scaling into a bet against the NDX as the market

extends its rebound, then you could choose to short-sell QQQ (the NASDAQ100 ETF),

or buy QID (the ProShares UltraShort QQQ Fund), or buy QQQ put options, or buy

QID call options, or establish another position that rises in price when the NDX

falls in price. As usual, we will use options to place the bet in our own

account. This is because we are comfortable trading options and because options

allow us to obtain the exposure we want to a potentially large market move

without putting much money at risk (for trades such as this we prefer to risk a

100% loss on a small sum than risk a much smaller percentage loss on a much

larger sum). However, buying an inverse fund such as QID could be a more

appropriate choice for many of our readers.

We haven't yet decided on the specific option or options that we'll use for this

bearish speculation, but we are sure that the ones we end up choosing will not

expire earlier than June-2016 or later than December-2016.

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date |

Description |

| Monday

Feb 29 |

Chicago PMI

Pending Home Sales Index |

| Tuesday

Mar 01 |

Motor Vehicle Sales

ISM Mfg Index

Construction Spending |

| Wednesday

Mar 02 |

Fed's Beige Book |

| Thursday

Mar 03 |

Q4 Productivity and Costs

(revised)

ISM Non-Mfg Index

Factory Orders |

| Friday

Mar 04 |

Monthly Employment Report

International Trade Balance |

Gold and the Dollar

Gold

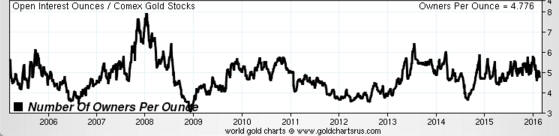

The COMEX Gold Stockpile - Fact versus Fiction

Every now and then ZeroHedge.com posts a chart showing the total Open Interest (OI)

in COMEX gold futures divided by the amount of "Registered" gold in COMEX

warehouses. Refer to the article posted

HERE for a recent example. The result of this division is supposedly the

amount of gold that could potentially be demanded for delivery versus the amount

of gold available for delivery, with extremely high numbers for the ratio

supposedly indicating that there is a high risk of a COMEX default due to

insufficient physical gold in storage. We say "supposedly", because it actually

indicates no such thing. The ratio routinely displayed by ZeroHedge -- and other

gold market 'pundits' who shall remain nameless -- is actually meaningless.

One reason it is meaningless is that the amount of gold available for delivery

is the amount of "Registered" gold PLUS the amount of "Eligible" gold, meaning

the TOTAL amount of gold at the COMEX. It is true that only Registered gold can

be delivered against a contract, but it is a quick and simple process to convert

between Eligible and Registered. In fact, much of the gold that ends up getting

delivered into contracts comes from the Eligible stockpile, with the conversion

from Eligible to Registered happening just prior to delivery.

If we look at the ratio of COMEX Open Interest to total COMEX gold inventory,

which we'll do with the aid of the following chart prepared by Nick Laird (www.sharelynx.com),

we see that it has oscillated within a 3.5-6.5 range over the past 7 years and

that nothing out of the ordinary has happened over the past three years.

Another reason that the OI/Registered ratio regularly displayed by ZeroHedge et

al is meaningless is that the total Open Interest in gold futures is NOT the

amount of gold that could potentially be demanded for delivery. The amount of

gold that could potentially be demanded for delivery is the amount of open

interest in the nearest contract. For example, when ZeroHedge posted its

dramatic "Something

Snapped At The Comex" article in late-January to supposedly make the point

that there were more than 500 ounces of gold that could potentially be called

for delivery for every available ounce of physical gold, in reality there were

about 15 ounces of physical gold in COMEX warehouses for every ounce that could

potentially have been called for delivery into the expiring (February-2016)

contract.

Although it provides no information about the ability of short sellers to

deliver against expiring futures contracts when called to do so, it is

reasonable to ask why the ratio of total OI to Registered gold has risen to such

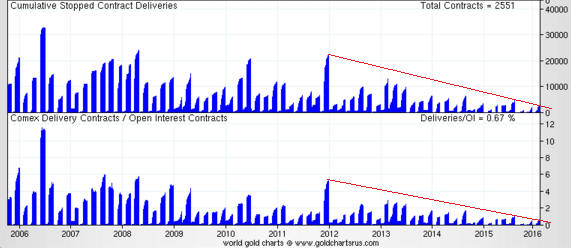

a high level. We can only guess, but we suspect that the following chart (also

from www.sharelynx.com) contains the explanation.

The chart shows the cumulative stopped contract deliveries, or the amount of

gold that was delivered into each expiring contract, in absolute terms and

relative to open interest. Notice the downward trend beginning in late-2011.

Notice also that the amount of gold delivered to futures 'longs' over the past

two years is much less in both absolute and relative terms than at any other

time over the past decade.

It is clear that as the gold price fell, the desire of futures traders to 'stop'

a contract and take delivery of physical gold also fell. In other words, the

unusually-small amount of gold maintained in the Registered category over the

past two years is probably related to the unusually-low desire on the part of

futures 'longs' to take delivery.

It's a good bet that the desire to take delivery will increase during the next

multi-year rally, prompting a larger amount of gold to be held in the Registered

category.

In conclusion, the fact is that at no time over the past several years has there

been even a small risk of a COMEX delivery default. However, this fact is

obviously not as exciting as the fiction that is regularly published by scare

mongers.

Gold and the Employment Report

At the end of this week (Friday 4th March) we get the latest edition of the US

monthly employment report. The data in this report, especially the headline jobs

growth number, can aptly be described as seasonally-adjusted noise. It's noise

because it indicates almost nothing about the current or future performance of

the economy, but it's made even less relevant as an economic indicator by

seasonal adjustment. How significant is the seasonal adjustment? Well, in

January a non-seasonally-adjusted LOSS of about 2.9 MILLION jobs became a

seasonally-adjusted GAIN of 151 thousand jobs*.

Despite its uselessness as an economic indicator, the monthly employment report

has an outsized effect on the financial markets in general and on the gold

market in particular because of this report's influence on the Fed.

The employment report's effect on the gold market tended to be negative during

2013, 2014 and the first few months of 2015, but the bias appears to have

changed. The gold price has risen on 6 of the past 11 employment-report days and

achieved a net gain of $59 over these 11 days.

That being said, we would not bet on the gold price rising in reaction to the

data to be revealed on Friday. We would also not bet on it falling, because both

the data and the market reaction to the data are too unpredictable to justify a

bet either way.

*Refer to the article at posted

HERE for details

Current situation for the US$ gold price

From last week's Interim Update:

"...a daily close below [lateral support at] $1190 would be a clear signal

that a short-term top was in place. Also, the 20-day MA has moved up to the

$1180s and will be above $1190 by the end of this week. Once it moves above

$1190 a daily close below the 20-day MA could reasonably be interpreted as

confirmation of a short-term top.

Until a short-term top is signaled via a daily close below $1190 and/or the

20-day MA there will be a realistic chance of a rise to the resistance that lies

at $1300-$1308. This resistance, in our opinion, defines the maximum

daily-closing upside potential with regard to the coming two months, although it

is likely to be breached within the coming 6 months."

By the end of last week the 20-day MA had reached $1195 and during the first

half of this week it will move above $1200, so this moving average can now be

considered the demarcation between a continuing short-term upward trend and a

significant downward correction. In other words, a daily close below the 20-day

MA would now provide the most timely confirmation that a short-term top is in

place.

As things currently stand, the price action since the 11th February peak could

reasonably be interpreted as either a consolidation within a continuing

short-term upward trend or a topping pattern (although if we had to make a guess

we'd choose the latter). This means that a move up to $1300-$1308 could still

occur prior to a short-term top.

In the absence of a dramatic catalyst, a move significantly beyond the

$1300-$1308 resistance is unlikely in the near future. The reason is that in

addition to the gold market recently becoming extremely stretched to the upside

based on measures of short-term momentum, the Commitments of Traders (COT)

situation is now bearish for gold.

Gold in terms of other currencies

Before gold can break out in terms of the strongest currency (the US$), it must

first break out in terms of the weaker currencies. Here are charts showing that

long-term breakouts have occurred in terms of some of the most important of the

weaker currencies.

The first chart shows that in Australian Dollar terms the gold price has

completed a multi-year consolidation. This chart suggests that gold/A$ will make

a new all-time high within the coming 12 months.

The second chart shows that gold/C$ (gold in Canadian Dollar terms) is in a

similar position to gold/A$.

The third chart suggests that in euro terms the gold price has either just

completed a multi-year consolidation or is close to doing so.

Silver

The following chart shows that silver reversed lower two weeks ago from the top

of a well-defined channel and fell below its 200-day MA last Friday.

Silver's problem at the moment is weak demand for the physical commodity. We

know that physical demand is weak, regardless of any anecdotal evidence to the

contrary, because it took a rise in the total speculative net-long position in

silver futures to a 7-year high just to get the price to the top of its

intermediate-term downward-sloping channel.

As explained in the past, it is normal for silver to perform worse than gold

during the first year of a cyclical gold bull market and to dramatically

outperform later in the bull market.

Gold Stocks

On Friday 26th February Goldcorp (GG) announced abysmal financial results for

2015 (including a $3.9B asset write-down) and reduced production guidance for

2016. This led to a 13% plunge in its stock price.

We suspect that the results and guidance reported by GG last Friday constitute

an attempt by the company's new CEO to 'clear the decks' and in doing so make it

easier to report better results in the future. In any case, we've thought that

GG was an over-hyped and over-valued stock for a long time. We had no interest

in owning it prior to last Friday and have no interest in owning it now.

Due to GG being one of the largest components of both the HUI and the XAU,

Friday's news from this company cast a pall over the entire gold-mining sector.

However, the gold-mining indices showed some resilience and the 'technical

damage' was minimal. At this stage, neither the HUI nor the XAU has signaled a

short-term top.

As mentioned last week, the XAU is closer than the HUI to important support and

would therefore have to fall by a lesser amount to confirm a short-term downward

reversal. For the XAU the demarcation level is lateral support at 58. A daily

close below 58 would be a clear signal that a short-term top is in pace.

An earlier, albeit less reliable, reversal signal would be a daily close below

the bottom of the 3-week channel drawn on the following chart.

Until a short-term top is signaled there will be a realistic chance that a very

'overbought' market will become even more so prior to such a top. Once a

short-term top is signaled it will be reasonable to expect a decline of

sufficient magnitude and/or time to bring about a test of the 50-day MA.

The Currency Market

Last week we wrote:

"There's a good chance that the Dollar Index will trade at least a few points

above its March-2015 peak before this year is over. The main question is: will

the start of a rally to new multi-year highs be preceded by a decline to near

the bottom of the 12-month range (the low-90s)?

Based on the recent price action the answer to the above question is: yes, it

probably will be. However, all it would take to negate the recent short-term

bearish evidence is a weekly close above 97.5.

Unless the facts change in the meantime, our intermediate-term outlook for the

Dollar Index will shift from "neutral" to "bullish" following either a decline

to the low-90s or a weekly close above 97.5."

The Dollar Index ended last week above 97.5, so our intermediate-term outlook

has shifted as noted above.

Our intermediate-term bullish outlook for the Dollar Index is based first and

foremost on relative strength in the US stock market. As illustrated by the

chart included in the 22nd February Weekly Update, the rally to new multi-year

highs in the SPX/MSWORLD ratio (US equities relative to global equities

excluding the US) projects a Dollar Index rally to new multi-year highs within

the next several months. And as illustrated by the chart displayed below, the

recent breakdown in the VGK/SPX ratio (European equities relative to US

equities) projects a euro decline to new multi-year lows. The Dollar Index is

dominated by the USD/EUR exchange rate, so a decline to new multi-year lows by

the euro would almost certainly go hand-in-hand with a rise to new multi-year

highs in the Dollar Index.

Last week's price action indicates that the Dollar Index probably made a

short-term bottom about two weeks ago and that the rally to new multi-year highs

projected by the US stock market's relative strength could be underway. However,

there is a realistic chance of at least a few more weeks of back-and-forth price

action prior to the start of a consistent upward trend in the Dollar Index.

The following chart of the Dollar Index shows a short-term price channel that is

NOT properly defined*. This channel represents a guess as to a plausible

short-term outcome. The guess is that the current multi-week rally will end at

98.5-99.0.

*A "properly defined" channel is defined by a minimum of

five points consisting of at least three points on one side and at least two

points on the other side.

Updates

on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Company

news/developments for the week ending Friday 26th February 2016:

Company

news/developments for the week ending Friday 26th February 2016:

[Note: AISC = All-In Sustaining Cost, FS = Feasibility Study, FY = Financial

Year, IRR = Internal Rate of Return, MD&A = Management Discussion and Analysis,

M&I = Measured and Indicated, NAV = Net Asset Value, NPV(X%) = Net Present Value

using a discount rate of X%, P&P = Proven and Probable, PEA = Preliminary

Economic Assessment, PFS = Pre-Feasibility Study]

*Almaden Minerals (AAU) put out a press release to report the

assay results from a single infill/metallurgical drill hole and to provide a

general corporate update. This is the sort of press release that junior mining

companies sometimes issue for the primary purpose of reminding the investing

community of the company's existence. In this case the message was: "Hey, gold

stock investors and analysts, don't forget about us -- we are ploughing ahead

with the development of a potentially-economic gold deposit in a decent

location."

*Evolution Mining (EVN.AX) advised that it has increased the size

of its gold forward-sales (hedge) book by 150K ounces -- from 688K to 838K

ounces. The additional forward sales were done at an average of A$1764/oz,

taking the overall average up from A$1588 to A$1619/oz.

The 838K ounces of forward sales is spread over four years. Given that EVN is

expected to have annual production of more than 800K ounces/year over this

period, the hedging covers about 25% of production. This is OK, but we wouldn't

like it if the company significantly increased its hedging beyond the current

level. Neither, we suspect, would 'the market', in that the main reason to own a

gold-mining stock is to obtain leveraged exposure to upside in the gold price.

*Ivanhoe Mines (IVN.TO) announced the results of the PFS for its

Kamoa copper project in the DRC (Democratic Republic of the Congo). Kamoa is a

joint venture between IVN and Zijin Mining. From our perspective the PFS results

were unsurprising and slightly positive.

The PFS covers the first phase of a planned 2-phase development at Kamoa. The

first phase involves spending US$1.2B to build a mine with average annual copper

production of about 200M pounds. The plan is to use the cash generated by the

first phase to eventually expand production to about 600M pounds per year.

According to the PFS, the first phase would be economically viable at a copper

price of US$3.00/pound, economically marginal at a copper price of

US$2.50/pound, and definitely not viable at the current copper price.

Specifically, the NPV(8%) and IRR would be US$986M and 17.2% at $3.00/pound and

$336M and 11.5% at $2.50/pound. This suggests that Kamoa will likely proceed to

mine construction when it looks like the copper price has made a sustained move

above $3/pound. We expect to see the copper price above $3/pound next year, but

not this year.

By the way, the discount rate used to calculate net present value (NPV) can have

a big effect on the result. IVN used an 8% discount rate for its base-case

calculations, which is reasonable without being conservative, whereas

gold-mining juniors typically use a far more aggressive 5% discount rate. If IVN

had used a 5% discount rate then its calculated NPV at $3/pound would be $1732M

instead of $986M. In other words, in this case a decrease of only 3% in the

assumed discount rate results in an increase of almost 100% in the calculated

NPV.

Based on current metal prices and what's currently known about project

resources/economics, from most to least valuable we rank IVN's projects as

follows:

1. Kipushi zinc project (DRC)

2. Kamoa copper project (DRC)

3. Platreef PGM project (SA)

The main reason we like the stock is that 'the market' is presently assigning no

value to any of these projects, given that IVN is trading well below its working

capital.

*Pilot Gold (PLG.TO): In discussing PLG's latest quarterly

financial statements last November, we had this to say: "The most important

number for an exploration-stage mining company is the working capital, which in

PLG's case was US$10.2M (C$13.6M) at 30th September (down from US$12.7M at 30th

June). At the current rate of spending this would be enough to fund the company

for 9-12 months, although we suspect that PLG's management will look for an

opportunity to top-up the treasury within the next 4 months."

It therefore didn't come as a surprise to us when PLG announced a relatively

small (C$4.45M) equity financing last week.

The new shares are unfortunately being issued at a price of only C$0.25 and each

new share comes with half of a 2-year C$0.40 warrant. This means that the new

shares are being issued at an all-time low price, resulting in significant

per-share value dilution. Surprisingly, however, the stock price reacted to the

financing news by rising sharply on heavy volume. This could possibly be

explained by the removal of the short-term financing uncertainty (sell the

rumour, buy the news) and PLG 'playing catch-up', but, as we said, it was a

surprising reaction.

PLG also announced that Cal Everett has been appointed president and chief

executive officer of the company. Mr. Everett has the right type and amount of

experience for the job.

The main concern/risk with PLG is that it hasn't yet discovered an economic gold

deposit. PLG has generated encouraging and in some cases spectacular drilling

results across multiple projects over the past couple of years, but is yet to

define a resource that stands a good chance of being developed into a mine. It

is therefore more of a play on future exploration success than on the gold

price, although pure exploration plays often start to become popular after a

gold rally has been in progress for a few months.

*Pretium Resources (PVG): A week ago we wrote: "Taking into

account the revised capex estimate and the amount of working capital that will

be needed between now and when the mine is expected to become cash-flow

positive, PVG will need to raise about US$100M. This will most likely happen via

an equity financing. Furthermore, although PVG probably won't need to raise the

additional money until next year, it's possible that the recent relative

sluggishness of PVG's share price is at least partly due to anticipation of a

sizable equity financing happening in the near future."

It turned out that 'the market' was correctly anticipating a sizable equity

financing. About 48 hours after we published the above comment, PVG announced

that it was issuing 26M new shares at US$4.58/share to raise US$120M. The

financing price represents a discount of about 10% to the market price prior to

the announcement.

In our estimate of PVG's fair value included in the 22nd February Weekly Update

we assumed that the company would issue 20M new shares. It is actually issuing

26M new shares, but this doesn't alter our view that fair value is US$5.50-$6.00

at the current gold price.

PVG could again be a good candidate for new buying after this equity financing

is put to bed and the gold-mining indices pull back to near their 50-day MAs.

List

of candidates for new buying

From within the ranks of TSI stock selections the best candidates for new buying

at this time, listed in alphabetical order, are:

1) FCG (last Friday's closing price: US$3.41)

2) IVN.TO (last Friday's closing price: C$0.68)

3) PRQ.TO (last Friday's closing price: C$2.85)

Note that the above list is limited to five stocks. It will sometimes contain

less than five, but it will never contain more than five regardless of how many

stocks are attractively priced for new buying.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html