--

Weekly Market Update for the Week Commencing

30th January 2017

Big Picture

View

Here is a summary of our big picture

view of the markets. Note that our short-term views may differ from our

big picture view.

The BULL market in US Treasury Bonds

that began in the early 1980s ended in early-2015, but there will be many years

of topping action in bond prices and bottoming action in bond yields before

major new trends get underway. (Last update: 29 June 2015)

The stock market, as represented by the S&P500 Index,

commenced

a secular BEAR market during the first quarter of 2000, where "secular

bear market" is defined as a long-term downward trend in valuations

(P/E ratios, etc.) and gold-denominated prices. This secular trend will bottom sometime between 2018 and 2020.

(Last update: 29 June 2015)

A secular BEAR market in the

US

Dollar

began during the final quarter of 2000 and ended in July of 2008. This

secular bear market will be followed by a multi-year period of range

trading.

(Last

update: 09 February 2009)

Gold commenced a

secular bull market relative to all fiat currencies, the CRB Index,

bonds and most stock market indices during 1999-2001.

This secular trend will peak sometime between 2018 and 2020.

(Last update: 29 June 2015)

Commodities,

as represented by the CRB Index, commenced a

secular BULL market in 2001 in nominal dollar terms. The first major

upward leg in this bull market ended during the first half of 2008, but

a long-term peak won't occur until 2018-2020.

(Last

update: 29 June 2015)

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Outlook Summary

Market

|

Short-Term

(1-3 month)

|

Intermediate-Term

(6-18 month)

|

Long-Term

(2-5 Year)

|

|

Gold

|

N/A |

Neutral

(21-Nov-16) |

Bullish

|

|

US$ (Dollar Index)

|

N/A |

Neutral

(17-Aug-16) |

Neutral

(19-Sep-07) |

|

US Treasury Bonds (TLT)

|

N/A |

Neutral

(21-Nov-16)

|

Bearish |

|

Stock Market (DJW)

|

N/A |

Neutral

(14-Nov-16) |

Bearish |

|

Gold Stocks

(HUI)

|

N/A |

Neutral

(21-Nov-16) |

Bullish

|

|

Oil |

N/A |

Neutral

(26-Oct-15) |

Bullish

|

|

Industrial Metals

(GYX)

|

N/A |

Neutral

(10-Oct-16) |

Bullish |

Notes:

1. Our short-term expectations are discussed in the commentaries, but except in

special circumstances we won't attempt to assign a "bullish", "bearish" or

"neutral" label to these expectations.

2. The date shown below the current outlook is when the most recent outlook change occurred.

3. "Neutral" means that we think risk and reward are roughly in balance with respect to the timeframe in question.

4. Long-term views are determined almost completely by fundamentals and intermediate-term views

are determined by a combination of fundamentals, sentiment and technicals.

Last week's posts at the TSI Blog

Casey's Financial Chaos Prediction

Gold

and the US Constitution

Summary of current

thinking/positioning

1) Thinking that the rebounds in

gold, silver and the associated mining indices are not yet close to being

over.

2) Expecting intermediate-term tops in non-gold commodities

and the associated equities later this quarter. Looking for profit-taking

opportunities, but planning to maintain some long-term exposure. Hedged

via EEM and USO put options.

3) Thinking that the US Treasury Bond

has significant additional short-term upside (within a long-term bearish

trend).

4) Expecting an extension of the US equity bull market and

expecting a generally-bullish global equity trend. Concerned about

short-term downside risk, but acknowledge that a significant correction

might not begin before March.

5) Thinking that the Dollar Index is

immersed in a 2-3 month correction, after which its longer-term upward

trend will resume.

6) Maintaining a large cash reserve to hedge

downside risk in equities (current cash percentage is about 35%).

Loosening is the

new tightening

The Fed meets to discuss its

monetary policy this week. There is almost no chance that an outcome of

this meeting will be another boost in the Fed Funds Rate (FFR), but

there's a decent chance that the next official rate hike will be announced

in March. Regardless of when it happens and regardless of how it is

portrayed in the press, the next Fed rate hike, like the two before it,

will NOT imply a tightening of US monetary policy/conditions.

The

two-part explanation for why hikes in the FFR no longer imply the

tightening of monetary policy has been discussed many times in TSI

commentaries over the past few years and was also addressed in a

March-2015 post at the TSI Blog titled "Tightening

without tightening". The first part of the explanation is that with

the US banking system inundated with excess reserves there is no longer an

active overnight lending market for Federal Funds (banks never have to

borrow Federal Funds anymore because they have far more than they

require). In other words, when the Fed hikes the FFR it is hiking an

interest rate that no one uses.

The second and more important part

of the explanation is that Fed rate hikes are now implemented by

increasing the interest rate PAID by the Fed on bank reserves. That is,

Fed rate hikes are now implemented not by charging the banks a higher rate

of interest but by paying the banks a higher rate of interest. To put it

another way, whereas in the "good old days" rate hikes were implemented by

removing reserves from the banking system, the Fed now implements rate

hikes by injecting reserves -- in the form of interest payments -- into

the banking system.

So, what's widely known as monetary tightening

is now a Federal Reserve action that actually has the effect of LOOSENING

monetary conditions.

Orwell's "1984" had the slogans "War is

Peace", "Freedom is Slavery" and "Ignorance is Strength". Thanks to the

Fed we can now add "Loosening is Tightening".

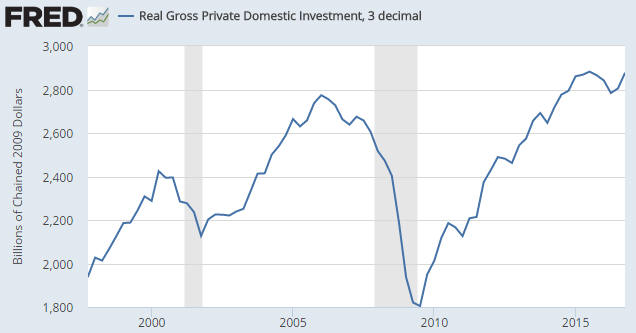

US Recession

Watch

Our most recent "US Recession

Watch" was in the 4th January Interim Update, at which time we concluded:

"The message of the ISM Manufacturing NOI [New Orders Index], the

most reliable short-term recession indicator, is that a US recession will

not begin EARLIER than the second quarter of 2017. At the same time, the

message of Real Gross Private Domestic Investment (RGPDI), the most

reliable long-term indicator of US recession, is that a US recession will

not begin LATER than the second quarter of this year.

The combined

message of the two indicators could therefore be interpreted as: a

recession should begin during the second quarter of this year. However, we

aren't confident that this is the correct interpretation. The reason is

that due to the extraordinary interventions on the monetary front and the

likelihood that -- for the first time ever, as far as we can tell --

"fiscal stimulus" will be implemented in the US with the economy in the

late stages of an expansion, the time from a downward reversal in RGPDI to

the start of a recession could be longer during the current cycle than

during any previous cycle."

A new quarterly RGPDI number was

released on Friday 27th January and revealed a significant increase in

Q4-2016. Due to this increase, RGPDI is within spitting distance of its

Q3-2015 peak.

We've been operating under the assumption that RGPDI's Q3-2015 peak

was the cyclical kind (the final high prior to the start of a major

decline), but the rebound over the past two quarters to the vicinity of

the high indicates that this assumption is probably wrong. If the

assumption is wrong and RGPDI is yet to reach its high for the cycle then

the next US recession probably won't begin until 2018.

The revised

message from RGPDI fits better than the previous message with most of our

current financial-market expectations and assessments. For one example, we

expect that 2017 will turn out to be a good year for industrial

commodities and a generally bullish year for global equities, but it's

difficult to imagine how this could happen if a US recession were to begin

by the middle of the year. For another example, the likelihood that the US

economy is still at least a few quarters away from the start of a

recession is consistent with our assessment that the fundamental backdrop

remains bearish for the world's premier counter-cyclical investment (gold).

Copper Update

The copper price remained below

its November high last week, meaning that it didn't break out to the

upside. It also remained above its 50-day MA, meaning that the potential

for an upside breakout and a quick rise to around $3.00 is intact.

The Stock Market

The US

Last week's upside breakouts by the S&P500 Index (SPX) and the Dow

Industrials Index established the first significant bearish divergence

between the senior US stock indices and stock-market internals since 2015.

The bearish divergence is illustrated by the following chart, the top

section of which shows the SPX and the bottom section of which shows the

UWSPX/SPX ratio (the unweighted SPX divided by the normal

market-cap-weighted SPX). The UWSPX/SPX ratio generally turns down well

before major and intermediate-term tops, warning that the rally is

becoming narrower. For example, notice that it turned down about 3.5

months prior to the intermediate-term top of July-2015.

As a result

of last week's price action we now have a divergence of almost two months,

in that the UWSPX/SPX ratio peaked in early-December and remains well

below this peak despite the new high achieved by the SPX last week.

If market internals continue to diverge bearishly from the senior

indices then an intermediate-term top (a top that holds for at least 6

months) will probably be put in place later this quarter.

A likely

news-related 'excuse' for an intermediate-term decline from a Q1-2017 peak

is the looming political battle over the US government's debt ceiling. The

current debt limit expires in mid-March and will have to be raised to

enable the government to continue its borrowing. It will be raised, but

months of Congressional wrangling over the issue could be the story that

justifies, in the mainstream financial press and the minds of many

traders, months of weakness in the stock market.

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date |

Description |

|

Monday January 30 |

Personal Income and Spending

Pending Home Sales Index |

| Tuesday

January 31 |

Employment Cost Index

Chicago PMI

Consumer Confidence |

|

Wednesday February 01 |

Motor Vehicel Sales

ISM Mfg Index

Construction Spending

FOMC

Announcement |

|

Thursday February 02 |

Q4 Productivity and Costs

(prelim) |

|

Friday February 03 |

Monthly Employment

Report

ISM Non-Mfg Index

Factory Orders |

Gold and the Dollar

Gold

The

US$ gold price reached its 50-day MA on Friday and then bounced. This means that

the decline has now gone as far as it should go IF, as we currently think is

most likely, the market is experiencing a routine correction prior to resuming

its short-term upward trend. However, with the fundamental backdrop

gold-bearish, as evidenced in part by the current enthusiasm for pro-cyclical

speculations such as copper, oil and the broad stock market, we certainly can't

rule out the possibility of a larger pullback in the gold price.

A solid

daily close below the 50-day MA would change the anticipated pattern/roadmap.

Such an event would suggest that the initial rebound from the December-2016 low

had ended sooner than expected and that a test of the December low was on the

cards, but could also lead to an extension of the overall rebound. We will deal

with the possibility of a longer rebound involving a test of the December-2016

low if the 50-day MA is solidly breached.

The Fed's actions naturally affect the gold market. The FOMC Announcement

scheduled for this Wednesday (1st February) could therefore be a market-moving

event, although it probably won't be.

The US$ gold price has risen on 11

of the past 13 FOMC Announcement days, but if it rises on Wednesday it probably

won't be due to anything the Fed does or says. The reason is that the Fed will

almost certainly do what almost everyone expects, which is make no change to its

targeted interest rate and make no significant change to the wording of its

policy statement.

Silver

Silver is in a similar

position to gold, in that it bounced off its 50-day MA on Friday. However, on a

very short-term basis the silver chart looks more bullish than the gold chart,

the reasons being that silver has now completed three successful tests of its

50-day MA and Friday's reversal was stronger in the silver market than in the

gold market (Friday was an "outside-up" day in the silver market).

The

Silver price has short-term upside potential to $18-$19.

Gold Stocks

The gold-mining sector remains in

consolidation mode, which is where it has been since 5th January. It is getting

helped to some extent by the strength in the industrial-metals-mining sector,

but at the same time the enthusiasm for gold-related investments is being

dampened by rising economic confidence.

There's no reason to favour gold

stocks over stocks in general and other commodity stocks in particular if the

pace of real economic growth is about to increase. The pace of real economic

growth is probably not actually about to increase, but financial-market price

trends are driven by perception and perception regularly deviates from reality.

We continue to have 220-250 in mind as a target for the HUI's rebound from

its December low. The upper end of this range will be achievable during Q1-2017

as long as the gold price holds above its 50-day MA.

The

first clear-cut evidence that the gold-mining consolidation is over will

probably be provided by GDXJ. This is due to GDXJ's numerous tests of its

200-day MA (the red line on the following chart). A daily close above this MA

would signal the resumption of the gold sector's short-term upward trend.

The Currency Market

The euro reached resistance near

108 last Monday and then pulled back. It could do what the gold and silver

markets have just done and drop back to its 50-day MA. That would be a routine

correction to a short-term upward trend, whereas a decline to below this MA

would suggest that the short-term rebound was over and the longer-term downward

trend had resumed.

The most we are expecting from the euro's rebound is a

test of intermediate-term resistance near 109.5.

The following chart compares the euro (the blue line) with the difference

between German and US 10-year government bond yields.

It is clear that

there has been a positive correlation over the 2-year period covered by the

chart and that the positive correlation has been very strong over the past 6

months. That is, recently the euro has consistently strengthened against the US$

when German 10-year interest rates have risen relative to US 10-year interest

rates and weakened against the US$ when the interest-rate differential has moved

in the other direction.

Prior to the past 2 years there were some large divergences between the

euro/US$ exchange rate and the interest-rate differential shown in the above

chart. Also, as an indicator of the euro/US$ exchange rate, relative

equity-market performance has a much better long-term track record than the

interest-rate differential. However, for some reason the interest-rate

differential has recently exerted more influence than usual.

We are

mentioning the relationship depicted above as something to watch, but at this

stage it is not giving us any clues about the future performance of the euro.

The reason is that we don't have an opinion on whether 10-year German interest

rates will rise or fall relative to 10-year US interest rates over the months

ahead. The fact that the ECB is still aggressively monetising bonds while the

Fed takes some tentative steps towards 'policy normalisation' suggests that

German bond yields are more likely to fall than rise relative to US bond yields,

but on the other hand German bond yields are starting at much lower levels than

US bond yields in both nominal and real terms.

Updates

on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Company

news/developments for the week ending Friday 29th January 2017:

Company

news/developments for the week ending Friday 29th January 2017:

[Note: AISC = All-In Sustaining Cost, FS = Feasibility Study, FY = Financial

Year, IRR = Internal Rate of Return, ISR = In-Situ Recovery, MD&A = Management

Discussion and Analysis, M&I = Measured and Indicated, NAV = Net Asset Value,

NPV(X%) = Net Present Value using a discount rate of X%, P&P = Proven and

Probable, PEA = Preliminary Economic Assessment, PFS = Pre-Feasibility Study]

*Blackham Resources (BLK.AX) published a revised

resource estimate for the Matilda/Wiluna gold project in Western Australia in

December. At that time, 900K ounces were added to the project's estimated global

resource. Specifically, the combined Matilda/Wiluna Measured, Indicated and

Inferred Mineral Resource grew to 6.0Moz (58Mt at 3.2g/t) from 5.1Moz, with

about 2.1M ounces of the new total being open-pit resources.

Another

revision to the resource estimate was published last week. The result is that

the project's estimated global resource has grown by an additional 400K ounces

-- to 6.4Moz (63Mt at 3.2g/t), including about 2.4M ounces of open-pit

resources. In other words, BLK has increased its estimated gold resource by 1.3M

ounces (about 25%) over the past 2 months.

These revised estimates are

part of the Stage 2 expansion study aimed at growing annual gold production to

200K ounces from this year's target of 100K ounces.

There was no market

reaction to BLK's mid-December announcement of an additional 900K ounces of

in-ground resources. There was, however, a meaningful positive reaction to last

week's news of a 400K-ounce resource addition, with the stock rising quickly to

A$0.80 before dropping back to the A$0.60s in sympathy with the sector-wide

correction.

This indicates that gold-sector sentiment is continuing to

cycle from depression to exuberance and back again. The market environment for

gold-mining stocks swung from depressed during the second half of 2015 (a period

when the market mostly ignored genuinely good news from gold-mining companies)

to exuberant during the second and third quarters of 2016 (when gold-mining

stocks rallied strongly in reaction to almost any news, regardless of its

significance) to depressed during November-December of 2016 (when genuinely good

news was again being mostly ignored). It now appears to be on its way back to

exuberant, although it still has a long way to go.

Obviously, most buying

should be done during the periods when sentiment is depressed and most selling

should be done during the periods when sentiment is exuberant.

*Evolution

Mining (EVN.AX) issued its quarterly report for the December quarter.

The results were good, but not surprising.

Gold production during the

quarter was 218K ounces at an AISC of only A$900 (US$675) per ounce. This puts

EVN on track to do a little better than its FY2017 guidance of 800K-860K ounces

at an AISC of A$900-$960/oz. Net debt at 31st December was apparently A$588M,

which is roughly in line with our expectations and not a problem for a company

with $100M+/quarter of positive cash flow.

As far as we know, EVN has

the lowest production cost of any mid-tier or major gold producer. It also has

the lowest geopolitical risk profile of any mid-tier or major gold producer. Its

shares should therefore be assigned a valuation premium, but if anything they

trade at a discount.

*Petrus Resources (PRQ.TO) provided

production guidance for 2017. The capital budget for the year is C$50M-$60M

(oil-and-gas production is a capital-intensive business), which will be funded

from cash flow, working capital and existing credit facilities. The plan is for

this money to fund the drilling of 16 new wells.

The production rate in

December was about 8,500 boe/d (barrels of oil equivalent per day). The company

has a base decline rate of 28%, which means that if it drilled no new wells its

production rate would decline to about 6,100 boe/d by December of this year.

However, due to this year's drilling the production rate is expected to rise to

the 9,600-10,200 range by year-end 2017.

*Sprott Resource

Corp. (SCP.TO) and Adriana Resources (ADI.V)

shareholders have given their respective approvals to the merging of the two

companies. The merger is now expected to be finalised on or shortly after 9th

February, at which time the name of the combined company will be Sprott Resource

Holdings.

List

of candidates for new buying

From within the ranks of TSI stock

selections the best candidates for new buying at this time, listed in

alphabetical order, are:

1) AAU at around US$0.90 (last Friday's closing

price: US$1.03)

2) ALK.AX at A$0.35 or lower (last Friday's closing

price: A$0.37)

3) BLK.AX (last Friday's closing price: A$0.665)

4)

PRQ.TO in the low-C$2.70s (last Friday's closing price: C$2.95)

5) SCP.TO

(last Friday's closing price: C$0.57) or ADI.V (last Friday's closing price:

C$0.19)

The above list is limited to five stocks. It will sometimes

contain less than five, but it will never contain more than five regardless of

how many stocks are attractively priced for new buying.

Speculative

exposure to fertiliser

Due to last week's news it's worth

revisiting Focus Ventures (FCV.V), a tiny company that owns the large Bayovar

phosphate (fertiliser) project in northern Peru. Based on the updated PFS

completed in Q2-2016, this project is estimated to have an after-tax NPV(7.5%)

of US$458M.

FCV is a member of the

TSI Small

Stocks Watch List, which means that we think it has speculative merit but

that it is too small/risky/illiquid to be in the TSI Stocks List.

Here's

what we wrote about FCV in the 2nd November 2016 Interim Update, at which time

it was trading at C$0.065:

"For there to be a large increase in FCV's

stock price, one of two things will have to happen. The company will have to

attract a JV partner of sufficient size and financial resources to fund the

development of the project or there will have to be a substantial rise in the

speculative enthusiasm for fertiliser-related equities. Currently, there is

almost no interest in such stocks.

Also worth mentioning is that FCV has

about C$1.1M of short-term liabilities and only about $0.6M of cash, so unless

it attracts a financially-strong JV partner in the near future it will have to

do another dilutive equity financing.

With a market cap of less than

US$7M and 100% ownership of a project with a US$458M NPV, FCV has massive upside

potential. However, in the absence of unexpected news the stock probably won't

do much over the next few months and could soon be weighed down by an equity

financing."

The expected equity financing was announced last week.

The company is raising C$4M by issuing 80M new shares at C$0.05/share and in

doing so is increasing its total share count to about 212M. Although this

dilutes the per-share value, it removes a short-term risk and allows the company

to move forward.

More significantly, in the

press release

that announced the equity financing the company also announced the hiring of a

new president.

The new president (Gordon Tainton) has an excellent C.V.,

including decades of experience in senior management roles in the fertiliser

industry. He should have the contacts and knowledge needed to negotiate the JV

deal that would make FCV a far more valuable company, and the fact that he has

accepted the position with FCV is a stamp of approval for the Bayovar project.

A final relevant point is that fertiliser stocks are beginning to garner

some interest as part of the general rise in the enthusiasm for

commodity-related investments. This is evidenced by the following chart of

Potash Corp. (POT), one of the world's largest producers of potash. It looks

like POT has completed a long-term base.

Buying POT shares would be a relatively low-risk way of obtaining exposure to

fertiliser, especially if the shares are bought with the price near the top of

the base (US$18.00). FCV is more of a Vegas-style gamble, but with better odds

for the punters.

FCV is an interesting speculation near its financing

price of C$0.05.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://research.stlouisfed.org/