![]()

![]()

![]()

![]()

-- Weekly Market Update for the Week Commencing 30th December 2019

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

True

Fundamentals Summary

[Notes:

1) The date shown next to the current True Fundamentals Model (TFM) signal is

when the most recent change occurred. 2) Charts of the Gold and Equity

TFMs are included in the "Charts and Indicators" section of the TSI web

site]

| Market | True Fundamentals Model (TFM) |

| Gold (US$ Price) | Bullish (27 Dec 2019) |

| US Equity (SPX) | Bullish (20 Dec 2019) |

| Currency (Dollar Index) | Neutral (15 Mar 2019) |

| Commodities (GNX) | Bearish (01 Jun 2018) |

Last week's posts at the TSI Blog

Accelerating Monetary Inflation

Summary of current

thinking/positioning

1) The Dollar Index (DX) remains

range-bound, needing a weekly close below 96.5 to signal an

intermediate-term reversal to the downside or a weekly close above 99.5 to

signal an intermediate-term rally. We are anticipating the former, but we

are uncertain as to whether it will happen in the near future or during

the first few months of next year.

2) Last week the conflict

between the gold bullion market and the gold mining sector was resolved by

the bullion market confirming the gold sector's bullish price action. We

expect a multi-month top in January.

3) The senior US stock

indices probably will make multi-month tops between late-December and

mid-January. Sentiment indicators are flashing warning signs, but breadth

indicators are saying that the coming decline will be limited to around

10%.

4) The T-Bond made a short-term bottom in early-November, but

there is still risk of downward acceleration over the coming month or two.

Regardless of what happens in the short-term, there's a good chance that

major price weakness will be seen in 2020. In other words, it looks like

higher interest rates are on the way.

5) Industrial commodities

such as oil and copper should perform well over the next 12 months, but

the stage is set for multi-month price highs early in the New Year.

6) We are holding a cash reserve of 25%-30% and are looking for

opportunities to increase this reserve.

The Fed

The Fed's interest rate

manipulations

According to the prices of Fed Funds Futures

contracts, the majority view right now is that the Fed will make no change

to its interest rate target in 2020. This means that the market currently

is in synch with Jerome Powell's characterisation of 2019's three rate

cuts as a mid-cycle correction along similar lines to the mid-cycle

corrections that happened during the economic expansion of the 1990s.

Consequently, a rate cut in 2020 would be a major event in that it would

change the way that 2019's rate cuts are perceived.

To further

explain, one more rate cut would indicate that the Fed's actions during

July-October of 2019 marked the start of a 'loosening' cycle as opposed to

a correction within a 'tightening' cycle. This shift in perception would

have big implications for all the financial markets and especially the

currency market. Specifically, it would lead to very significant weakness

in the US dollar.

A catalyst for the Fed's next rate cut could

arrive during the first quarter of 2020 in the form of a 10% decline in

the S&P500 Index. While an SPX decline of this magnitude initially could

boost the US$ and put irresistible downward pressure on the prices of

almost all equities, the Fed's reaction probably would set in motion an

intermediate-term rally in the commodity sector and an upward trend in

inflation expectations.

Monetising the government deficit

A number of temporary factors came together during September to create

the "repo crisis", but the underlying issue (the root cause) was not

temporary. That's why the Fed felt the need to continue pumping money and

reserves into the banking system after the initial crisis subsided and

order was restored. The underlying issue is that the demand for the US

Federal Government's debt is falling short of supply at current interest

rates.

The Primary Dealers (PDs) are intermediaries in the

Treasury market. When the Fed conducts its open market operations it deals

through the PDs. For example, when the Fed wants to inject money into the

banking system it buys Treasury securities from the PDs. Also, the PDs are

obligated to place bids at the regular auctions of US government debt and

they do this with the aim of quickly selling the debt at a profit. The Fed

is a potential buyer of this debt.

Prior to mid-September the Fed

was not doing any net buying of Treasuries, so Treasury debt purchased by

the PDs at government debt auctions had to be sold to hedge funds, bond

funds, pension funds, foreign central banks, etc. However, there wasn't

sufficient demand at high-enough prices (low-enough yields) to enable the

PDs to earn the desired profit, so they ended up with a much

larger-than-normal amount of unsold Treasury inventory.

A knock-on

effect was that the PDs, most of which are banks, had less ability than

normal to offer short-term money to the "repo" market. At the same time,

the demand from hedge funds for short-term money was ramping up.

During September, the elevated demand for short-term funding on the part

of hedge funds and the reduced supply of short-term funding from PDs and

the associated major banks collided with a substantial build-up of cash in

the government's account at the Fed and a corporate tax payment. The

result was a dramatic spike in the cost of short-term funding (a dramatic

interest-rate spike) that the Fed addressed by providing the "repo market"

with whatever additional 'liquidity' it needed.

By aggressively

pumping money the Fed was able to bring the cost of short-term funding

back into line with its target, but, as mentioned above, the underlying

issue of excess Treasury supply remained. This meant that the Fed couldn't

just switch on the money pumps for a short period and then turn them off.

It had to keep pumping because the government kept emitting new debt at a

rapid pace.

It's beginning to look as if the non-Fed demand for

Treasury securities will continue to fall short of Treasury supply at the

Fed's desired interest rates until/unless there is a financial shock of

sufficient magnitude to provoke a large-scale flight to safety. In other

words, in the absence of a widespread shift away from risk it seems that

the Fed will have to keep filling-in the gap between Treasury supply and

Treasury demand with its own buying of Treasury debt. This means that for

all intents and purposes, the Fed is now monetising the government

deficit.

In the 21st October Weekly Update we explained why this is

potentially very important. At that time we wrote:

"The Fed has

emphasised that the new asset monetisation program should not be called

"QE" because it does not constitute a shift in monetary policy.

Technically this is correct, but in a way it's worse than a shift towards

easier monetary policy. The Fed's new program is actually a

thinly-disguised attempt to help the Primary Dealers absorb an increasing

supply of US Treasury debt. To put it another way, the Fed is now

monetising assets for the purpose of financing the US federal government,

albeit in a surreptitious manner."

And:

"...when

the central bank is perceived to be financing the government, as opposed

to implementing monetary policy to achieve economic (non-political)

objectives such as "price stability", there is a heightened risk that a

large decline in monetary confidence will be set in motion. One effect of

this would be an increase in what most people think of as "inflation"."

As well as leading to an increase in what most people think of as

"inflation", the spreading realisation that the Fed is monetising assets

for the express purpose of financing the US federal government should lead

to weakness in the US dollar on the foreign exchange market.

Oil

Flawed Forecasts

Most forecasts are extrapolations of the recent past and as a result

will be wildly inaccurate around major turning points or trend

accelerations. The forecasts made by the U.S. Energy Information

Administration (EIA) a decade ago are great examples, in that there are

big differences between the actual US energy situation today and what the

EIA projected 10 years ago. Some of the most important differences are

illustrated in the following charts, which were taken from the article

posted

HERE.

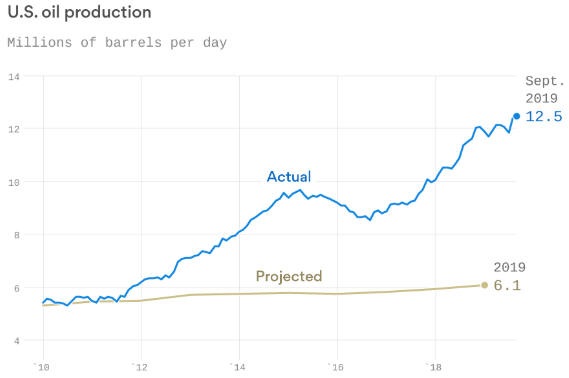

The first chart shows that US oil production today is

approximately double the projection that was made by the EIA in 2009.

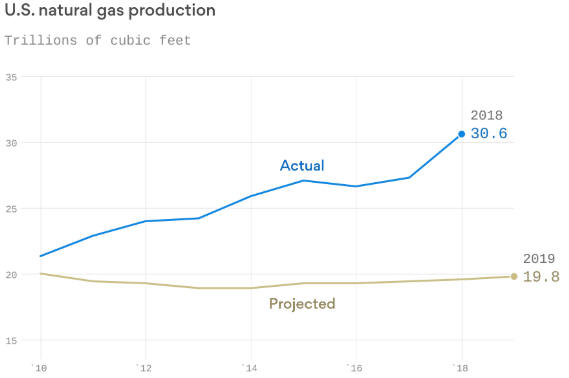

The next chart shows that it's a similar story with natural gas

production.

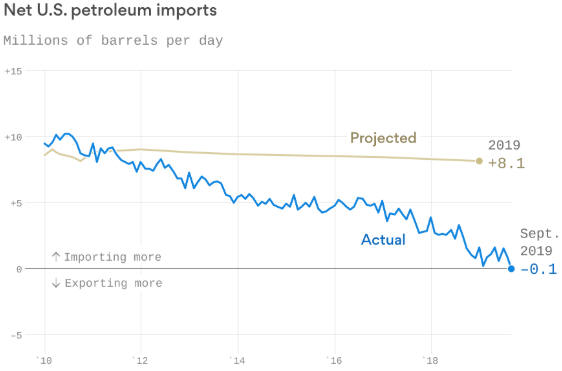

In 2009 the net amount of oil imported by the US was expected to

remain at around 8M barrels/day over the ensuing decade. Instead, the

chart displayed below shows that the US has become a net exporter of oil.

In addition to having economic consequences, this has foreign policy

implications. In particular, it removes the main excuse for US military

intervention in the Middle East.

The popular assumption now is that US production of oil and gas will

continue to trend upward, but this line of thinking could turn out to be

as 'off-the mark' as the projections made by the EIA in 2009. We don't

have the information or the expertise to have a strong opinion on the

matter, but we do know that it is dangerous to assume that the future will

be a linear extrapolation of the recent past.

Current

Market Situation

We have been expecting a

December-February (most likely January) turning point in the oil price.

Prior to the past fortnight a turn from down to up was the more likely

scenario, but that's no longer the case. Due to an extension of the stock

market's short-term upward trend and the positive correlation between the

oil and stock markets, there's a good chance of a multi-month top in the

oil price during January-2020.

A January-2020 top for the oil price

would, we think, prove to be similar to the January-2018 top, meaning that

it would be followed by a sharp multi-week pullback.

The Oil Services ETF (OIH) is consolidating after reaching its 200-day

MA. We expect big things from OIH during 2020, but the short-term

risk/reward is neutral. We won't be surprised if the ETF gains another 10%

before topping on a short-term (1-3 month) basis, but we also won't be

surprised if there is a correction of up to 10% prior to the upward trend

resuming.

The Stock Market

Sentiment Alert, Part 2

A week ago we wrote that there had just been a surge in optimism that

constituted a loud warning signal. This was evidenced by an upward spike

in the TSI Index of Bullish Sentiment (TIBS). Well, the warning signal got

even louder over the past week.

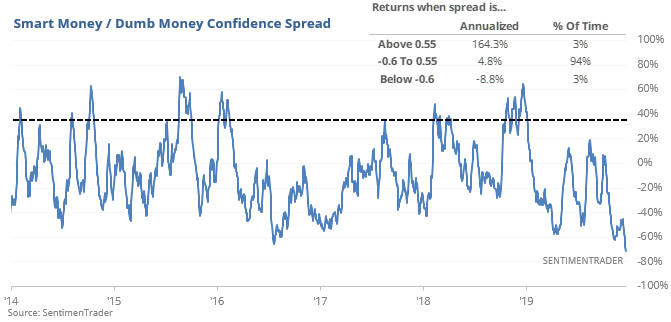

At around this time last year, the

Smart-Money/Dumb-Money Confidence Spread calculated by

Sentimentrader.com was near a

5-year high, meaning that the confidence of the Smart Money (institutional

traders) was extremely high relative to the confidence of the Dumb Money

(retail traders). This was a buy signal.

The current signal is the

opposite. As illustrated by the following chart, the

Smart-Money/Dumb-Money Confidence Spread has just reached a 6-year low.

Rarely has the Dumb Money been so confident relative to the Smart Money.

Current Market Situation

Sentiment isn't the

only reason to suspect that a sizable correction will get underway in the

near future. Another reason is the extent to which the senior US stock

indices and many other stock indices are stretched to the upside in

momentum terms. For example, the following chart shows that the daily

RSI(14) of the NASDAQ100 Index (NDX) has just risen to near a multi-year

high and that the previous two times that the NDX's RSI reached a similar

extreme there was a quick decline of around 10%.

The US stock market's saving grace is that breadth remains strong.

This suggests that while a correction of up to 10% may well be likely, a

bear market is not about to begin.

The only bearish divergence or

non-confirmation we can identify right now is the obvious lack of strength

in the Dow Transportation Average (TRAN). As illustrated below, the TRAN

remains below its early-November high.

It isn't only the US stock market that is stretched to the upside and

due for a sizable correction. On a short-term basis the Emerging Markets

ETF (EEM) is in a similar position to the NDX, having 'gone vertical' over

the past few weeks.

We expect that due to the combination of US$

weakness and relatively attractive valuations, Emerging Market equities

will outperform US equities over the coming 12 months.

It would be reasonable to accumulate new or add to existing bearish

speculations over the coming fortnight. These speculations could take the

form of put options with expiry dates of March-2020 or later that are

5%-10% out of the money, or bear funds such as QID.

At some point

over the next week we may add one or two new bearish option trades to the

TSI List. The ones we have in mind are the SPY March-2020 $290 Put Option

and the IYT (Transportation ETF) March-2020 $180 Put Option.

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date | Description |

| Monday Dec-30 |

Pending Home Sales Chicago PMI |

| Tuesday Dec-31 |

Case-Shiller Home Price Index Consumer Confidence Index |

| Wednesday Jan-01 | Markets closed for New Year's Day |

| Thursday Jan-02 | No important events scheduled |

| Friday Jan-03 |

ISM Mfg Index Construction Spending Motor Vehicle Sales |

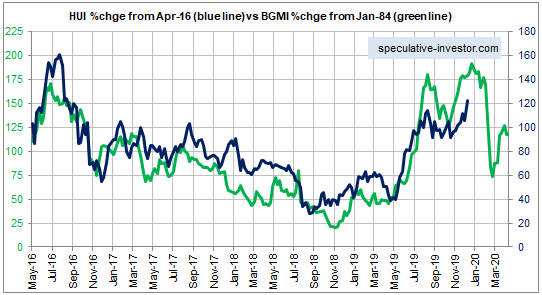

Gold and the Dollar

In terms of time the gold mining sector probably isn't far from an

intermediate-term top, but there is the potential for a continuing strong

advance over the weeks immediately ahead.

As illustrated below, a

top in January would keep the HUI on a similar path to the one traveled by

the Barrons Gold Mining Index (BGMI) in the 1980s.

Our comparison

with the 1980s points to a January-2020 high followed by a large decline

to a March-2020 low. This is just something to be aware of. The current

market eventually will deviate from our 1980s model, but as long as the

model is consistent with the recent price action we will continue to pay

heed to it.

With the gold mining indices and the broad stock market (represented

by the S&P500 Index) having just made new multi-year highs together, the

gold mining sector is far more vulnerable than usual to weakness in the

broad market. That is, don't assume that the gold mining sector will

benefit from significant stock market weakness in the near future.

Instead, due to the gold sector having just rallied with the broad market

it's more likely that gold mining stocks would be dragged down by

significant short-term stock market weakness.

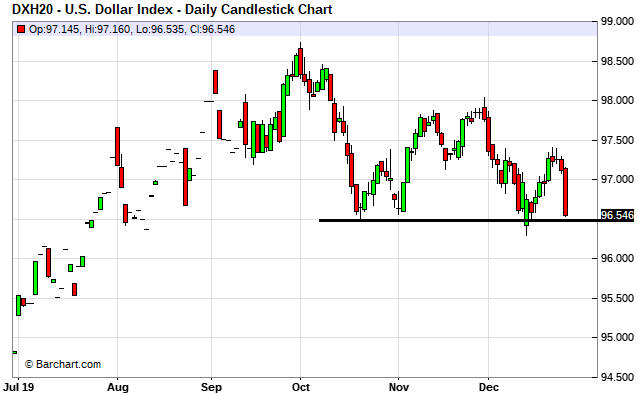

The Currency

Market

The Dollar Index (DX) ended last week slightly

above important support at 96.5. A weekly close or consecutive daily

closes below this support probably would be followed by a multi-week

decline to 94.5 or lower.

As mentioned early in today's report, the

DX initially could be boosted by a 'flight to safety' during the next

sizable stock market decline. However, if the Fed's reaction to the stock

market decline involves a rate cut it would, we think, lead to persistent

weakness in the DX.

The following chart shows that gold and the Yen have diverged over the

past several weeks, with gold beginning to trend upward and the Yen

continuing to drift downward. Based on the historical relationship between

these markets it is reasonable to expect that the divergence will be

closed within the coming month via a surge in the Yen or a plunge in the

gold price. We think that the former is more likely, but it's a virtual

coin toss.

The Yen's decline since its August-2019 peak has traced out a wedge

pattern. Refer to the following daily chart for the details. A daily close

above 92 would break the Yen out of its wedge and suggest that the

gold-Yen divergence mentioned above was going to be resolved via a surge

in the Yen.

Updates

on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

![]() Company

news/developments for the week ending Friday 20th December 2019:

Company

news/developments for the week ending Friday 20th December 2019:

[Note: AISC = All-In Sustaining Cost, EBITDA = Earnings Before

Interest, Tax, Depreciation and Amortisation (a measure of cash flow), EV

= Enterprise Value or Electric Vehicle, FS = Feasibility Study, FY =

Financial Year, IRR = Internal Rate of Return, ISR = In-Situ Recovery, JV

= Joint Venture, MD&A = Management Discussion and Analysis, M&I = Measured

and Indicated, NAV = Net Asset Value, NPV(X%) = Net Present Value using a

discount rate of X%, NSR = Net Smelter Return or Net Smelter Royalty, P&P

= Proven and Probable, PEA = Preliminary Economic Assessment, PFS =

Pre-Feasibility Study]

*Premier Gold (PG.TO)

advised that it is involved in a legal dispute with Centerra Gold

(CG.TO), its JV partner at the feasibility-stage Hardrock gold project in

Ontario. According to PG, the project meets the requirements defined in

the 2015 partnership agreement for mine construction to proceed. According

to CG, it does not. In other words, PG wants to begin the process of

putting the project into production, but CG wants to wait.

CG could

resolve this dispute by purchasing PG's 50% stake in the project or making

a takeover bid for PG. We doubt that it will do this in the near future,

but it's a realistic possibility.

Regardless of how the current

PG-CG dispute is resolved, we would prefer that PG was NOT involved in

moving the Hardrock project through the construction phase. The reason is

that given the US$1B estimated construction cost, doing so would entail PG

taking on a lot of debt and a lot of risk.

![]() List

of candidates for new buying

List

of candidates for new buying

From within the ranks of TSI

stock selections the best candidates for new buying at this time, listed

in alphabetical order, are:

1) ALK.AX (last Friday's closing price:

A$0.55)

2) AOI.TO (last Friday's closing price: C$1.19)

3)

PG.TO (last Friday's closing price: C$2.01)

4) PRQ.TO (last

Friday's closing price: C$0.24)

5) TGB (last Friday's closing

price: US$0.46)

The above list is limited to five stocks. It

sometimes will contain less than five, but it never will contain more than

five regardless of how many stocks are attractively priced for new buying.

![]() The

Fortuna Silver Mines (FSM) Trade

The

Fortuna Silver Mines (FSM) Trade

FSM was added to the TSI

List during the week before last with an initial daily-closing stop at

US$3.15. It was expected to either start working or get stopped out right

away.

It has started working and is up by 16% to date. As a result

it makes sense to lift the sell stop.

From now on we will use a

10% trailing stop. For example, the high to date (since the start of the

trade) is US$4.07, so the current sell stop is US$3.66.

![]() Tax

Trade Update

Tax

Trade Update

Three weeks ago we mentioned five candidates

for a tax-loss trade that we planned to track as a group, with each stock

being added to the group if/when it became available at a targeted entry

price. The aim was to average into the group over the remainder of this

year and exit at a profit during the first month of the New Year.

At the moment our tax trade group contains three stocks: AAL.V, TGB and

TK.V. The other two potential inclusions (CGT.TO and GRG.V) didn't quite

make it to their stipulated entry prices before beginning to rebound.

Consequently, they have been ruled out.

We were considering a few

other stocks for inclusion in the tax trade group, but each has enjoyed a

significant bounce over the past two weeks. Clearly, the

post-tax-loss-selling rebound started early this season.

Here is a

table showing the performance to date of our tax trade group. The entire

group will be exited within the coming three weeks and any member of the

group will be automatically removed if it trades at least 100% above its

entry price.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

https://stockcharts.com/

https://www.barchart.com/