![]()

![]()

![]()

![]()

-- Weekly Market Update for 17th June 2019

Big Picture

View

Here is a summary of our big picture

view of the markets. Note that our short-term views may differ from our

big picture view.

The BULL market in US Treasury Bonds that began in the early 1980s ended in mid-2016, but there will be many years of topping action in bond prices and bottoming action in bond yields before major new trends get underway. A major decline in government bond prices will unfold during the 2020s. (Last update: 11 September 2017)

The stock market, as represented by the S&P500 Index, commenced a secular BEAR market during the first quarter of 2000, where "secular bear market" is defined as a long-term downward trend in valuations (P/E ratios, etc.), gold-denominated prices and inflation-adjusted prices. This secular trend will bottom in 2020 or later. (Last update: 11 September 2017)

A cyclical BEAR market in the US Dollar began in 2016-2017. (Last update: 11 September 2017)

Gold commenced a secular bull market relative to all fiat currencies, the CRB Index, bonds and most stock market indices during 1999-2001. This secular trend will peak in 2020 or later. (Last update: 11 September 2017)

Commodities,

as represented by the CRB Index, commenced a

secular BULL market in 2001 in nominal dollar terms. The first major

upward leg in this bull market ended during the first half of 2008, but

a long-term peak won't occur until 2020 or later.

(Last

update: 11 September 2017)

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

True

Fundamentals Summary

[Notes:

1) The date shown next to the current True Fundamentals Model (TFM) signal is

when the most recent change occurred. 2) Charts of the Gold and Equity

TFMs are included in the "Charts and Indicators" section of the TSI web

site]

| Market | True Fundamentals Model (TFM) |

| Gold (US$ Price) | Bullish (04 Jan 2019) |

| US Equity (SPX) | Bearish (19 Apr 2019) |

| Currency (Dollar Index) | Neutral (15 Mar 2019) |

| Commodities (GNX) | Bearish (01 Jun 2018) |

Last week's posts at the TSI Blog

The "true fundamentals" are still in gold's favour

Summary of current

thinking/positioning

1) The Dollar Index (DX) has

signaled a downward trend, but it could be a while before the new downward

trend becomes consistent. A counter-trend rebound is currently underway.

2) The US$ gold price looks set to break above resistance at $1350

within the coming several weeks, perhaps following a correction to the

low-$1300s.

3) The gold mining indices have extended their

short-term rebounds and are close to resistance that probably will hold

for at least three weeks. These rebounds should evolve into something more

than counter-trend reactions IF the US$ begins to trend downward with

conviction.

4) The US stock market remains in correction mode. The

SPX could make a marginal new all-time high within the next three weeks,

but we expect that it will test its early-June low within the next three

months.

5) An upside blow-off has set the stage for a large T-Bond

decline. The decline should begin by early July at the latest.

6)

Oil's correction is probably very close to complete, at least in terms of

price, although stock market weakness during July-August could push the

oil price to a new multi-month low.

7) We are holding a cash

reserve of 25%-30%.

TSI Access

Problems

Late last month the TSI web site

was moved to a new server, leading to a small number of subscribers

experiencing access problems.

As noted in the 5th June Interim

Update:

"Most problems reported to date have come from

subscribers using Apple computers, but there also were a few reported

issues from subscribers using other PCs. In these cases the problem

manifests as a request to confirm a "Security Certificate" and "HTTP Error

403.16". A potential solution is the same -- try using a different

browser. For example, if you have been using Chrome, then try using

Firefox. Also, when the "Security Certificate" request pops up, click

"Cancel" (that is, don't click "OK"). Based on info received from a couple

of subscribers, this can enable access."

Neither we nor our

web hosting company can duplicate the reported problems despite testing

almost every conceivable device/browser combination, making it very

difficult for us to determine the best solution. However, as far as we

know, nobody using the Firefox browser has had a problem with access since

the website relocation.

Please let us know if you are still

experiencing problems accessing the site and which browser you are using.

The Fed's next

move

According to the prices of Fed

Funds Futures (FFF) contracts, the market currently expects the Fed to

make three (three!) rate cuts before the end of this year and to make its

first rate cut at the FOMC meeting scheduled for July 30-31. The Fed is

not expected to make any adjustments to its monetary levers at the FOMC

Meeting scheduled for this coming Tuesday-Wednesday, but this week's

meeting will be important because if the Fed is going to start a rate

cutting program in July then it will want to lay the groundwork via the

wording of its 19th June post-meeting statement.

With the market

already having priced-in three rate cuts it will be difficult for the Fed

to over-deliver on the side of monetary accommodation. It's more likely

that the Fed will under-deliver, that is, that the Fed will cut rates by

less than the market currently expects, although there is a realistic

chance that the Fed will generate some excitement by making its first move

a 0.50% cut as opposed to the expected 0.25% cut.

What the Fed does

will be largely determined by what the stock market does. If the stock

market performs the way we expect then there will be one or two rate cuts

before the end of September, but none during the subsequent several

months. That being said, we admit to be being surprised by how quickly and

completely the Fed capitulated (abandoned its "monetary policy

normalisation" plan) over the past 6 months.

Taking into account

the performances of the US stock market and economy, it is more than a

little strange that almost everyone now expects a rate-cutting program to

get underway in the near future. As far as we can tell, the main cause of

this unusual (to put it mildly) set of circumstances is the inversion of

the yield curve.

Almost everyone, including everyone in a senior

position at the Fed, knows that a yield curve inversion precedes a

recession. Armed with this knowledge, the Fed believes that it can stave

off a recession by taking action that ends the inversion, that is, by

taking actions that steepen the yield curve.

However, an inverted

yield curve doesn't cause a recession; it's just a symptom that a

monetary-inflation-fueled boom is 'long in the tooth'. Therefore, the Fed

can't prevent a recession by taking actions that eliminate the curve

inversion. This would be like a doctor trying to cure a life-threatening

disease that has high temperature as a symptom by immersing the patient in

cold water. The patient might feel better for a short while, but the

disease will remain.

Commodities

A bottom, but not THE

bottom, for oil

Last week the oil price tested its early

June low and then turned upward on Thursday. The catalyst for the up-turn

was news that two oil tankers had been attacked in the Gulf of Oman, but

we suspect that the price would have reversed upward without the help of

this news.

Last week's successful test of the preceding week's low

has created a 'double bottom' that probably will hold for at least a few

weeks. However, the lack of strength in the oil market in the face of a

strong stock market over the past fortnight suggests that oil's final

correction low is not yet in place.

If oil is going to take out its

early-June low then the most likely time for it to do so will be after the

S&P500 Index (SPX) has dropped to the vicinity of its own early-June low.

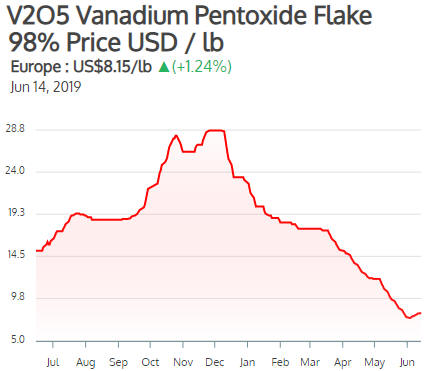

The vanadium price went up!

In the 27th May

Weekly Update, under the heading "The most relentless decline ever", we

wrote:

"The price of vanadium pentoxide (V2O5) in Europe has

not had an up-day since 26th November of last year. Apart from 30-40

'unch' days, since then it has dropped on every trading day. We've never

seen anything like this."

The "most relentless decline ever"

ended on 4th June. Since then, the vanadium pentoxide price in Europe has

edged up from US$7.50/pound to US$8.15/pound.

There are no technical or sentiment indicators that can give us clues

regarding what to expect from the vanadium price over the next several

months. That's because price is determined by supply from the mining

industry relative to demand from industrial users (steel manufacturers,

mostly). We suspect that supply from the mining industry is roughly the

same now as it was a year ago and won't change by much over the next year,

so the price will be driven by changes in industrial demand.

Our

guess is that the industrial demand for vanadium will increase over the

next six months due to the rebuilding of stockpiles that were drawn down

over the past six months and new Chinese rebar standards coming into full

effect. This should result in an upward bias in the price, but not the

sort of spectacular rally that occurred in 2018.

If you don't have

any exposure to vanadium it would be reasonable to add some. In this

regard it's worth revisiting Largo Resources (LGO.TO), a profitable

vanadium producer operating the Maracas mine in Brazil.

In the 22nd

April Weekly Update we wrote that due to its recent price action LGO had

become a worthwhile moderate-risk speculation. At that time the LGO price

was in the C$1.60s and the vanadium price was around US$12. Despite the

vanadium price now being about 30% lower, the LGO price is almost 20%

higher and clearly has broken upward from the channel drawn on the

following daily chart.

We think that LGO would be a good candidate

for new buying if it were to pull back to near its 50-day MA (currently at

C$1.76). Also, Prophecy Development Corp. (PCY.TO), an exploration-stage

vanadium miner and a member of the TSI Small Stocks Watch List, would be a

reasonable speculation below C$0.20.

A new 50-year low for platinum

Last week the

platinum price made a new 50-year low. Not in US$ terms, obviously, but in

gold terms. Also, the platinum price is in the bottom third of its

multi-decade range relative to the silver price. Therefore, investors who

are accumulating physical metal with the aim of holding for at least two

years should favour silver over gold and should favour platinum over both

silver and gold.

Based on the price action there is a risk that the

US$ platinum price will test or spike below its 2018 low near $750 prior

to a long-term reversal, but the remaining downside potential is very

small relative to the upside potential.

A weekly close above the

April-2019 high ($920.40) would confirm a long-term reversal to the

upside.

The Stock Market

The S&P500 Index (SPX) made a

new rebound high last Monday and then consolidated over the rest of the

week. It is about 2% below its early-May all-time high, but the lower

section of the following daily chart shows that the NYSE Advance-Decline

Line (ADL), a measure of market breadth, made a new all-time high last

Thursday. As a result, there is now a bullish divergence between the ADL

and the SPX.

The ADL's new all-time high is evidence that the bull

market is not over, but it doesn't preclude another sharp multi-week

decline along the lines of what happened last month.

The TSI Put/Call Indicator (TPCI) is shown in the bottom section of

the following chart. It generated a new sell signal on Friday 14th June.

Such signals were rare prior to last September, but over the past 9

months there have been five -- a buy signal in late-December and sell

signals in late-September, February, April and now June. On the following

chart, green arrows mark the buy signals and red arrows mark the sell

signals.

A TPCI signal identifies the sort of sentiment extreme

that often, but not always, occurs near a significant turning point in the

price. All signals over the past two years were useful with the exception

of the sell signal in February-2019.

Last Friday's TPCI sell

signal means that even if the SPX gains some additional ground over the

coming three weeks, it probably will trade well below its current level

within the next three months.

The new high for the ADL suggests that there will be some additional

upside prior to the start of the next tradable decline, while the TPCI

sell signal warns that the direction of the next substantial move will be

down.

It would be reasonable to average into bearish speculations

in anticipation of a meaningful decline getting underway by mid-July. For

traders using options to profit from a market decline, the options should

have expiry dates of September or later.

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date | Description |

| Monday Jun-17 | No important events scheduled |

| Tuesday Jun-18 | Housing Starts |

| Wednesday Jun-19 | FOMC Statement and Powell Press Conference |

| Thursday Jun-20 | Q1 Current Account |

| Friday Jun-21 | Existing Home Sales |

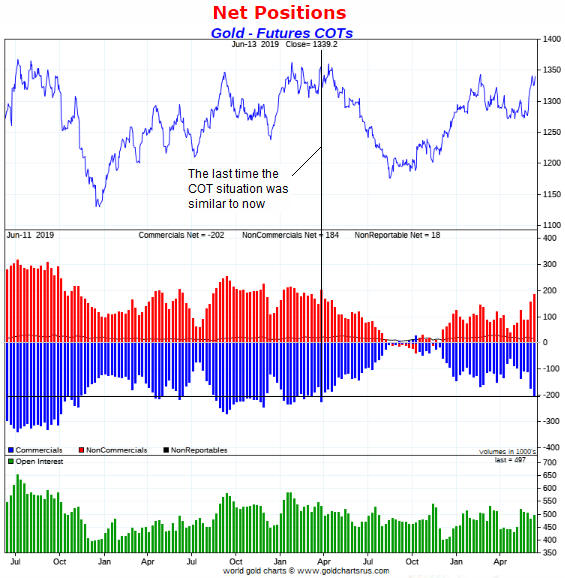

Gold and the Dollar