Platinum versus

Gold / Considerable Slack

The following is an extract from

commentary that was posted at www.speculative-investor.com on 14th April

2002.

Platinum versus Gold

Although they are both precious metals

the prices of platinum and gold respond in very different ways to different

economic and monetary environments.

Below is a long-term chart of the platinum/gold

ratio. The chart was taken from http://www.cairns.net.au/~sharefin/Markets/Master.htm,

an excellent resource for financial market data. We've added notes and

lines to the chart to illustrate (labour?) the point we are about to make.

Platinum tends to out-perform gold

during prolonged periods of economic growth or perceived monetary stability

and to under-perform gold during prolonged periods when confidence in the

economy and the financial system is deteriorating. This relationship occurs

due to gold's status, a status that has developed over thousands of years,

as the ultimate form of money outside the financial system.

With reference to the above chart we

can see that the platinum/gold ratio plunged (the gold price rocketed higher

relative to the platinum price) during the early-1970s and bottomed, in

late-1974, at around the same time that the stock market was hitting its

major low. It is also apparent that the platinum/gold ratio trended higher

from 1982 through to 2000, reaching what looks like a bubble peak in late-2000

at around the same time that the stock market bubble began to lose air

at a rapid rate.

If the decline in the stock market

and real economic growth over the past 18 months represents nothing more

significant than an interruption to the 1990s' boom then the platinum/gold

ratio will move above its 2000 peak over the coming 2 years. However, if

we have just witnessed the end of an era characterised by, amongst other

things, growing confidence in government, central banks and the fiat money

system, then the year 2000 gave us a multi-decade peak in the platinum/gold

ratio.

Our analyses of all the financial markets

over the past few years strongly suggest that the level of confidence in

government and government-sponsored money made a secular peak in 2000 and

is now in a secular downtrend. As such, the downturn in the platinum/gold

ratio in late-2000 represents a major trend reversal.

The above chart shows that trends in

the platinum/gold ratio, once set in motion, tend to continue for at least

4 years. In other words, we should expect the gold price to trend higher

relative to the platinum price until at least the second half of 2004.

This means that although some exposure to platinum (via the stocks of platinum/palladium

producers) is desirable we should, based on the evidence at hand, continue

to substantially overweight gold relative to platinum in our investment

portfolios.

There are certainly going to be extended

periods over the next few years - periods when the prospects for economic

growth temporarily take a turn for the better - when platinum will out-perform

gold. However, the trend in the ratio is now DOWN and we will not be surprised

if gold trades higher than platinum at some point over the next 2-3 years.

Considerable Slack

"Inflation declined during the recession

and seems poised to decline further as growth accelerates in an economy

with considerable slack," he [Dallas Federal Reserve Bank President

Robert McTeer] said in the Dallas Fed's annual report.

The above really is an incredible statement

from the president of the Dallas Federal Reserve Bank. There was apparently

so little slack in the economy during 1999 that the Fed felt compelled

to raise short-term interest rates a number of times, yet today, with consumer

spending and the overall level of indebtedness having grown considerably

over the past 3 years, the economy supposedly has "considerable slack".

We wouldn't argue that there is considerable slack in those few sectors

of the economy where capacity was expanded at a phenomenal rate during

the Fed-sponsored NASDAQ bubble (eg, the telecom industry), but the absence

of "slack" that led to an energy crisis during 2000-2001 has certainly

not been addressed.

The 'lack of slack' in the US economy

is evidenced by the surge in energy prices over the past 5 months despite

the continuing strength of the US$ (only the recent gains were Middle East

related). It is also evidenced by the behaviour of the bond market.

Below is a chart showing the yield

on the 10-year T-Note during the 6-month period following the 1990-1991

recession. At the end of a recession there is typically a lot of 'slack'

in the economy and this 'slack' enables long-term interest rates to fall

during the initial stages of recovery. This is what happened after the

early-90s recession.

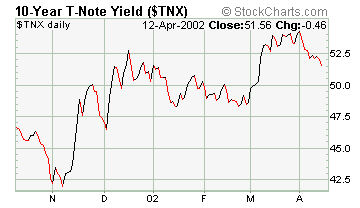

Below is a chart showing the yield

on the 10-year T-Note over the past 6 months. If there really was "considerable

slack" in the economy and inflation really was "poised to decline further"

then interest rates would still be trending lower. That is clearly not

the case.

When McTeer uses the word inflation

he is incorrectly referring to an increase in the CPI. If we define inflation

correctly (as an increase in the supply of money) then the current US inflation

rate is 9.1%. This inflation will eventually put upward pressure on some

prices, although anyone who truly believes that the CPI accurately represents

cost of living changes, or is even an honest attempt to accurately represent

cost of living changes, deserves a gullibility award. Ironically, if we

define our terms correctly then McTeer's statement that inflation is "poised

to decline further" is actually true since the money supply growth rate

is

poised to decline further.

Regular financial market forecasts

and

analyses are provided at our web site:

http://www.speculative-investor.com/new/index.html

One-month free trial available.

|