--

Weekly Market Update for the Week Commencing

23rd January 2017

Big Picture

View

Here is a summary of our big picture

view of the markets. Note that our short-term views may differ from our

big picture view.

The BULL market in US Treasury Bonds

that began in the early 1980s ended in early-2015, but there will be many years

of topping action in bond prices and bottoming action in bond yields before

major new trends get underway. (Last update: 29 June 2015)

The stock market, as represented by the S&P500 Index,

commenced

a secular BEAR market during the first quarter of 2000, where "secular

bear market" is defined as a long-term downward trend in valuations

(P/E ratios, etc.) and gold-denominated prices. This secular trend will bottom sometime between 2018 and 2020.

(Last update: 29 June 2015)

A secular BEAR market in the

US

Dollar

began during the final quarter of 2000 and ended in July of 2008. This

secular bear market will be followed by a multi-year period of range

trading.

(Last

update: 09 February 2009)

Gold commenced a

secular bull market relative to all fiat currencies, the CRB Index,

bonds and most stock market indices during 1999-2001.

This secular trend will peak sometime between 2018 and 2020.

(Last update: 29 June 2015)

Commodities,

as represented by the CRB Index, commenced a

secular BULL market in 2001 in nominal dollar terms. The first major

upward leg in this bull market ended during the first half of 2008, but

a long-term peak won't occur until 2018-2020.

(Last

update: 29 June 2015)

Copyright

Reminder

The commentaries that appear at TSI

may not be distributed, in full or in part, without our written permission.

In particular, please note that the posting of extracts from TSI commentaries

at other web sites or providing links to TSI commentaries at other web

sites (for example, at discussion boards) without our written permission

is prohibited.

We reserve the right to immediately

terminate the subscription of any TSI subscriber who distributes the TSI

commentaries without our written permission.

Outlook Summary

Market

|

Short-Term

(1-3 month)

|

Intermediate-Term

(6-18 month)

|

Long-Term

(2-5 Year)

|

|

Gold

|

N/A |

Neutral

(21-Nov-16) |

Bullish

|

|

US$ (Dollar Index)

|

N/A |

Neutral

(17-Aug-16) |

Neutral

(19-Sep-07) |

|

US Treasury Bonds (TLT)

|

N/A |

Neutral

(21-Nov-16)

|

Bearish |

|

Stock Market (DJW)

|

N/A |

Neutral

(14-Nov-16) |

Bearish |

|

Gold Stocks

(HUI)

|

N/A |

Neutral

(21-Nov-16) |

Bullish

|

|

Oil |

N/A |

Neutral

(26-Oct-15) |

Bullish

|

|

Industrial Metals

(GYX)

|

N/A |

Neutral

(10-Oct-16) |

Bullish |

Notes:

1. Our short-term expectations are discussed in the commentaries, but except in

special circumstances we won't attempt to assign a "bullish", "bearish" or

"neutral" label to these expectations.

2. The date shown below the current outlook is when the most recent outlook change occurred.

3. "Neutral" means that we think risk and reward are roughly in balance with respect to the timeframe in question.

4. Long-term views are determined almost completely by fundamentals and intermediate-term views

are determined by a combination of fundamentals, sentiment and technicals.

Last week's posts at the TSI Blog

The "war on cash" has nothing to do with fighting crime

Summary of current

thinking/positioning

1) Thinking that the rebounds in

gold, silver and the associated mining indices are not yet close to being

over, but on the lookout for profit-taking opportunities in individual

stocks.

2) Expecting intermediate-term tops in non-gold commodities

and the associated equities later this quarter. Looking for profit-taking

opportunities, but planning to maintain some long-term exposure. Hedged

via EEM and USO put options.

3) Thinking that the US Treasury Bond

has significant additional short-term upside (within a long-term bearish

trend).

4) Expecting an extension of the US equity bull market and

expecting a generally-bullish global equity trend, but concerned about

short-term downside risk.

5) Thinking that the Dollar Index is

immersed in a 2-3 month correction, after which its longer-term upward

trend will resume.

6) Maintaining a large cash reserve to hedge

downside risk in equities (current cash percentage is about 40%).

Yearly Forecast

Link

Our 2017 annual forecasts were

spread across three commentaries during the first half of this month. For

ease of reference, these forecasts have now been consolidated into a

single page at

http://www.speculative-investor.com/new/yearly.asp.

Commodities

Copper

The US$ copper price has essentially been in consolidation mode since

spiking up to the $2.70s in early-November. As previously mentioned, the

price action suggests the potential for a rise to around $3.00 prior to an

intermediate-term peak.

Critical (trend-defining) support remains

at $2.45 and a daily close below this support would leave little doubt

that an intermediate-term top was in place. However, it would be

reasonable to view a daily close below the 50-day MA as an early warning

of an intermediate-term reversal to the downside. The 50-day MA is now at

$2.57 (only 0.04 below the current price) and is rising.

Oil

Recent oil-market speculation has been

linked to stock-market speculation. Therefore, with the Dow Industrials

and S&P500 indices having moved sideways near the tops of their 12-month

ranges over the past month it makes sense that the oil price has done the

same. The recent link between the two markets suggests that there won't be

substantial downside in the oil price until there is a sizable correction

in the stock market. Both are likely to occur during the first half of

this year, albeit at least a couple of months later than we originally

expected.

The oil price has short-term upside potential to the 2015

high in the low-$60s, whereas short-term downside potential is probably

limited by the 200-day MA near $47.

Our main oil-related concern is that speculative enthusiasm for the

commodity is out of synch with the commercial supply-demand situation.

This creates the risk that unless the fundamental situation becomes a lot

more bullish within the next few months, the price will have to move a lot

lower. We therefore think that the intermediate-term downside potential is

much greater than the short-term downside potential mentioned above.

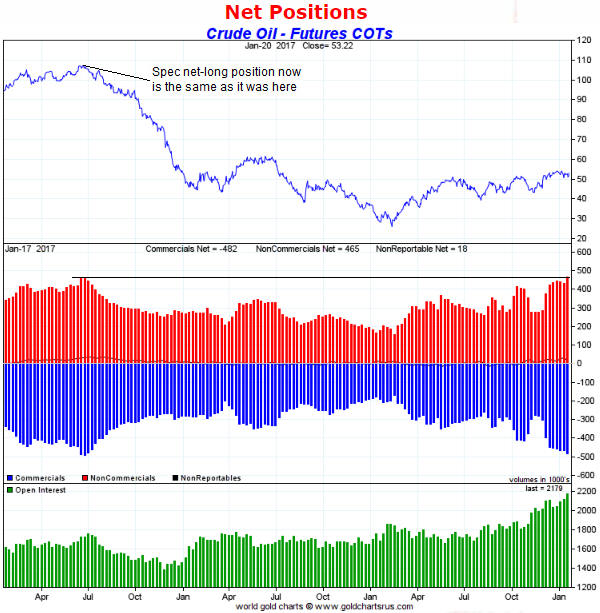

The current extent of speculative enthusiasm for oil is illustrated by

the following weekly chart from

goldchartsrus.com. The chart shows that the speculative net-long

position in oil futures rose last week to a 3-year high and is now roughly

the same as it was in June of 2014, when the oil price was around

$110/barrel. Putting it another way, the last time the speculative

net-long position in oil futures was as high as it is today the oil price

was about to commence a 6-month decline of more than 50%.

It is not reasonable to expect a 50% decline in the oil price over the

next 6 months, because oil is nowhere near as expensive relative to other

commodities as it was in mid-2014. However, the intermediate-term downside

risk is uncomfortably high. Consequently, we will be looking for

opportunities over the weeks ahead to purchase USO (oil ETF) put options

with a July-2017 expiry date.

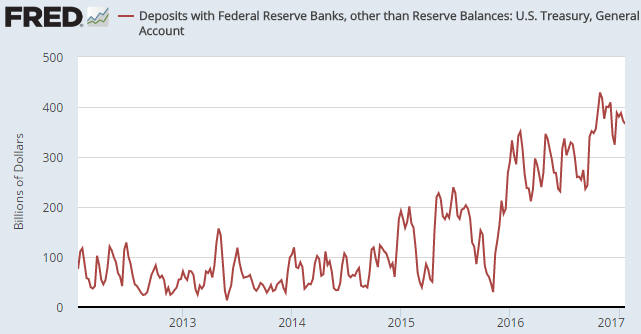

The latest on the US

government's bank account

The Treasury General Account is

the name of the US federal government's bank account at the Fed. The bulk

of the government's income from taxing and borrowing gets cycled through

this account.

Money going into the Treasury General Account is

effectively removed from the economy until it is spent, but prior to the

past 14 months the account itself had minimal economic relevance. This is

because the account balance was always small, with almost all the money

entering the account being spent quickly. Since November-2015, however,

the balance in this account has been large enough and/or has shifted by

enough from month to month to have an influence on the economy and the

stock market.

Our most recent comment on the Treasury General

Account was in the 19th December Weekly Update. At that time there had

just been a 2-week draw-down of $85B (meaning: $85B had just been released

into the financial markets and the economy), which was a little strange.

It was a little strange because a) the main reason for the preceding

build-up in the account was to provide the Treasury with a cash buffer in

case access to the debt market was temporarily shut off, and b) there is a

looming threat that access to the debt market will temporarily be shut off

when the "debt ceiling" comes up for re-negotiation in March-2017.

In attempting to explain what was going on, we hazarded the following

guess:

"...with a Republican moving into the White House and

with the Republican Party in control of both legislative chambers (the

Senate and the House of Representatives), the Obama Administration has

decided to spend whatever money it can before it departs. Having very

little cash in reserve prior to an imminent 'debt ceiling standoff' will

potentially create a substantial problem for the Trump Administration to

deal with. Also, the superficial impression will be created that the

Democrats left the economy in good shape.

The probability that our

guess is correct will increase if the Treasury's General Account continues

to be drawn down prior to Trump's 20th January Inauguration."

Our guess that the Obama Administration was engaged in a last-minute

spending spree appears to have been off-the-mark. As illustrated below,

the balance in the Treasury General Account has since risen from about

$325B to about $365B.

However, it is worth noting that there is a

strong seasonal tendency for the balance in the Treasury's account to rise

during the second half of December and the first half of January. In other

words, it is normal for the money coming into the government to handily

exceed the government's spending between mid-December and mid-January. It

is therefore possible that a last-minute spending spree by the outgoing

administration was masked by the seasonal net in-flow of money. We will

probably never know for sure.

The Stock Market

The US

In mid-December the Dow Industrials Index (Dow) was as 'overbought' on a

short-term basis as it ever gets. Also, sentiment at the time was

dangerously exuberant. This 'overbought/overbullish' situation could have

been resolved via a steep decline, but it was actually resolved via more

than a month of trading sideways within an unusually narrow range. In

fact, the Dow's trading range since mid-December has been narrow enough to

be record-breaking. In percentage terms it is the Dow's narrowest 5-week

range in at least 60 years and possibly ever.

On a short-term basis

the market is no longer 'overbought' and sentiment indicators are now

mixed. It is certainly possible that the market will experience a

post-Inauguration decline (as many pundits are predicting), but another

multi-week surge to the upside is equally probable.

The most

bearish price action would involve a quick rise to well above 20,000

followed within less than two weeks by a decline to well below 20,000.

Elsewhere

The EURO STOXX 50 Index (STOX5E),

the European equivalent of the Dow Industrials Index, broke above the top

of a year-long basing pattern in December. The chart suggests short-term

upside potential to around 3500, while downside risk should be limited by

former resistance (now support) at around 3150.

We suspect that

European equities will handily outperform US equities during 2017 and also

perform well in absolute terms, although if our currency-market outlook is

close to the mark there will be significant stock-market weakness in

Europe from the time of a Q1 high to around the middle of the year.

The Emerging Markets Equity ETF (EEM) rebounded from an early-November

low and has managed to get above resistance at $36, but remains well below

last year's high of around $38. The point we wanted to make/reiterate

today is that there has traditionally been a strong positive correlation

between EEM and broad-based commodity indices such as GNX (the Goldman

Sachs Spot Commodity Index). This correlation is illustrated below.

EEM and GNX have tracked each other less closely than usual over the

past 7 months, but it is still reasonable to expect that a big move to

either the upside or the downside in one will be accompanied by a similar

move in the other.

This week's

significant US economic events

[Notes:

1) The most important events

(to the markets) are shown

in bold. 2) A list of global economic events can be found

HERE]

| Date |

Description |

|

Monday January 23 |

No important events scheduled |

| Tuesday

January 24 |

Existing Home Sales |

|

Wednesday January 25 |

No important events scheduled |

|

Thursday January 26 |

International Trade Balace

New Home Sales

Leading Economic Indicators |

|

Friday January 27 |

Durable Goods Orders

Q4 GDP (preliminary)

Consumer Sentiment |

Gold and the Dollar

Gold

Cycles

Market prices tend to move in

cycles; from very long-term cycles lasting decades to short-term cycles lasting

a few weeks or months. These cycles are often very clear in hindsight --

particularly the ones that last a few years or more -- but putting a lot of

emphasis on cycles in market analyses can create problems. This is because in

real time things regularly don't play out the way that a purely cycles-based

view of the world suggests they should.

A good example of cycles-based

analysis leading to a monumental error is provided by those followers of the

Long Wave, or Kondratyev Wave, who anticipated a collapse in US$-denominated

commodity prices during the first decade of this century based on their belief

that the world was scheduled to experience the "Kondratyev Winter" (a long

period in which commodity prices are supposed to fall). As it turned out,

commodity prices rose sharply. So, either the K-Wave winter ended in 2001 (a

possibility that none of the K-Wave adherents acknowledged at the time), or

didn't begin until 2011, or hasn't yet begun, or is never going to occur because

there is no such thing, or is demonstrating different characteristics to

previous K-Wave winters because this is the first time that this part of the

Long Wave is occurring while none of the national currencies are officially tied

to gold. In other words, even if the K-Wave idea has some merit it can't be

reliably applied to speculating/investing.

Our belief is that cycles are

real and deserve to have a place in our overall market analysis, but that it is

important not to defer to any interpretation of cycles just as it is important

not to be married to any preconceived ideas of what the markets are going to do

in the future. Instead, speculators should be continually developing a thesis

(the thesis is always a work-in-progress because there are no start and finish

points in the markets) by assessing the fundamentals and the price action and,

more generally, by paying attention to what is happening in the world. A review

of cycles could, and probably should, form part of this thesis.

We

generally ignore short-term cycles, because they are more often the result of

randomness than genuine cyclicality. However, we do pay attention to longer-term

cycles that have regularly/reliably timed turning-points in the markets. We

don't assume that the next occurrence of any cycles-predicted turning point will

usher in a reversal, but if a market trends strongly into a cyclical time-window

then our interest will almost certainly be piqued. For example, when the British

Pound collapsed during September-October last year our attention was drawn to

the fact that an 8-year cycle low for this currency was 'due' in early-2017

plus/minus a few months. There is absolutely no guarantee that the Pound's

8-year cycle is going to 'work' this time around, but the fact that the Pound

trended strongly into the turning-point window increases the probability that it

will.

Now that we've explained how we think cycles should fit into the

overall market analysis, let's revisit gold's 8-year cycle. It's appropriate to

do so because the December-2016 low occurred within the turning-point window

predicted by this cycle.

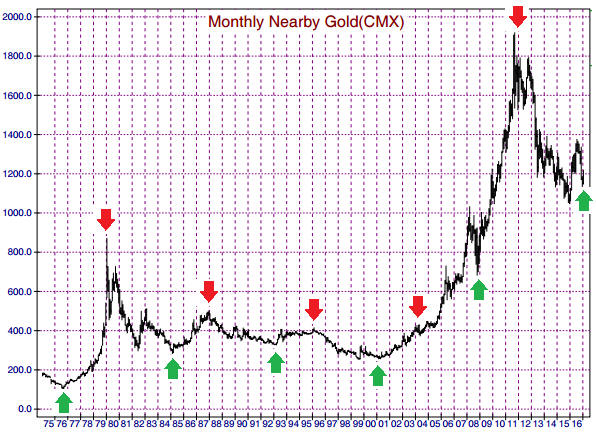

Since the mid-1970s gold has made a cycle low

every 8 years (+/- a couple of months) beginning in 1977 and a cycle high every

8 years (+/- a couple of months) beginning in 1980. A monthly chart on which the

8-year cycle lows are indicated by upward-pointing green arrows and the 8-year

cycle highs are indicated by downward-pointing red arrows is displayed below.

The last two 8-year cycle lows were in early-2001 and late-2008, so the next

one was/is due in late-2016 or early-2017. With the gold price having turned

upward in December following a steep multi-month decline it is certainly

possible that the 8-year cycle has just timed another important bottom.

The 8-year cycle makes no prediction regarding the magnitude of the rally

following a cycle low. For example, the cycle low in late-1976 was followed by a

3-year rally of more than 700% whereas the cycle low in early-1993 was followed

by a 3-year rally of only 29%. The cycle's only predictions are that the cycle

low should hold for at least a few years and be followed about three years later

by an 8-year cycle high.

Current Market

Situation

The idea that an 8-year cycle low was put in place in

December conflicts with our view that the US$ gold price will probably undercut

its December-2016 low in the second or third quarters of this year. However,

this conflict is not a problem, because:

1) At this stage we don't know

for sure that an 8-year cycle low is in place. For instance, similar to the way

the 8-year cycle high that was due in early-2012 occurred a few months earlier

than the predicted time, the 8-year cycle low due about now could occur a few

months later than the predicted time.

2) For reasons that have nothing to

do with cycles we anticipated a strong rebound in the gold price from its

December-2016 low.

3) If the December-2016 low is destined to be

longer-lasting than we currently expect then a pronounced fundamental shift in

gold's favour should become evident within the next few months. The new

information would prompt a change in our view with no harm done (since we would

have participated in the initial rally from the low).

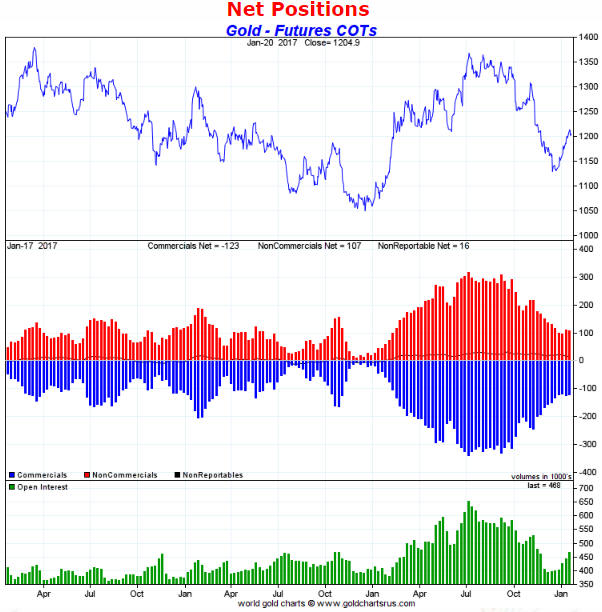

Gold's Commitments

of Traders (COT) situation is worth highlighting today, mainly because it hardly

changed at all during the rebound of the past few weeks. The relevant chart is

displayed below. In other words, the net position of speculators in Comex gold

futures is roughly the same now, with the gold price in the low-$1200s, as it

was when the gold price was bottoming in the $1120s last month. This is both

unusual and unequivocally bullish. It is bullish because it means that the gold

price has managed to gain about $80/ounce without consuming any

speculative-buying fuel.

Also worth highlighting is that the current rebound has differentiated

itself from the preceding rebound (the rebound from the early-October low) by

not reversing downward immediately after reaching the 50-day MA.

With gold's rebound from its December bottom having reached the lower end of our

target range (the low-$1200s) without using-up any speculative fuel and with

inter-related markets poised to remain supportive for gold in the short-term,

there is now a good chance that the gold price will reach the upper end of our

target range before making a top that holds for more than 2-3 weeks. The upper

end of our target range is defined by the 200-day MA, which is presently near

$1270.

An intervening correction should find support near the 50-day MA,

which is presently in the low-$1180s.

Gold Stocks

On a very short-term basis the gold-mining sector is out of synch with the

bullion market. Whereas the US$ gold price trended upward to some sort of peak

on 17th January, the HUI has been in consolidation mode since 5th January. This

is notable, but not unusual.

We

suspect that the gold-mining sector's consolidation will end this week, but

before it ends there could be a decline to near the HUI's 50-day MA in the

mid-180s. It would be reasonable for short-term traders to view such a decline

as a buying opportunity.

The 200-day MA near 220 continues to be the

bottom of our target range for the HUI's short-term rally, although it is

becoming increasingly likely that the rally will end closer to the top than the

bottom of this range (the top of the range is 250). One reason is the evidence

that the gold price is headed for the top of its own target range. Another

reason is that some gold-mining indices and ETFs have already reached their

200-day MAs. For example, in last week's Interim Update we included a chart

showing that the XAU had reached its 200-day MA. For another example, the

following chart shows that GDXJ has tested its 200-day MA several times over the

past two weeks.

The Currency Market

The downward correction in the

Dollar Index continued over the past week and probably isn't complete. We'll

take the evidence as it comes, but at this stage we expect to see the Dollar

Index in the high-90s prior to the start of the next multi-month US$ rally.

Critical support for the Dollar Index lies at 97.5. This is as far as the

dollar could fall while leaving its intermediate-term upward trend intact.

The British Pound and the Japanese Yen are the major currencies with the

most bullish Commitments of Traders (COT) situations. We discussed the Pound at

length in last week's Interim Update, so we'll now turn our attention to the

Yen.

As mentioned many times in the past, the Yen is the currency that

has the strongest correlation with the gold price. The correlation is clearly

illustrated by the following chart. It therefore isn't surprising that the

rebound in the gold price from a mid-December low has gone hand-in-hand with a

rebound in the Yen. Furthermore, evidence (mainly in the form of the COT data)

that the Yen's rebound is not complete supports the short-term bullish case for

gold, and evidence (in the form of the bond/dollar ratio and the COT data) that

gold's rebound is not complete supports the short-term bullish case for the Yen.

Zooming-in on the Yen's recent price action, we have a bounce from an

'oversold' extreme to the 50-day MA and then a pullback. This is normal for the

first phase of a larger rally.

It can take time for confidence to build

in the sustainability of a rally, with speculators initially being hesitant to

'go long' and each step forward being followed by half a step backward. That's

the case right now with the Yen. When the Yen bottomed in December, speculators

had a large net-short position in Yen futures. Despite the rebound of the past

few weeks the speculative net-short position has hardly changed at all, which

from a contrarian perspective is bullish.

We

expect to see the Yen in the 90s before the end of this quarter.

Updates

on Stock Selections

Notes: 1) To review the complete list of current TSI stock selections, logon at

http://www.speculative-investor.com/new/market_logon.asp

and then click on "Stock Selections" in the menu. When at the Stock

Selections page, click on a stock's symbol to bring-up an archive of

our comments on the stock in question. 2) The Small Stock Watch List is

located at http://www.speculative-investor.com/new/smallstockwatch.html

Company

news/developments for the week ending Friday 20th January 2017:

Company

news/developments for the week ending Friday 20th January 2017:

[Note: AISC = All-In Sustaining Cost, FS = Feasibility Study, FY = Financial

Year, IRR = Internal Rate of Return, ISR = In-Situ Recovery, MD&A = Management

Discussion and Analysis, M&I = Measured and Indicated, NAV = Net Asset Value,

NPV(X%) = Net Present Value using a discount rate of X%, P&P = Proven and

Probable, PEA = Preliminary Economic Assessment, PFS = Pre-Feasibility Study]

*Just in case it isn't already well known we point out that

Evolution Mining (EVN.AX), via two deals that were done at opportune

times last year, has exposure to copper in addition to gold. First, EVN has

current copper production of around 45M pounds/year thanks to its agreement,

last August, to buy a stake in Glencore's Ernest Henry copper-gold mine. The

copper production will be accounted for as a byproduct of the acquired gold

production, which means that copper sales revenue will be deducted from the cost

line rather than added to the revenue line. A rise in the copper price therefore

reduces the reported gold-production cost. Second, EVN added a 1.5B-pound copper

resource to its portfolio via the purchase, last October, of the Marsden

copper-gold project from Newcrest Mining.

This constitutes unlevered,

low-risk exposure to copper.

*Taseko Mines (TGB)

announced an improvement in the estimated economics of its development-stage

Florence copper project in Arizona. Assuming a long-term copper price of

$3/pound, the estimated pre-tax NPV(7.5%) and IRR have increased from US$850M

and 39% to US$920M and 44%, respectively. The earlier numbers were part of a

PFS completed in 2013.

The improvement is good news, but it is

annoying that the company chose to report PRE-tax economics and assumed a copper

price that's almost 20% above the current spot price. Unless the company has

figured out a way to avoid tax, reporting the project economics excluding tax

makes about as much sense as reporting the project economics excluding materials

or energy or any other major cost.

What we are interested in are the

POST-tax project economics at a range of prices that span the current spot

price. Based on information in the 2013 PFS, the Florence project appears to be

economically robust at $2.50/pound and might still be viable at $2.25/pound.

TGB provides highly-levered, relatively-high-risk exposure to copper.

*UEX Corp. (UEX.TO) is raising C$6M by issuing

non-flow-through shares at C$0.25 and flow-through shares at C$0.30. The total

number of new shares is expected to be about 16M.

As an

exploration-stage uranium miner with no revenue, UEX must regularly issue new

shares to fund its business. The new shares reduce the company's per-share value

when they are issued at depressed prices (despite having rebounded strongly with

most other uranium stocks over the past couple of months, UEX's stock price can

still be classed as "depressed"), but it has to be done.

List

of candidates for new buying

From within the ranks of TSI stock

selections the best candidates for new buying at this time, listed in

alphabetical order, are:

1) AAU at around US$0.90 (last Friday's closing

price: US$1.00)

2) ALK.AX at A$0.35 or lower (last Friday's closing

price: A$0.37)

3) ESM.TO (last Friday's closing price: C$0.83)

4)

SCP.TO (last Friday's closing price: C$0.54) or ADI.V (last Friday's closing

price: C$0.19). Note that these companies are merging and that -- due to the

warrants to be received by ADI shareholders as part of the merger -- fair value

for ADI is slightly more than one-third the price of SCP. For example, with SCP

at C$0.54, fair value for ADI would be about C$0.19.

The above list is

limited to five stocks. It will sometimes contain less than five, but it will

never contain more than five regardless of how many stocks are attractively

priced for new buying.

Chart Sources

Charts appearing in today's commentary

are courtesy of:

http://stockcharts.com/index.html

http://www.mrci.com/

http://www.goldchartsrus.com/

http://research.stlouisfed.org/